In‑depth explainer on emerging stablecoin bills, from the US GENIUS Act and yield fight to Hong Kong and Canada’s regimes, unpacking how new laws on reserves, licensing, and interest reshape USDC‑style tokens, DeFi, and the future of digital dollars.

+6 sources across the wider coverage universe

Deloitte and Stablecorp build QCAD institutional payment rails as Canada advances stablecoin regulation via Bill C-152026-03

Deloitte and Stablecorp build QCAD institutional payment rails as Canada advances stablecoin regulation via Bill C-152026-03 Tether to be brought under US jurisdiction, regardless of where it is based, according to newest version of Genius Stablecoin Bill2025-05

Tether to be brought under US jurisdiction, regardless of where it is based, according to newest version of Genius Stablecoin Bill2025-05 Ripple, Circle, and BitGo are pursuing U.S. trust bank licenses amid regulatory shifts, as stablecoin bills like the Genius Act push crypto closer to traditional finance. Kraken eyes a debit card, while Robinhood and Revolut expand banking services.2025-07

Ripple, Circle, and BitGo are pursuing U.S. trust bank licenses amid regulatory shifts, as stablecoin bills like the Genius Act push crypto closer to traditional finance. Kraken eyes a debit card, while Robinhood and Revolut expand banking services.2025-07 American Stablecoin legislation remains on shaky ground as draft bills spark industry division amid Trump 2.0 and a Republican majority, with lobbyists reportedly pushing unconfirmed proposals to ban non-U.S. issuers from buying Treasurys.2025-02

American Stablecoin legislation remains on shaky ground as draft bills spark industry division amid Trump 2.0 and a Republican majority, with lobbyists reportedly pushing unconfirmed proposals to ban non-U.S. issuers from buying Treasurys.2025-02 U.S. Lawmakers indicate progress on Stablecoin Bill, the final version expected soon.2024-04

U.S. Lawmakers indicate progress on Stablecoin Bill, the final version expected soon.2024-04 US Senate Banking Committee will vote on the updated, bipartisan GENIUS Act stablecoin bill—led by GOP Senators Bill Hagerty, Cynthia Lummis, and Tim Scott, along with Democrats Kirsten Gillibrand and Angela Alsobrooks—on March 13, following bipartisan discussions.2025-03

US Senate Banking Committee will vote on the updated, bipartisan GENIUS Act stablecoin bill—led by GOP Senators Bill Hagerty, Cynthia Lummis, and Tim Scott, along with Democrats Kirsten Gillibrand and Angela Alsobrooks—on March 13, following bipartisan discussions.2025-03

Stablecoin Bills: How New Laws Are Rewiring Crypto’s Dollar Backbone

Lawmakers in the United States and abroad are racing to pass “stablecoin bills” that define who can issue fiat‑pegged tokens, how they must be backed, and whether they can pay yield, reshaping the core plumbing of crypto markets in the process. At the center of this shift sits the US GENIUS Act and related market‑structure proposals, which together aim to turn systemically important stablecoins like USDC‑style products into tightly regulated payment instruments rather than lightly supervised crypto experiments.

What People Mean By A “Stablecoin Bill”

In policy conversations, a “stablecoin bill” is shorthand for legislation that creates a legal and supervisory framework for so‑called payment stablecoins, meaning digital tokens designed to hold a stable value relative to a reference currency such as the US dollar and to be used primarily for payments and settlement. In practice, most of these bills focus on fiat‑backed stablecoins that maintain stability by holding reserves in cash and safe short‑term assets, rather than on algorithmic designs that rely on mechanisms like over‑collateralization or arbitrage incentives. The US GENIUS Act, for example, defines a payment stablecoin as a digital asset designed for use as a means of payment or settlement and backed on a one‑to‑one basis by US dollars or other high‑quality liquid assets. Hong Kong’s new Stablecoins Ordinance similarly covers “fiat‑referenced stablecoins,” meaning tokens referencing one or more legal‑tender currencies.

What distinguishes a stablecoin bill from broader “cryptocurrency bills” is this tight focus on tokens that behave like money rather than like speculative investment assets. General market‑structure legislation such as the US Digital Asset Market Clarity Act seeks to clarify whether a wide range of crypto tokens are securities, commodities, or something else. By contrast, stablecoin bills usually start from the premise that core payment stablecoins should sit inside the traditional prudential regulatory perimeter, with rules on reserves, redemption, and risk management that look more like those for banks or money‑market funds than for equities. That is why the GENIUS Act explicitly amends federal banking and securities laws to clarify that qualifying payment stablecoins are not securities and cannot be treated as such by the SEC or bank regulators, thereby steering them into a bespoke payments regime.

When crypto market participants talk about “the stablecoin bill,” they are usually referring to the GENIUS Act in the United States, because it is the first federal statute to set out a comprehensive framework for dollar‑pegged payment stablecoins and their issuers. In practice, however, the policy landscape is more fragmented. On Capitol Hill, the GENIUS Act interacts with House proposals such as the STABLE Act and a bipartisan bill promoted by Representative Maxine Waters, as well as with the broader Clarity Act that tackles issues like stablecoin yield and the classification of other crypto assets. At the same time, jurisdictions like Hong Kong and Canada have enacted or proposed their own stablecoin legislation, and US states such as Florida are experimenting with state‑level licensing regimes. Understanding what a “stablecoin bill” does thus requires a comparative lens, not just a narrow focus on a single statute.

For traders and developers, the practical question is how these laws will affect familiar tokens like USDC, USDT, and newer fiat‑backed coins or tokenized T‑bill products, as well as the infrastructure that supports them. Many of the largest centralized stablecoins already voluntarily hold conservative reserves and publish attestations, but until now they have operated under a patchwork of state money‑transmitter rules, offshore licenses, and informal guidance from agencies like the SEC and CFTC. The stablecoin bills now moving forward would transform that patchwork into explicit licensing regimes, with strict requirements for reserve segregation, redemption rights, anti‑money‑laundering controls, and in some jurisdictions explicit prohibitions on paying interest‑like yield. As a result, the legal status of stablecoins as “crypto dollars” is converging toward a world in which they are treated less like experimental tokens and more like regulated digital cash.

Deloitte and Stablecorp build QCAD institutional payment rails as Canada advances stablecoin regulation via Bill C-15

Deloitte involvement in QCAD means enterprise adoption likely. Bill C-15 creating clear rules makes Canada competitive for stablecoin innovation

Readers clicked most heavily on extraterritorial jurisdiction over Tether and the race by crypto firms to obtain bank licenses — revealing that the real story is not stablecoin policy in the abstract but who gets to issue dollars on the internet and whether offshore players like Tether get squeezed out by U.S. law.↗

Why Stablecoin Legislation Is Arriving Now

The rush to legislate on stablecoins reflects their evolution from a niche trading tool into systemic infrastructure for both crypto and, increasingly, traditional finance. Fiat‑backed stablecoins now routinely settle tens of billions of dollars in on‑chain value per day, serve as base money for centralized and decentralized exchanges, and are increasingly used for cross‑border remittances and institutional payments. Policymakers worry that such a fast‑growing, dollar‑denominated market operating largely outside traditional prudential oversight could pose risks similar to those posed by shadow banking, including the potential for runs if users lose confidence in an issuer’s reserves. The experience of algorithmic stablecoin failures and stress events in crypto money markets has sharpened those concerns, even though most current legislation targets fiat‑backed tokens rather than algorithmic designs.

In the United States, stablecoin regulation also sits at the intersection of several political priorities: protecting consumers after a series of high‑profile crypto failures, defending US dollar dominance in digital markets, and ensuring that offshore issuers do not create systemic exposures without being subject to US law. The White House fact sheet announcing President Donald Trump’s signing of the GENIUS Act explicitly framed the legislation as a way to “make America the leader in digital assets” by creating the first federal regulatory system for stablecoins with strong reserve requirements. Senators backing the bill have presented it as a pragmatic way to harness private‑sector innovation while ensuring that tokens used as digital dollars are safe, transparent, and fully backed. At the same time, lawmakers like Representative Waters have emphasized the need to prevent large technology companies and foreign issuers from using stablecoins to build quasi‑banking empires outside traditional safeguards.

Internationally, the sense of urgency comes from both competitive and defensive concerns. Hong Kong has positioned its Stablecoins Ordinance as a key plank in its strategy to become a leading international hub for virtual assets while mitigating risks to financial stability. The ordinance creates a comprehensive licensing framework for stablecoin issuers and service providers, with strict reserve, redemption, and governance requirements, aiming to attract reputable firms while reassuring global regulators that Hong Kong’s virtual‑asset ecosystem is well supervised. Canada, meanwhile, has proposed federal stablecoin legislation in Bill C‑15 that assigns the Bank of Canada specific responsibilities in respect of stablecoins and requires it to maintain a public registry of stablecoin issuers, signaling that the country views stablecoins as systemically important instruments that warrant central‑bank oversight. A strategic collaboration between Deloitte Canada and QCAD issuer Stablecorp explicitly positions that CAD‑denominated stablecoin as an institutional payments rail that will operate within this emerging federal framework.

The geopolitical dimension is particularly clear in debates over foreign‑domiciled issuers like Tether. The Atlantic Council has warned that if US legislation does not effectively cover offshore dollar‑pegged stablecoins widely used in US‑facing crypto markets, it could create a “Tether loophole” that undermines the core purpose of regulation by allowing key risks to remain outside US jurisdiction. Waters’ bipartisan bill responds to this concern by explicitly seeking to close loopholes that would allow issuers like Tether to evade US law simply by basing themselves overseas, for example by conditioning access to US customers and financial infrastructure on compliance with US standards. As stablecoins become more deeply entangled with cross‑border payments and global capital markets, the question of how national laws interact and whether regulatory arbitrage will persist has become central to the policy agenda.

Finally, stablecoin legislation is at the leading edge of a broader push to clarify crypto market structure in the United States. The GENIUS Act is tightly focused on payment stablecoins, but it moves in parallel with the Digital Asset Market Clarity Act, which the House has already passed and which the Senate Banking Committee has advanced with bipartisan support. That broader bill addresses issues such as the division of labor between the SEC and CFTC, the status of crypto exchanges, and the rules around offering yield on stablecoin balances. Because stablecoins function as the settlement layer for much of the crypto ecosystem, lawmakers see them as a natural starting point for imposing guardrails while more contentious debates around other tokens continue. For crypto firms, this sequencing means that stablecoin compliance is likely to be the first piece of the new regulatory puzzle they must solve.

The GENIUS Act: The Flagship U.S. Stablecoin Framework

Origins And Political Coalition

The Guiding and Establishing National Innovation for U.S. Stablecoins Act, or GENIUS Act, began as a Senate bill introduced on February 4, 2025, by Senator Bill Hagerty, with co‑sponsorship from Senate Banking Committee Chair Tim Scott and Senators Kirsten Gillibrand and Cynthia Lummis. The bill drew on a discussion draft circulated in October 2024 and reflected months of negotiation among Republicans and Democrats who saw payment stablecoins as one of the more tractable areas for bipartisan crypto legislation. After an initial failure to secure a procedural vote, the Senate ultimately passed the GENIUS Act on June 17, 2025, with a 68–30 bipartisan vote, marking the first time the chamber approved significant digital‑asset legislation. Observers described the vote as a watershed moment that “broke the crypto dam,” in the sense that it opened the way for further market‑structure reforms by demonstrating that bipartisan agreement on at least some aspects of crypto policy was possible.

Once Congress sent the bill to the White House, President Trump signed it into law, with an official fact sheet presenting the GENIUS Act as a “historic piece of legislation” that would pave the way for the United States to lead the global digital currency revolution. The administration emphasized that the law created the first federal regulatory system for stablecoins, with strong reserve requirements, consumer protections, and explicit anti‑money‑laundering obligations. At the same time, House committees continued working on companion legislation, including the STABLE Act and broader market‑structure bills, some of whose provisions will interact closely with the GENIUS framework. The result is that “the stablecoin bill” in US discourse is both a standalone law and part of a larger package of crypto reforms whose details are still being negotiated.

What Counts As A “Payment Stablecoin”

A central move in the GENIUS Act is the creation of a legally defined category of payment stablecoins, which anchors the rest of the regulatory architecture. The Act defines a payment stablecoin as a digital asset that is designed to be used as a means of payment or settlement and that maintains a stable value relative to a fixed monetary value, typically the US dollar, by holding backing assets. The law requires that these payment stablecoins be fully backed on a one‑to‑one basis with reserve assets such as US dollars or specified high‑quality liquid instruments, including short‑term Treasury bills and certain repurchase agreements. In addition, issuers must maintain public redemption policies and take necessary steps to ensure price stability relative to the US dollar, reinforcing the idea that payment stablecoins should behave like digital cash rather than speculative assets.

This statutory definition draws a sharp line between fiat‑backed payment stablecoins and other types of tokens that sometimes market themselves as “stablecoins.” Algorithmic designs that rely on dynamic supply adjustments or collateralized debt positions rather than holding matching reserves would generally fall outside the GENIUS definition, unless a centralized issuer assumed a binding redemption obligation and maintained specified reserves. Similarly, tokenized money‑market fund shares or tokenized bank deposits may not qualify as payment stablecoins if they are structured as securities or deposits rather than as standalone digital assets with direct redemption rights. By narrowing the category in this way, Congress seeks to ensure that only tokens that truly function as general‑purpose payment instruments receive the regulatory treatment and legal clarity the Act confers.

It is also important that the Act’s definition hinges on an issuer obligation to convert, redeem, or repurchase the stablecoins at a fixed monetary value and to maintain stable value. That issuer‑centric focus underpins the law’s licensing and supervisory regime, because regulators can tie obligations such as reserve maintenance, audits, and compliance programs to identifiable legal entities. It also means that decentralized protocol‑issued stablecoins without a single accountable issuer may fall outside the core GENIUS category, at least directly, even though they may still be affected indirectly through restrictions on intermediaries that list or custody such assets. This issuer emphasis is echoed in other jurisdictions’ laws, such as Hong Kong’s requirement that stablecoin reserves be held in trust and safeguarded by qualified custodians under license, underscoring a global trend toward placing regulatory obligations on clearly identifiable responsible parties.

Licensing, Oversight, And The Federal–State Split

The GENIUS Act makes it unlawful to issue a payment stablecoin in the United States unless the issuer is a permitted payment stablecoin issuer, a new regulatory status that brings issuers under direct prudential supervision. To qualify as a permitted issuer, an entity must fall into one of several categories specified in the Act, notably including banks and certain nonbank entities that obtain federal or state licenses under the new framework. Issuers with more than 10 billion dollars in total stablecoin market capitalization are subject to federal regulation by the appropriate federal banking agency, such as the Federal Reserve, the Office of the Comptroller of the Currency (OCC), or the Federal Deposit Insurance Corporation (FDIC). Issuers with 10 billion dollars or less in market capitalization may opt for state regulation by a relevant state banking agency, provided that the state regime is deemed “substantially similar” to the federal framework.

This structure reflects a political compromise between federal standard‑setting and the longstanding role of US states in overseeing nonbank financial services. On the one hand, the law allows states that adopt robust stablecoin regimes to remain active supervisors of smaller issuers, thereby preserving existing state innovation hubs and tailoring. On the other hand, it prevents a race to the bottom by conditioning state oversight on Treasury’s determination that the regime is substantially similar to federal standards and by authorizing federal regulators to take enforcement action against state‑regulated issuers in certain circumstances. For example, the Act grants the Federal Reserve, OCC, and FDIC authority analogous to their powers under Section 8 of the Federal Deposit Insurance Act, enabling them to issue cease‑and‑desist orders, impose civil money penalties, or revoke licenses when issuers fail to meet compliance standards.

The law also anticipates growth and migration. If a state‑regulated issuer crosses the 10 billion dollar threshold in total issuance, it must transition to federal oversight within 360 days or cease issuing new stablecoins until it again falls below the threshold. This mechanism allows startups or smaller projects to launch under state regimes that meet federal criteria, while ensuring that larger, systemically significant issuers migrate into direct federal supervision over time. A parallel logic appears in emerging state frameworks like Florida’s Payment Stablecoin bill, which revises the state’s anti‑money‑laundering rules to include payment stablecoins and prohibits persons from engaging in the activities of a qualified payment stablecoin issuer without being licensed or exempt, while specifying the activities licensed issuers may undertake. Together, these federal and state developments are gradually transforming stablecoin issuance from a lightly regulated money‑services business into a prudentially supervised financial activity with a clear regulatory home.

Reserves, Disclosures, Redemption, And Insolvency

At the heart of the GENIUS Act are stringent reserve requirements designed to ensure that payment stablecoins are fully and safely backed. The White House fact sheet emphasizes that the legislation requires 100 percent reserve backing with liquid assets such as US dollars or short‑term US Treasury securities, coupled with monthly public disclosures of the composition of reserves. The Act further mandates segregation of reserve assets from the issuer’s own property, prohibits rehypothecation of reserves, and imposes capital and liquidity requirements to ensure that issuers can meet redemption requests even under stress. These provisions are meant to prevent situations in which stablecoin issuers invest reserves in risky or illiquid assets, creating a mismatch between user expectations of cash‑like safety and the reality of their backing.

Transparency is a key complement to these reserve rules. Issuers must provide monthly certifications and other reporting on their reserves, allowing both regulators and the public to verify that tokens are fully backed and that reserve composition remains within prescribed limits. The law’s emphasis on public disclosures echoes similar requirements in Hong Kong’s Stablecoins Ordinance, which requires licensees to make public their reserve management policies, the composition and market value of their reserve assets, and the results of regular independent attestations and audits. Hong Kong goes even further by requiring daily reserve statements and weekly reporting to its monetary authority, underscoring how regulators around the world see frequent disclosures as essential to maintaining confidence in digital cash‑like instruments.

The GENIUS Act also codifies redemption rights. Payment stablecoin issuers must maintain clear policies allowing holders to redeem their tokens at par value in a timely manner, reinforcing the expectation that these stablecoins function as close substitutes for bank deposits or cash. Although the US law does not specify precise redemption timelines in the same way as Hong Kong’s requirement that redemptions be fulfilled at par within one business day without unreasonable fees, the overall structure reflects a similar concern with ensuring that stablecoin users can exit positions quickly and at face value. Redemption rights are particularly important during stress events, when users may rush to cash out, and regulators want to avoid destabilizing runs that could spill over into other markets.

Crucially, the GENIUS Act prioritizes stablecoin holders’ claims over those of other creditors in the event of an issuer insolvency. This creditor‑priority rule effectively treats stablecoin reserves as a trust‑like pool dedicated to users, echoing Hong Kong’s requirement that reserves be held on trust and segregated from the issuer’s own assets. By insulating reserve assets from the issuer’s general creditors, the law aims to prevent situations in which stablecoin users find themselves competing with other claimants in bankruptcy, thereby enhancing confidence in the tokens as safe settlement assets. For centralized stablecoins like USDC that already market themselves as fully reserved with high‑quality liquid assets, these legal protections formalize and reinforce existing practices, while raising the bar for competitors.

AML, Sanctions, And Technical Control Requirements

Another pillar of the GENIUS Act is its explicit integration of payment stablecoins into the United States’ anti‑money‑laundering (AML) and sanctions apparatus. The Act expressly subjects stablecoin issuers to the Bank Secrecy Act, clearly obligating them to establish effective AML and sanctions compliance programs, including risk assessments, sanctions‑list screening, and customer identification procedures. This removes any ambiguity about whether major stablecoin issuers must behave like other financial institutions in monitoring for illicit finance and complying with sanctions. Payment stablecoin issuers are classified as financial institutions for AML purposes, reinforcing their obligations to file suspicious activity reports and maintain appropriate records.

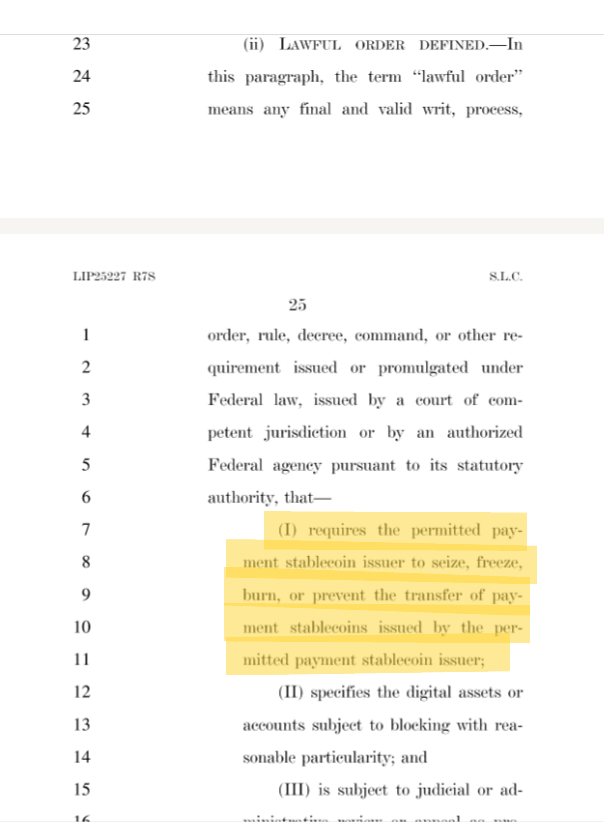

The Act also contains a requirement that all stablecoin issuers possess the technical capability to seize, freeze, or burn payment stablecoins when legally required and to comply with lawful orders to do so. This provision essentially codifies a design expectation that authorized issuers will retain some degree of centralized control over their tokens at the smart‑contract level, at least sufficient to block or claw back funds when ordered by a court or regulator. While most major centralized stablecoins already include such administrative functions in their contract code, embedding them in statute underscores how lawmakers view technical design as an integral part of regulatory compliance, not a separate engineering choice. It also raises questions about the compatibility of truly immutable, censorship‑resistant stablecoins with the regulatory frameworks now being built.

These AML and technical‑control requirements are broadly consistent with international trends. Hong Kong’s Stablecoins Ordinance, for example, mandates that licensees implement effective, risk‑based AML/CFT policies, procedures, and controls, including governance structures, risk assessments, staff training, sanctions screening, suspicious‑transaction reporting, and record‑keeping. Canada’s emerging framework likewise positions stablecoins within the orbit of regulated financial services, with the Bank of Canada tasked with maintaining a public registry of issuers, implying coordination with existing AML and sanctions enforcement regimes. For crypto users, the practical consequence is that on‑chain stablecoin transactions increasingly sit within a traceable, compliance‑driven environment, particularly at the issuer and custodial levels, even if peer‑to‑peer transfers on public blockchains remain technically permissionless.

Securities, Custody, And The Role Of The SEC

One of the most contentious issues in US crypto policy has been whether and when tokens should be treated as securities, bringing them under the jurisdiction of the SEC. The GENIUS Act takes a firm position on this question for qualifying payment stablecoins by amending federal securities laws to make clear that they are not securities and cannot be classified as such by the SEC, federal banking agencies, or the National Credit Union Administration. The Act also prohibits these regulators from requiring an asset held in custody to be treated as a liability on a custodian’s balance sheet, a change aimed at resolving accounting issues that have complicated banks’ ability to offer digital‑asset custody services. Together, these provisions are designed to treat payment stablecoins as payment instruments, more akin to deposits or stored‑value balances than to investment products.

Clarifying that payment stablecoins are neither securities nor commodities also shifts the primary regulatory locus from the SEC and CFTC to banking regulators and the Federal Reserve, consistent with the Act’s emphasis on prudential oversight. At the same time, the House Waters bill explicitly preserves the existing authorities of agencies like the Treasury, SEC, CFTC, and the Consumer Financial Protection Bureau with respect to entities covered by the Act, such as wallet providers, broker‑dealers, exchanges, and market‑makers, to the extent they engage in activities subject to their jurisdiction. In other words, while the GENIUS framework carves out a specific regulatory lane for payment stablecoin issuance and core operations, it does not remove other aspects of stablecoin‑related activity from broader financial‑regulatory oversight.

Custody rules are another important component. The GENIUS Act imposes customer‑protection standards on persons that provide custody services for permitted payment stablecoins, including supervision and regulation, segregation of customer funds, prohibitions on commingling, and requirements to provide monthly audited reports on fiat reserves backing the tokens they hold. These obligations are intended to protect stablecoin users from the kinds of misuses of customer funds seen in some failed crypto platforms, by ensuring that custodians cannot treat stablecoin balances as their own property or use them for proprietary trading. Similar themes appear in Hong Kong’s requirement that reserve assets be held on trust and segregated from issuers’ own assets, safeguarded by qualified custodians, and subject to regular independent audit and disclosure. As a result, both issuers and custodial service providers face a much more bank‑like compliance and reporting environment.

Even with DC gridlocked, momentum for crypto market structure reform has never been stronger — after bipartisan meetings on the Hill, both sides are 90% aligned, and Coinbase remains confident a clear DeFi and stablecoin bill could pass by year-end.

He's not splitting hairs!

- 01Tether US jurisdiction reach↗

The revelation that the GENIUS Act would bring Tether under U.S. law regardless of domicile was the single most-clicked angle, signaling readers understand this as an existential threat to the dominant offshore issuer.

- 02Crypto firms chasing bank licenses↗

Ripple, Circle, and BitGo pursuing trust bank charters — alongside Kraken's debit card and Robinhood/Revolut banking expansion — showed readers that stablecoin legislation is the forcing function pushing crypto into regulated finance.

- 03GENIUS Act vs STABLE Act↗

Readers engaged with the head-to-head comparison because the yield ban in the STABLE Act and differing treatment of decentralized stablecoins like DAI meant the choice of bill determines winners and losers across the entire sector.

- 04Senate passage momentum↗

Multiple high-click headlines tracked the cloture vote, final vote scheduling, and eventual Senate passage, reflecting readers treating each procedural step as a market-moving event.

- 05Stablecoin yield ban stakes↗

The prospect of Congress banning interest-bearing stablecoins drew repeated engagement because it directly threatens the revenue model of DeFi protocols and emerging consumer products.

- 06Global regulatory race↗

Hong Kong's licensing regime passage and Canada's Bill C-15 institutional rails showed readers that U.S. delay hands competitive ground to other jurisdictions.

The Fight Over Stablecoin Yield

What “Stablecoin Yield” Means In Practice

While the GENIUS Act focuses on making payment stablecoins safe and well regulated, a parallel and increasingly intense debate concerns stablecoin yield—that is, whether and how issuers, exchanges, and DeFi protocols should be allowed to pay interest‑like returns on stablecoin balances. In practice, stablecoin yield can arise from several sources. Centralized platforms may offer savings‑account‑style products that pay a fixed or variable percentage on USDC or USDT balances, funded by lending those tokens to traders or rehypothecating underlying reserves into higher‑yielding assets. DeFi protocols may offer liquidity‑provider rewards, lending interest, or governance‑token incentives that produce economic returns for stablecoin holders. And some issuers have experimented with explicit yield‑bearing stablecoins backed by interest‑accruing assets like US Treasuries.

Regulators worry that if stablecoin balances paying yield become close substitutes for insured bank deposits, they could undermine traditional banks’ funding base and create shadow‑banking risks outside the existing supervisory perimeter. Banks have argued that allowing nonbank stablecoin platforms to pay interest essentially replicates deposit‑taking without the capital, liquidity, and resolution regimes that protect depositors and the financial system. At the same time, crypto advocates respond that yield is an integral part of programmable money, enabling innovative treasury, collateral, and payments applications that rely on the returns generated by tokenized safe assets like Treasury‑backed stablecoins. Industry participants also note that prohibiting yield in regulated venues may simply push users toward riskier, offshore, or unregulated products, without eliminating demand.

The policy challenge, therefore, is to distinguish between stablecoin yield products that pose genuine bank‑like risks and those that represent low‑risk, transparent returns from holding tokenized cash‑equivalent instruments. The White House’s own stablecoin yield report captures this nuance, concluding that a blanket yield prohibition would do little to protect bank lending while forgoing potential consumer benefits, and recommending a more tailored approach that focuses on products that are economically equivalent to bank deposits. This tension has played out in congressional negotiations, where lawmakers seek to satisfy banks’ concerns without overly constraining innovation in digital‑asset markets.

The Clarity Act And Its Yield Provisions

The most concrete legislative vehicle for stablecoin‑yield rules in the United States is the Digital Asset Market Clarity Act of 2025, often referred to as the Clarity Act. Alongside its broader crypto‑market‑structure provisions, a key section of the bill addresses stablecoin rewards. Language crafted by Senators Angela Alsobrooks and Thom Tillis bars crypto firms from issuing rewards on stablecoin balances that are “economically or functionally equivalent” to interest‑bearing bank deposits. The legislation aims to prevent nonbank stablecoin platforms from offering deposit‑like products that compete head‑on with traditional savings accounts without being subject to the same regulatory obligations and safety nets.

In March, the Senate Banking Committee approved a version of the Clarity Act, including the yield language, by a 15–9 vote, with two Democrats joining the committee’s Republicans to move the bill forward. The Act now heads to the full Senate, where it will require sixty votes to be considered and would then need to be reconciled with a House bill passed earlier. Banking trade groups have argued that the yield restrictions should be further tightened by more explicitly prohibiting “interest‑like” rewards for simply holding stablecoins while allowing limited rewards linked to specific payment transactions or activities, such as loyalty points or merchant discounts, which they view as less deposit‑like. This distinction reflects the tricky line lawmakers are trying to draw between prohibiting stablecoin products that mimic deposit accounts and preserving room for promotional incentives and innovative payments use‑cases.

The Clarity Act’s yield provisions have become a lightning rod in industry lobbying. Some crypto firms warn that an overly broad definition of “interest‑equivalent” could chill not just CeFi savings products but also DeFi protocols that algorithmically distribute trading fees or governance tokens, depending on how regulators interpret the law. Others argue that bringing yield products into a clearer regulatory framework could actually reduce uncertainty, enabling compliant yield‑bearing instruments that satisfy disclosure, risk‑management, and suitability requirements. The difficulty lies in crafting statutory language that can distinguish, in a technologically neutral way, between genuine investment products, bank‑like deposits, and low‑risk yield from tokenized safe assets without opening new loopholes.

The White House Yield Report And Competing Narratives

The Biden‑appointed and later Trump‑retained White House crypto policy team commissioned a Stablecoin Yield Report to inform this debate, and the findings complicate the case for a sweeping yield ban. According to a summary released by legal analysts, the report states that “a yield prohibition would do very little to protect bank lending, while forgoing the consumer benefits of” well‑designed stablecoin yield products, suggesting that the macroeconomic case for protecting bank credit supply by banning stablecoin yield is relatively weak. Instead, the report appears to favor a more targeted approach that differentiates between high‑risk, opaque yield schemes and transparent, well‑regulated products backed by safe assets and subject to robust disclosure and risk‑management rules.

This White House perspective has emboldened some industry participants who argue that stablecoin yield, if properly regulated, can coexist with a healthy banking system and even complement it by channeling savings into Treasury‑backed instruments and other safe assets. For example, Treasury‑backed stablecoins that pass through a portion of the interest earned on their underlying securities could, in principle, offer consumers a return comparable to money‑market funds while operating on a 24/7 programmable ledger. Proponents contend that prohibiting such products in the name of protecting banks ignores the evolution of capital markets and the shift of savings into nonbank vehicles that has been underway for decades. The real risk, in their view, is not yield per se but complexity, leverage, and inadequate supervision.

Banks and more cautious regulators, however, worry that once yield on stablecoins is permitted, competitive pressures will push platforms to increase returns, potentially leading to riskier reserve portfolios, longer‑duration exposures, or hidden leverage. They point to the history of money‑market funds and other cash‑equivalent instruments, which have required emergency backstops during crises despite conservative investment mandates. From this perspective, even if a blanket yield ban is not strictly necessary to protect bank lending, it may be a prudent safeguard against the emergence of a parallel, deposit‑like system without a lender of last resort. The stablecoin yield report’s skepticism about broad prohibitions thus feeds into an ongoing debate about whether the focus of regulation should be on the nature of underlying assets, the design of products, or the institutional form of issuers.

Market Reactions And Industry Strategies

Even before final legislation has passed, markets are already pricing in the potential impact of stablecoin yield restrictions. When one of the major crypto media outlets reported that a Big Four accounting firm had completed a significant audit for Tether and that pending crypto legislation threatened stablecoin yield, shares of Circle’s parent company fell, reflecting investor anxiety about how tighter rules might affect USDC‑centric business models built partly on interest from reserve assets. Exchanges and DeFi projects are likewise reassessing their product roadmaps to anticipate possible bans or curbs on interest‑like rewards for simply holding stablecoins, even if more complex DeFi yield structures might remain viable.

Industry responses have not been uniformly pessimistic. In interviews and conference appearances, some executives, such as Abra CEO Bill Barhydt, have argued that fears about stablecoin yield bans are overstated and that there will remain substantial opportunities to build compliant yield products, especially those aimed at institutions and treasuries rather than retail savers. Other firms are pursuing regulatory strategies to position themselves as banks or trust banks, betting that by coming under full prudential regulation they can offer a wider range of yield‑bearing services. Recent moves by companies like Ripple, Circle, and BitGo to seek US trust bank licenses, as reported in industry coverage, can be seen in this light: they are preparing for a future where only bank‑like entities can offer deposit‑like stablecoin products, while nonbank platforms stick to pure payments tokens and non‑interest‑bearing services.

Politically, the yield issue has drawn in high‑profile figures beyond traditional financial‑policy circles. Reporting has highlighted comments by Eric Trump, co‑founder of World Liberty Financial, criticizing banks’ efforts to tighten yield restrictions, reflecting how the debate over stablecoin rewards has become entangled with broader partisan narratives about innovation, incumbents, and financial freedom. At the same time, lawmakers such as Senator Tim Scott have publicly emphasized that crypto bills advancing through the Senate include draft yield provisions that will be refined through negotiation, underscoring that nothing is final. The outcome of this legislative tug‑of‑war will shape not only how stablecoin issuers design their products but also where yield‑seeking capital flows in the broader digital‑asset ecosystem.

Competing U.S. Visions: STABLE, Waters, And State Frameworks

The House STABLE Act And Maxine Waters’ Bipartisan Bill

While the GENIUS Act originated in the Senate, the House of Representatives has been developing its own stablecoin proposals, most notably the Stablecoin Transparency and Accountability for a Better Ledger Economy Act, or STABLE Act, and a separate bipartisan bill spearheaded by Representative Maxine Waters. The STABLE Act began as a discussion draft released by House Financial Services Committee Chairman French Hill and Representative Bryan Steil in early February 2025, aimed at commencing a companion process to the Senate’s GENIUS legislation. The bill has since advanced out of committee, though it has not yet received a full House vote, and its final contours will likely be shaped in conference negotiations with the Senate.

Representative Waters’ bipartisan payment stablecoin legislation, developed over three years of staff work and in close consultation with the Treasury Department and Federal Reserve, represents another influential House perspective. Her bill creates a regulatory framework for both depository‑institution and nonbank stablecoin issuers, with a central role for the Federal Reserve and strong reserve requirements similar in spirit to the GENIUS Act. It goes further in some respects, however, particularly in its treatment of ownership and governance. To preserve the traditional separation of banking and commerce, the legislation prohibits non‑financial commercial companies—explicitly including large technology firms like Facebook, Google, and X—from owning a stablecoin issuer. This reflects concerns that Big Tech could leverage their vast user bases and data to build dominant private monetary systems, potentially undermining competition and financial stability.

Waters’ bill also includes detailed conduct and suitability provisions. It imposes explicit obligations on issuers to comply with sanctions and anti‑money‑laundering and counter‑terrorist‑financing laws and seeks to close offshore loopholes that could allow issuers like Tether to circumvent US law by operating from foreign jurisdictions while accessing US customers. The bill bans certain convicted individuals, such as FTX founder Sam Bankman‑Fried, from serving as executive officers of a stablecoin issuer or controlling more than 5 percent of its shares, reflecting a desire to prevent individuals with histories of serious financial misconduct from controlling key financial infrastructure. It also contains robust protections for consumer wallets, including risk‑management and financial‑resource requirements for wallet providers and backup examination and enforcement authority for the Federal Reserve. Importantly, the bill explicitly preserves the existing authorities of agencies like the Treasury, CFPB, SEC, and CFTC over stablecoin‑related activities within their jurisdictions.

These House proposals thus share many themes with the GENIUS Act—such as full reserve backing, Federal Reserve involvement, and AML compliance—but differ in emphasis. Waters’ bill is more explicit about limiting Big Tech’s role, tightening governance standards, and closing foreign‑issuer loopholes, while GENIUS leans more heavily on prudential banking regulators and the distinction between large and small issuers. The ultimate shape of US stablecoin law will depend on how these strands are woven together in conference, but for market participants the key point is that both chambers are converging on a model of tightly regulated, fully backed payment stablecoins anchored in the existing banking and financial‑regulatory ecosystem.

The “Tether Loophole” And Foreign Issuers

One of the sharpest critiques of early US stablecoin proposals has come from policy analysts who warn that they may contain a foreign issuer loophole. The Atlantic Council has argued that by focusing primarily on issuers established in the United States, early drafts of both the GENIUS Act and STABLE Act risk leaving offshore issuers like Tether outside direct US prudential oversight, even though their dollar‑pegged tokens are widely used in US‑facing crypto markets. This so‑called “Tether loophole” is seen as undermining the purpose of US stablecoin legislation, because it would allow a significant portion of global dollar‑stablecoin activity to remain under weaker or less transparent regulatory regimes.

Waters’ bill directly targets this concern by including provisions that close loopholes allowing issuers like Tether to circumvent US law overseas. Although the full statutory language is complex, the basic approach is to tie access to US customers, banking relationships, and critical infrastructure to compliance with US standards, regardless of where an issuer is incorporated. This extraterritorial strategy mirrors tactics used in other areas of financial regulation and sanctions enforcement, where the centrality of the US dollar and US banks gives Washington leverage over non‑US entities. If implemented successfully, such provisions could bring foreign‑domiciled stablecoin issuers effectively under US jurisdiction in respect of their dollar‑pegged tokens, even while they remain headquartered abroad.

Designing these extraterritorial mechanisms is challenging. Overly aggressive measures risk fragmenting global markets if foreign regulators perceive them as unilateral overreach and respond with their own restrictions. Insufficiently robust measures, however, could leave major gaps. The Atlantic Council has proposed several ways to tighten US stablecoin bills, such as requiring any dollar‑pegged stablecoin accessible in the United States to meet US standards or conditioning access to US payment systems and Treasuries on adherence to certain reserve and disclosure requirements. As negotiations continue, the treatment of foreign issuers will remain a key fault line, not only for policymakers but also for traders and DeFi protocols that rely heavily on offshore stablecoins.

State‑Level Experiments: Florida And Beyond

In parallel with federal efforts, US states are beginning to experiment with their own stablecoin frameworks, particularly for smaller or regionally focused projects. Florida’s Payment Stablecoin bill, for example, revises the state’s Control of Money Laundering in Money Services Business Act to explicitly include payment stablecoins and prohibits persons from engaging in the activity of a qualified payment stablecoin issuer without being licensed or exempt from licensure. The bill requires applicants seeking to be qualified payment stablecoin issuers to submit specified applications to the state Office of Financial Regulation and limits licensed issuers to certain permitted activities. While the legislative process is still ongoing, with the Senate having laid the bill on the table and referred to a related House measure, the initiative illustrates how states envision stablecoin issuance as a regulated money‑services business tightly linked to their existing AML frameworks.

Such state‑level experiments can serve as testbeds for regulatory approaches that may later be harmonized with or superseded by federal standards. The GENIUS Act explicitly allows issuers with 10 billion dollars or less in market capitalization to opt into state regulation if the state regime is deemed substantially similar to the federal framework, thereby incentivizing states to develop compatible rules. States that move early, like Florida, could position themselves as attractive domiciles for smaller stablecoin projects if they align their standards with federal expectations while offering responsive supervision and tailored support. Conversely, a proliferation of divergent state rules could complicate compliance for multi‑state issuers and lead to calls for stronger federal preemption.

For crypto businesses, the interplay between state and federal stablecoin rules will influence decisions about where to incorporate, which licenses to seek, and how to structure products. Firms that serve national or global markets will likely gravitate toward the federal permitted‑issuer regime, while niche or regionally focused players may find state pathways more accessible, at least in the early stages. Over time, however, the gravitational pull of federal oversight is likely to grow as thresholds like the 10 billion dollar cap are reached and as markets and regulators push toward more uniform standards.

Ripple, Circle, and BitGo are pursuing U.S. trust bank licenses amid regulatory shifts, as stablecoin bills like the Genius Act push crypto closer to traditional finance. Kraken eyes a debit card, while Robinhood and Revolut expand banking services.

GENIUS Act introduced in Senate

Senate Banking Committee votes on bipartisan GENIUS Act

Senate cloture vote passes 68-30, clearing path to final vote

US Senate passes GENIUS Act

President Trump signs GENIUS Act into law

Hong Kong Stablecoin Bill passes legislature, licensing regime launches

A Global Race To Regulate: Hong Kong, Canada, And Beyond

Hong Kong’s Stablecoins Ordinance

Outside the United States, Hong Kong has emerged as one of the most proactive jurisdictions in building a comprehensive regulatory regime for stablecoin issuers. On May 21, 2025, its Legislative Council passed the much‑anticipated Stablecoins Bill, now cited as the Stablecoins Ordinance, marking a significant milestone in its ambition to be a leading international virtual‑asset hub. The Ordinance, which came into force on August 1, 2025, establishes a licensing framework for fiat‑referenced stablecoin issuers and service providers, with a six‑month transitional period for existing operators. The Hong Kong Monetary Authority (HKMA) is responsible for administering the regime and has been consulting on detailed guidelines covering issuance, reserve management, redemption, risk controls, and governance.

Under the Ordinance, the business of issuing fiat‑referenced stablecoins is a regulated activity that requires a license. Licensees must ensure that stablecoins are fully backed at all times by high‑quality, highly liquid reserve assets, such as short‑term bank deposits, certain marketable debt securities, dedicated investment funds, or other HKMA‑approved assets. Reserve assets are generally required to be denominated in the reference currency, with limited flexibility allowing, for example, reserves of HKD‑referenced stablecoins to be denominated in USD in some cases. Crucially, reserves must be held on trust, segregated from the issuer’s own assets, and safeguarded by qualified custodians, mirroring the trust‑like structures US and EU policymakers have discussed.

The Ordinance also places strong emphasis on transparency and disclosure. Licensees must publicly disclose their reserve‑management policies, the composition and market value of reserve assets, and the results of regular independent attestations and audits. They are required to prepare daily statements on reserves and outstanding stablecoins, submit weekly reports to the HKMA, and keep relevant information updated on a publicly accessible website. In terms of user protections, issuers must ensure that redemption requests are fulfilled at par value within one business day without unreasonable fees or conditions, and holders are granted rights to direct the disposal of reserve assets on a pro‑rata basis and to claim shortfalls in redemption even in the event of an issuer’s insolvency. This combination of trust‑based reserve segregation, rapid redemption, and strong disclosure aims to make Hong Kong‑licensed stablecoins behave very much like well‑regulated e‑money or cash‑equivalent instruments.

Hong Kong’s rules also address business conduct, governance, and risk management. Licensees must implement comprehensive risk‑management frameworks covering credit, liquidity, market, technology, operational, and reputational risks, including stress testing and incident response plans, and adopt a “three lines of defence” model encompassing business units, independent risk and compliance functions, and internal audit. Governance requirements include a clear organizational structure, defined responsibilities, transparent decision‑making processes, and a board with at least one‑third independent non‑executive directors, while senior management and key personnel must meet fitness and propriety standards approved by the HKMA. Licensees are required to publish white papers and maintain up‑to‑date public disclosures about reserve management, redemption mechanisms, and associated risks, and to maintain robust complaints‑handling and redress mechanisms. Importantly, they are also subject to rigorous AML/CFT obligations similar to those in the banking sector.

A distinctive feature of Hong Kong’s regime is a near‑blanket prohibition on paying interest or interest‑like incentives to stablecoin holders, except for limited marketing incentives that do not amount to interest. This rule reflects concerns about stablecoins evolving into deposit‑like investment products without proper deposit insurance or access to central‑bank liquidity. In effect, Hong Kong is opting for a pure‑payments model for fiat‑referenced stablecoins, in contrast to the more nuanced debate over yield seen in US policy circles. For global stablecoin issuers, these differences will shape product design and marketing strategies across jurisdictions.

Canada’s Bill C‑15 And The QCAD Experiment

Canada is moving toward its own federal stablecoin framework through Bill C‑15, an omnibus budget implementation bill that includes provisions defining the role of the Bank of Canada in respect of stablecoins. The legislation sets out the central bank’s objects regarding stablecoins and requires it to maintain a public registry of stablecoin issuers, effectively making the Bank of Canada a central node in the oversight and transparency of CAD‑denominated and potentially other stablecoins. While many details will be fleshed out in subsequent regulations, the choice to center stablecoin oversight in the central bank underscores Canada’s view of these tokens as systemically important payment instruments closely intertwined with monetary policy and financial stability.

The significance of Canada’s move is underscored by real‑world initiatives aiming to build institutionally compliant stablecoin infrastructure. Deloitte Canada and Stablecorp, issuer of the QCAD Canadian‑dollar stablecoin, announced a strategic collaboration to deliver QCAD‑based stablecoin infrastructure for financial institutions, explicitly framed as preparation for the anticipated progress of the federal government’s stablecoin framework and Bill C‑15. The alliance aims to help banks and other institutions integrate QCAD into their existing platforms and operations in a secure, compliant manner, focusing on use‑cases such as 24/7 collateral mobility, interbank clearing, cross‑border payments, and next‑generation treasury solutions involving on‑chain B2B payments and trade‑finance flows. By tying these initiatives to the legislative process, Canada signals that it intends to position regulated, domestically anchored stablecoins as key components of its future financial infrastructure.

Canada’s approach shares some similarities with both the US and Hong Kong models. Like the US, it leverages existing financial‑market institutions and central‑bank oversight, integrating stablecoins into familiar supervisory structures. Like Hong Kong, it emphasizes fully compliant, institutional‑grade infrastructure over lightly regulated retail‑trading use‑cases. However, Canada is unique in explicitly enshrining a central‑bank registry for stablecoin issuers in primary legislation, which may support more integrated oversight of systemic risk and interoperability with future central‑bank digital currency (CBDC) initiatives. For stablecoin issuers targeting the Canadian market, aligning with Bank of Canada expectations and building strong institutional partnerships will likely be essential.

Comparing Emerging Regimes

Although each jurisdiction’s stablecoin framework has its own nuances, several common themes and differences emerge when they are placed side by side. The following high‑level comparison illustrates these dynamics:

| Jurisdiction | Core Law / Bill | Who Can Issue | Reserve Requirements | Yield Allowed? | Primary Regulator / Role | Status |

|---|---|---|---|---|---|---|

| United States (federal) | GENIUS Act (payment stablecoins) | Permitted issuers: banks and licensed nonbanks; small issuers may use qualifying state regimes | 100% backing with cash and high‑quality liquid assets; segregation; no rehypothecation; monthly disclosures | GENIUS Act itself does not ban yield; Clarity Act would bar interest‑equivalent rewards on balances | Federal banking agencies and Federal Reserve; SEC/CFTC limited role for qualifying tokens | Enacted (GENIUS); Clarity Act advancing in Congress |

| United States (House proposals) | Waters’ bipartisan bill; STABLE Act | Depository and nonbank issuers with Fed’s central role; restrictions on Big Tech ownership | Strong reserve requirements; AML/CTF compliance; detailed conduct rules | Focus on closing loopholes and governance; yield to be shaped with Clarity Act | Federal Reserve, Treasury; preserves SEC, CFTC, CFPB authorities | Drafts advanced through committee; final form pending |

| United States (state example) | Florida Payment Stablecoin bill | Qualified payment stablecoin issuers licensed or exempt | To be detailed in rulemaking; integrated into state AML framework | Not specified in statute | Florida Office of Financial Regulation | Bill advancing; tied to parallel House measure |

| Hong Kong | Stablecoins Ordinance | Licensed issuers of fiat‑referenced stablecoins | Fully backed by high‑quality liquid assets; reserves held on trust and segregated; daily and weekly reporting | Interest and interest‑like incentives generally prohibited, except limited marketing incentives | Hong Kong Monetary Authority | In force since August 2025, with transitional period |

| Canada | Bill C‑15 (stablecoin provisions) | Stablecoin issuers registered with Bank of Canada | To be defined by regulation; likely full‑reserve model for systemically important issuers | Not yet specified | Bank of Canada maintains registry; broader oversight expected | Bill moving through Parliament; industry positioning ahead of framework |

This comparison highlights that fully backed reserves, segregation of assets, redemption rights, and strong AML/CFT controls are becoming global standards. Where jurisdictions diverge most is on yield and on the extent to which they welcome non‑traditional players like Big Tech and foreign issuers into their ecosystems. For stablecoin projects, these differences will increasingly influence decisions about where to base operations, how to design tokens, and which user segments to target.

What Stablecoin Bills Mean For Issuers, Users, And Crypto Markets

Impact On Centralized Issuers Like USDC And Tether

For centralized fiat‑backed stablecoins, the emerging legislation is both a constraint and an opportunity. Issuers that already maintain conservative reserves, publish attestations, and cooperate with regulators—such as those behind USDC‑style tokens—may find that laws like the GENIUS Act largely validate their existing business models, while providing much‑needed legal clarity and a level playing field. Being designated a permitted payment stablecoin issuer under federal or qualifying state regimes could become a badge of safety that strengthens institutional adoption, particularly if regulators and market participants treat GENIUS‑compliant stablecoins as acceptable collateral or settlement assets in a wider range of contexts. At the same time, these issuers will face higher compliance costs, more intrusive supervision, and constraints on their ability to experiment with yield or higher‑risk reserve investments.

For offshore issuers like Tether, US and allied stablecoin laws pose a more complex challenge. On the one hand, they may not be directly subject to all aspects of the GENIUS framework if they do not seek permitted‑issuer status or avoid certain US‑regulated activities. On the other hand, House bills and policy analyses explicitly target the “Tether loophole,” seeking to ensure that foreign issuers cannot sidestep US standards while enjoying access to US customers and financial infrastructure. As US and other major jurisdictions roll out licensing requirements, reserve standards, and extraterritorial measures tied to access to banking and payment systems, offshore issuers will be under pressure to either meet those standards or risk losing market share in regulated venues.

Market dynamics are already reflecting these pressures. Reports that Tether had secured a Big Four audit have been framed in part as efforts to demonstrate institutional‑grade transparency at a time when regulatory and investor scrutiny is rising, including around potential yield restrictions that could affect how issuers manage and profit from their reserves. Meanwhile, equity markets’ reaction to legislative developments—such as share‑price moves in firms closely tied to USDC—show that investors are actively reassessing the profitability and growth prospects of stablecoin businesses under new regulatory constraints, particularly regarding how much of the interest on underlying reserves can be retained by issuers versus passed through to users or used to fund ecosystem incentives.

Decentralized Stablecoins And DeFi Protocols

Decentralized stablecoins like DAI and FRAX occupy a more ambiguous position in the emerging legal landscape. Because laws like the GENIUS Act define payment stablecoins in terms of an identifiable issuer that maintains reserves and redemption rights, many decentralized designs may fall outside the core category of regulated payment stablecoins, at least formally. Instead, they may be treated as other types of digital assets, potentially subject to securities or commodities laws depending on their design and governance. The Clarity Act’s broader market‑structure provisions could bring some of these tokens and the protocols that manage them under SEC or CFTC jurisdiction, particularly if governance tokens or yield‑bearing features are deemed investment contracts.

Even if decentralized stablecoins are not directly regulated as payment stablecoins, they will be affected indirectly through constraints on centralized on‑ and off‑ramps, custodians, and exchanges. For example, House and Senate bills preserve the SEC’s and CFTC’s authority over broker‑dealers, exchanges, and market‑makers that facilitate trading or swapping of payment stablecoins and related assets, allowing these agencies to impose listing, disclosure, and conduct standards on platforms that support decentralized stablecoins. Similarly, stablecoin yield restrictions that apply to “interest‑equivalent” rewards could encompass centralized platforms’ DeFi‑staking or yield‑farming offerings, even if the underlying protocol remains technically outside direct US jurisdiction. Over time, major DeFi projects may need to design interfaces and user‑flows that segregate US and non‑US users, or that differentiate between compliant and non‑compliant stablecoin products.

At the same time, decentralized stablecoins may benefit from some of the pressures facing centralized issuers. If tightly regulated payment stablecoins are barred from paying yield or from engaging in certain forms of risk‑taking, and if offshore centralized options face mounting regulatory headwinds, demand could grow for decentralized alternatives that offer programmable yield backed by transparent on‑chain collateral. Policymakers are aware of this possibility, which is why some policy papers and commentaries have called for careful calibration of rules to avoid simply pushing risk into less regulated corners of the ecosystem. For builders, the key challenge will be to navigate a patchwork where some jurisdictions view decentralized stablecoins as innovative financial primitives and others as potential systemic risks to be constrained.

Custodians, Wallets, And Exchanges

Stablecoin bills also carry significant implications for custodial wallets, exchanges, and other intermediaries, which serve as the interface between users and the underlying tokens. The GENIUS Act imposes customer‑protection standards on entities that provide custody services for payment stablecoins, requiring them to segregate customer assets, avoid commingling, submit to supervision and regulation, and provide regular audited reports on fiat reserves backing the tokens they hold. These requirements mirror and in some cases go beyond existing obligations for broker‑dealers and investment advisers, emphasizing that stablecoin balances should not be treated as part of custodians’ own balance sheets or used as a source of unsecured funding.

House bills like Waters’ legislation also impose risk‑management and financial‑resource requirements on consumer wallet providers, along with backup examination and enforcement authority for the Federal Reserve, reflecting a recognition that wallets can become systemic nodes in a stablecoin‑based payments ecosystem. Exchanges and venues that facilitate trading or swapping of payment stablecoins are expressly subject to the continuing jurisdiction of agencies like the SEC and CFTC, ensuring that stablecoin bills do not displace existing market‑conduct rules for trading platforms. For centralized exchanges, this means that listing, margin, and lending products involving stablecoins will need to comply not only with general securities‑ or commodities‑law obligations but also with any specific restrictions on yield and use of customer stablecoin balances that flow from stablecoin legislation.

Non‑custodial wallets and decentralized interfaces may be less directly affected, but they, too, could come under increased scrutiny if regulators interpret them as intermediaries that “facilitate” stablecoin transactions at scale. Some stablecoin frameworks, such as Waters’ bill, explicitly include wallet providers among the entities subject to oversight when they meet certain thresholds or offer specific types of services, blurring the line between pure software and financial intermediation. As a result, wallet and interface designers may need to make conscious choices about whether to operate purely as open‑source software or to offer more integrated service stacks that include regulated custody and compliance functions.

Macro Implications: Treasuries, Banks, And Dollar Dominance

Finally, stablecoin bills have potential macroeconomic implications that extend beyond crypto markets. Because laws like the GENIUS Act require payment stablecoins to be backed 100 percent by cash and high‑quality liquid assets such as short‑term US Treasuries, widespread adoption of regulated stablecoins could generate substantial additional demand for government securities. Some policymakers and industry advocates have argued that this demand could reach into the trillions of dollars over time, effectively turning stablecoin reserves into a major new buyer base for US sovereign debt and reinforcing the dollar’s role as the dominant global currency in digital form. Others caution that such projections are speculative, but there is broad agreement that regulated stablecoins would deepen the integration between crypto markets and traditional money markets.

For banks, the picture is more mixed. On the one hand, if individuals and firms shift some of their transactional and savings balances from bank deposits into stablecoins, banks could face increased competition for low‑cost funding, especially if stablecoin yield products are allowed to pass through some of the interest earned on reserve assets. On the other hand, banks could also become key infrastructure providers for the stablecoin ecosystem by serving as custodians, reserve managers, and permitted payment stablecoin issuers, particularly if they obtain licenses under frameworks like GENIUS. The White House stablecoin yield report’s conclusion that a broad yield prohibition would do little to protect bank lending suggests that policymakers are wary of over‑protecting banks at the expense of innovation, but the ultimate balance between incumbents and new entrants will depend on how yield, access to Federal Reserve facilities, and other details are resolved.

From a dollar‑dominance perspective, stablecoin regulation is both an opportunity and a defensive move. Clear, robust US rules for dollar‑pegged stablecoins could cement the greenback’s position as the default currency of the internet, especially if US‑regulated tokens become the asset of choice for cross‑border payments, DeFi collateral, and tokenized real‑world assets. At the same time, if US rules are perceived as too restrictive or unpredictable, other jurisdictions’ frameworks—such as Hong Kong’s or Canada’s—could gain ground, and non‑dollar stablecoins might increase in relative importance. Policymakers are acutely aware of this dynamic, which is why legislative debates often frame stablecoin bills as tools not only for financial‑stability and consumer‑protection goals but also for maintaining or extending national currencies’ roles in digital finance.

The GENIUS Act imposes extraterritorial reach over foreign issuers like Tether, mandates full dollar backing and annual audits for large issuers, and creates a federal licensing regime that displaces state frameworks — compliance failure risks market exclusion.

Bank charter requirements and reserve mandates favor well-capitalized incumbents (Circle, Ripple, BitGo) and structurally disadvantage decentralized issuers like DAI and Frax that cannot hold Fed master accounts.

A yield ban on stablecoins would eliminate a core DeFi revenue stream and compress margins for exchanges offering savings products, while simultaneously boosting demand for U.S. Treasuries by forcing reserve requirements.

Full-reserve mandates reduce the ability of issuers to deploy capital productively, but the requirement to hold liquid, dollar-denominated assets also insulates holders from bank-run dynamics seen in algorithmic stablecoin collapses.

The GENIUS Act is primarily a regulatory and reserve framework targeting centralized issuers; on-chain smart contract risk for payment stablecoins is unaddressed by the legislation and remains a residual technical risk.

Key Open Questions And Fault Lines

Despite substantial progress, stablecoin bills leave several important questions unresolved. One is the precise perimeter of what counts as a regulated payment stablecoin. While laws like the GENIUS Act define this category with reference to an issuer’s redemption obligation and reserve backing, innovation in token design may blur these boundaries, for example through hybrid models that combine features of money‑market funds, tokenized deposits, and programmable cash. Regulators will need to decide how to treat such instruments, and whether to bring them under stablecoin frameworks, securities laws, or banking rules. The answer will shape not only compliance burdens but also how interoperable different forms of digital cash are allowed to be.

A second fault line concerns how to balance innovation, consumer protection, and national‑security objectives. Strong reserve, redemption, and AML requirements clearly address some of the risks highlighted by past crypto crises and concerns about illicit finance. Yet if regulations are too prescriptive or rigid, they may stifle experimentation with new forms of on‑chain credit, liquidity provision, and cross‑border payments that could deliver substantial efficiency gains. Policymakers’ responses to the stablecoin yield debate illustrate this tension: the White House yield report cautions against blanket prohibitions that would forgo consumer benefits, while banks push for tighter rules to avoid deposit‑like products outside their regulatory perimeter. Striking an appropriate balance will likely require iterative rulemaking and close dialogue between regulators and industry.

A third open question is whether stablecoin bills will reduce risk in the crypto ecosystem or simply push it into other corners, such as unregulated offshore tokens or complex DeFi structures. Legislators are acutely aware of the “Tether loophole” risk, and House proposals like Waters’ bill seek to close it by extending US standards extraterritorially where possible. Nevertheless, as long as global capital and code are mobile, there will be incentives for some actors to operate beyond the reach of major jurisdictions, especially if they can still access global liquidity through decentralized protocols. Policymakers must therefore complement stablecoin‑specific rules with broader international coordination and robust enforcement against illicit finance, while recognizing that some degree of regulatory arbitrage is inevitable in a global, open‑source environment.

Finally, there is the question of how stablecoin regulation interacts with other digital‑asset initiatives, such as central‑bank digital currencies (CBDCs), tokenized securities, and real‑world‑asset (RWA) protocols. In Canada, for example, the Bank of Canada’s role in maintaining a registry of stablecoin issuers sits in the same institutional space as potential future CBDC projects, raising questions about how private and public digital money will coexist. In Hong Kong, the stablecoin ordinance is part of a broader push to build a regulated virtual‑asset hub that could support tokenized bonds and other RWAs. In the United States, proposals around tokenized Treasuries and T‑bill‑backed stablecoins intersect with debates over stablecoin yield, reserve composition, and the role of Treasuries in stablecoin portfolios. As these adjacent domains evolve, stablecoin bills will need to be revisited and updated to keep pace.

Outlook

The near‑term trajectory for stablecoin bills points toward consolidation and implementation rather than radical new departures. In the United States, the GENIUS Act is now law, and attention is shifting to rulemaking by federal banking agencies, state‑federal coordination on permitted‑issuer regimes, and the final legislative negotiations over the Clarity Act’s yield provisions and the House’s STABLE and Waters bills. Industry participants should expect a multi‑year process in which agencies flesh out detailed capital, liquidity, disclosure, and technical‑control requirements, while Congress continues to fine‑tune issues like yield, foreign issuer treatment, and Big Tech’s role. For stablecoin issuers and service providers, early engagement with regulators and proactive alignment with the most conservative plausible standards will likely pay dividends in terms of licensure and market trust.

Globally, jurisdictions like Hong Kong and Canada will move from legislating to building out supervisory practices and industry ecosystems around their new frameworks. The HKMA’s consultations on guidelines, custody, and over‑the‑counter stablecoin services suggest that further refinement is coming, particularly around operational resilience and integration with existing financial infrastructures. Canada’s Bank of Canada‑centric model will evolve as regulations define reserve assets, redemption rights, and potential interactions with broader payments‑modernization and CBDC efforts. For firms with global ambitions, designing products that can comply with multiple regimes—some that ban yield, others that may allow it under conditions—will be a key strategic challenge.

For the crypto ecosystem, the most important takeaway is that stablecoins are being pulled decisively into the regulated core of the financial system. Fully backed, fully transparent payment stablecoins are likely to become more, not less, central to both crypto and traditional markets as laws and regulations clarify their status and responsibilities. At the same time, innovation around decentralized stablecoins, RWA‑backed tokens, and on‑chain yield will continue, shifting the frontier of experimentation into areas not yet fully addressed by stablecoin‑specific bills. The balance policymakers strike between safety and openness in these foundational laws will go a long way toward determining whether the next decade of crypto finance is characterized by compliant, institutional‑grade growth or by continued fragmentation between regulated and gray‑market liquidity.

Latest Stablecoin Bill news

Deloitte and Stablecorp build QCAD institutional payment rails as Canada advances stablecoin regulation via Bill C-15Even with DC gridlocked, momentum for crypto market structure reform has never been stronger — after bipartisan meetings on the Hill, both sides are 90% aligned, and Coinbase remains confident a clear DeFi and stablecoin bill could pass by year-end.Ripple, Circle, and BitGo are pursuing U.S. trust bank licenses amid regulatory shifts, as stablecoin bills like the Genius Act push crypto closer to traditional finance. Kraken eyes a debit card, while Robinhood and Revolut expand banking services. With the stablecoin bill passing the Senate, crypto is exploding (good exploding, not bad exploding).

With the stablecoin bill passing the Senate, crypto is exploding (good exploding, not bad exploding). US Senate schedules final GENIUS stablecoin bill vote for June 17

US Senate schedules final GENIUS stablecoin bill vote for June 17 Senate clears path for GENIUS stablecoin bill with 68–30 cloture vote, setting up final vote next week on measure requiring full dollar backing and annual audits for major issuers

Senate clears path for GENIUS stablecoin bill with 68–30 cloture vote, setting up final vote next week on measure requiring full dollar backing and annual audits for major issuersSources

- https://www.whitehouse.gov/fact-sheets/2025/07/fact-sheet-president-donald-j-trump-signs-genius-act-into-law/

- https://www.arnoldporter.com/en/perspectives/advisories/2025/07/new-stablecoin-legislation-analyzing-the-genius-act