Comprehensive explainer on the Winklevoss twins’ role in crypto, covering Gemini’s rise, IPO, regulatory battles, Bitcoin strategy, venture bets like Zcash and N3XT, and their growing influence in U.S. politics and digital‑asset regulation.

+8 sources across the wider coverage universe

3 ex-Signature Bank execs launch blockchain-powered narrow bank backed by Paradigm, Winklevoss. N3XT Bank operates under a Wyoming charter and opened its proverbial doors on Thursday.2025-12

3 ex-Signature Bank execs launch blockchain-powered narrow bank backed by Paradigm, Winklevoss. N3XT Bank operates under a Wyoming charter and opened its proverbial doors on Thursday.2025-12 Winklevoss Twins’ Gemini Exchange Faces Hard Landing Risk as Crypto Rout Squeezes Growth Plans and Stability2026-02

Winklevoss Twins’ Gemini Exchange Faces Hard Landing Risk as Crypto Rout Squeezes Growth Plans and Stability2026-02 Zcash privacy wallet ZODL raises $25M seed from Paradigm, a16z crypto, Winklevoss Capital and Coinbase Ventures for self-custodial ZEC development2026-03

Zcash privacy wallet ZODL raises $25M seed from Paradigm, a16z crypto, Winklevoss Capital and Coinbase Ventures for self-custodial ZEC development2026-03 Winklevoss-led Gemini to return over $1 billion to customers with a $37 million fine in agreement with NY regulator.2024-02

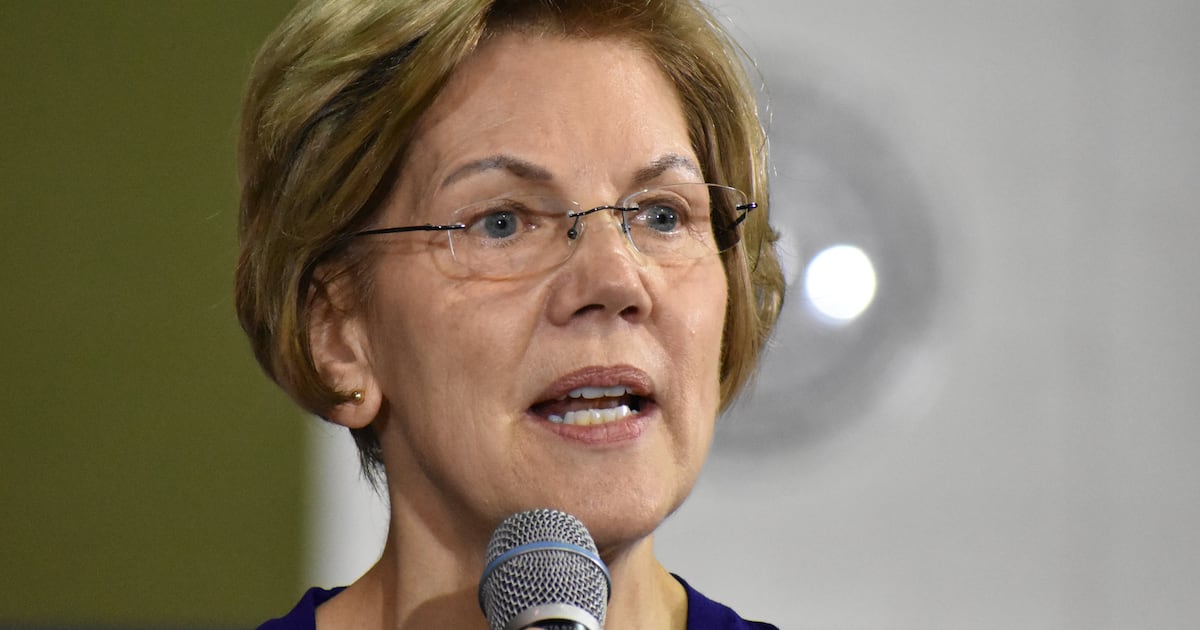

Winklevoss-led Gemini to return over $1 billion to customers with a $37 million fine in agreement with NY regulator.2024-02 Senator Elizabeth Warren rallies donors against crypto bosses like the Winklevoss twins, accusing them of sponsoring attack ads as her Massachusetts Senate race intensifies.2024-09

Senator Elizabeth Warren rallies donors against crypto bosses like the Winklevoss twins, accusing them of sponsoring attack ads as her Massachusetts Senate race intensifies.2024-09- Cameron Winklevoss, Co-founder of Gemini, publishes an open letter to CEO of DCG, alleging DCG knowingly lied to its counterparties2023-07

The Winklevoss Twins And The Making Of A Crypto Empire

The Winklevoss twins, Cameron and Tyler, are American investors best known in crypto for founding the Gemini exchange, becoming early Bitcoin billionaires, and evolving into high‑profile political donors and power brokers at the intersection of digital assets, regulation, and U.S. politics. Their trajectory from a Harvard startup dispute with Mark Zuckerberg to running a publicly listed exchange and funding pro‑crypto super PACs has made “Winklevoss” shorthand for both institutional crypto adoption and the controversies that come with it.

Who Are The Winklevoss Twins?

The Winklevoss twins are identical brothers born in 1981 who first entered the tech spotlight through their role in the early history of Facebook. Educated at Harvard, they co‑founded the social network ConnectU and later sued Mark Zuckerberg, alleging he had appropriated their concept to build Facebook. That dispute culminated in a settlement that left the brothers with a substantial payout, providing seed capital for the investment activities that would eventually propel them into the crypto industry.

Beyond technology, the twins also built an athletic resume that helped shape their public persona as disciplined, performance‑driven competitors. Both were accomplished rowers who represented the United States in international rowing competitions, including the Olympics, a background they frequently cite as formative for their approach to risk and persistence. This combination of elite academic credentials, high‑stakes litigation experience, and Olympic‑level sport produced a distinctive profile once they moved into Bitcoin and crypto investing. It also helped mainstream audiences recognize them as characters in the broader narrative of digital disruption, long before they launched their own exchange.

Their early experiences in traditional tech and finance shaped a particular view of how digital innovation should interact with regulation. The ConnectU saga, which played out in federal court and popular culture, introduced them early to the realities of legal process, intellectual property disputes, and public scrutiny. When they later turned to crypto, they did so with a pronounced emphasis on regulatory compliance and legal structure, a stance that set them apart from many early crypto entrepreneurs who were more inclined to avoid or challenge existing rules. This regulatory orientation became a defining feature of their flagship company, Gemini.

3 ex-Signature Bank execs launch blockchain-powered narrow bank backed by Paradigm, Winklevoss. N3XT Bank operates under a Wyoming charter and opened its proverbial doors on Thursday.

Readers click Winklevoss stories not for crypto mechanics but for the accountability-and-escape arc: the regulatory hammer that fell on Gemini, the political donations that may have softened it, and whether the IPO can paper over the losses underneath.↗

From Facebook Settlement To Bitcoin Pioneers

The settlement from the Facebook lawsuit provided the initial capital pool that supported the twins’ entry into early‑stage technology and crypto investments. Through their family office and venture vehicle, Winklevoss Capital, they began allocating funds into what they perceived as the next wave of the internet, ultimately converging on Bitcoin as a core conviction bet. While the exact timeline and size of their initial Bitcoin purchases are best documented in popular accounts rather than regulatory filings, by the mid‑2010s they were widely recognized as among the largest individual holders of Bitcoin, a status that earned them the label “Bitcoin billionaires” in both media and book‑length treatments.

This early positioning in Bitcoin was not merely passive investment. They became visible advocates for the asset, portraying it as “digital gold” and a hedge against monetary debasement, and publicly argued that Bitcoin’s upside remained significant relative to its perceived risk. Their role as both investors and promoters helped normalize the idea of institutional involvement in Bitcoin at a time when large financial firms were still skeptical. As prices appreciated over the years, on‑chain analytics would later estimate that their Bitcoin holdings generated paper profits in the billions, reinforcing their reputational status as among the most successful early adopters.

The creation of Winklevoss Capital in this period formalized their activities as technology investors and set the stage for a more structured approach to building in crypto. The firm’s portfolio, as described on its public materials, spans early bets on Bitcoin, Ether, and the Gemini exchange itself, alongside a range of other startups across the digital asset, fintech, and broader technology sectors. Rather than solely trading tokens, they positioned themselves as long‑term company builders and infrastructure investors, an approach that would later be reflected in their roles as founders and executives at Gemini, and as backers of projects such as Zcash Open Development Lab and the blockchain‑powered bank N3XT.

Building Gemini: From Regulated Exchange To Public Company

Founding Gemini As A New York Trust Company

Gemini, formally Gemini Space Station Inc., was founded in 2014 by Cameron and Tyler Winklevoss as a New York‑based cryptocurrency exchange and custodian. From the outset, Gemini emphasized regulatory compliance and institutional‑grade infrastructure, securing a trust company charter from the New York State Department of Financial Services (NYDFS) rather than operating under lighter regulatory regimes available in other jurisdictions. The company is headquartered in New York City and was structured to serve both retail and institutional clients with services that include trading, custody, and later credit card and yield‑style products.

The regulatory posture distinguished Gemini from many early crypto exchanges, some of which prioritized rapid growth over compliance. By pursuing a trust charter and operating under NYDFS oversight, Gemini subjected itself to capital, governance, and risk‑management requirements more akin to those applied to traditional financial institutions. This approach allowed the twins to position Gemini as a safer, more compliant alternative in a market often criticized for lax standards, and it paved the way for the firm to seek additional regulatory approvals in areas such as derivatives and clearing. However, it also meant higher fixed costs and exposure to intense regulatory scrutiny, dynamics that would later prove pivotal.

Gemini’s branding leaned heavily on the idea of a “regulated crypto exchange,” targeting both crypto‑native users who wanted secure custody and newcomers who were more comfortable with institutions vetted by traditional regulators. For several years, this strategy helped Gemini secure banking relationships, institutional clients, and a reputation as one of the more conservative large exchanges, even as competitors such as Coinbase grew larger in terms of trading volume and market share. The platform’s curated listing strategy and U.S. regulatory anchor reinforced the perception of Gemini as a bridge between the crypto frontier and mainstream finance.

Growth, Products, And The Earn Partnership

As the crypto market expanded through multiple bull cycles, Gemini broadened its product suite beyond simple spot trading. It added custodial services for institutional clients, interest‑earning products for retail, and eventually a crypto‑rewards credit card aimed at everyday users who wanted exposure to digital assets through spending. One of the most consequential offerings was Gemini Earn, a yield product that allowed customers to lend their crypto to institutional counterparties via the lending firm Genesis Global Capital in exchange for interest payments.

Earn was marketed as a way for users to put idle crypto assets to work, with Gemini acting as program sponsor and Genesis as the underlying borrower that generated yield. In practice, this structure embedded counterparty and duration risk familiar from traditional securities lending and structured products into a retail‑facing crypto service. As long as markets were rising and counterparties remained solvent, Earn functioned as intended. However, the program’s architecture would become a central vulnerability when the broader crypto credit system came under strain in 2022.

For Gemini, Earn represented an attempt to compete with other exchanges’ yield products without directly taking on the full credit exposure on its own balance sheet. Nevertheless, regulators later concluded that the way Gemini vetted and managed the relationship with Genesis, and the way it communicated risk to customers, fell short of expectations for a NYDFS‑regulated trust company. The unraveling of Earn illustrated the tension between offering competitive, yield‑bearing crypto products and maintaining the conservative risk posture implied by a bank‑like regulatory regime.

Earn Collapse, DFS Settlement, And SEC Dismissal

The contagion that followed the collapse of several large crypto firms in 2022 reverberated through the lending sector and ultimately brought down Genesis Global Capital, the borrowing counterparty in Gemini’s Earn program. When Genesis halted withdrawals in November 2022, Earn customers suddenly lost access to their funds, triggering a wave of complaints and regulatory scrutiny. Gemini faced simultaneous pressure from users, state regulators, and eventually the U.S. Securities and Exchange Commission (SEC), which alleged that Earn constituted an unregistered securities offering.

In February 2024, the NYDFS announced a settlement under which Gemini committed to return at least \( \$1.1 \) billion to Earn customers through the Genesis bankruptcy process and agreed to contribute an additional \( \$40 \) million into the bankruptcy estate for their benefit. As part of the consent order, Gemini also accepted a \( \$37 \) million fine for what NYDFS described as “significant failures” that threatened the safety and soundness of the company. A notable element of the settlement was that Gemini would not be forced to surrender its New York trust charter, allowing the firm to continue operating under state supervision.

In parallel, Gemini reached an agreement “in principle” with Genesis and other creditors that, once approved, would result in Earn users receiving 100% of their digital assets back in kind, with total value estimated at more than \( \$1.8 \) billion based on prices at the time of the announcement. This represented approximately \( \$700 \) million more than the assets were worth when Genesis halted withdrawals, reflecting the recovery in crypto markets during the delay. The SEC, which had filed a civil enforcement action against Gemini over Earn in 2023, ultimately moved in January 2026 to dismiss the case with prejudice, citing the full in‑kind return of customer assets and the state and regulatory settlements as reasons for exercising its discretion to end the litigation.

The combination of the NYDFS settlement and the SEC dismissal allowed Gemini to stabilize its regulatory footing after a period of severe uncertainty. However, the episode damaged the firm’s reputation as a conservative, risk‑managed platform and revealed how tightly intertwined even “regulated” exchanges can become with opaque crypto credit markets. The fact that Earn users ultimately recovered more than they initially deposited owed less to the original product design than to subsequent market appreciation and regulatory pressure, underscoring the structural risks that remain in yield‑bearing crypto offerings.

Gemini’s IPO: From Private Unicorn To Nasdaq Listing

Even as it navigated the Earn fallout, Gemini moved forward with plans to become a publicly traded company. In 2025, Gemini filed an amended registration statement with the SEC for an initial public offering (IPO) on the Nasdaq Global Select Market under the ticker GEMI. The filing proposed offering 16.67 million Class A shares at a price range of \( \$17 \) to \( \$19 \), with underwriters granted an option to sell an additional 2.5 million shares. At the top of the indicated range, the IPO targeted a valuation of up to \( \$2.22 \) billion, significantly below the company’s prior private valuation of \( \$7.1 \) billion achieved during the 2021 bull market.

When the listing arrived on September 12, 2025, Gemini’s IPO ultimately priced at \( \$28 \) per share, and the stock opened at \( \$37.01 \), implying a market capitalization of approximately \( \$3.3 \) billion. The firm thus debuted at a higher valuation than initially targeted in its filing, reflecting stronger than expected demand for exposure to a U.S.‑regulated crypto exchange despite lingering regulatory baggage. Gemini became the third U.S.‑listed centralized crypto exchange operator, following Coinbase’s high‑profile direct listing in 2021 and the listing of Bullish earlier in 2025, cementing the Winklevoss twins’ company as part of the public‑markets cohort of crypto infrastructure firms.

The underwriting syndicate for the offering included major Wall Street banks such as Goldman Sachs, Citigroup, Morgan Stanley, and Cantor Fitzgerald, along with Evercore ISI, Mizuho, and Truist Securities, among others. Their participation signaled that for mainstream capital markets, Gemini’s regulatory and reputational issues were manageable in light of its growth potential and the broader normalization of crypto as an investable sector. For the twins, the IPO created a liquid, publicly traded equity currency they could use for acquisitions, employee compensation, and capital raising, even as they retained dominant control through their share structure and voting rights.

Financial Performance As A Public Company

Gemini’s IPO filings and subsequent earnings reports reveal a company experiencing rapid revenue growth alongside heavy and persistent losses. For 2024, Gemini reported \( \$142.2 \) million in revenue but a net loss of \( \$158.5 \) million, reflecting the costs of compliance, infrastructure, and the fallout from the Earn program. Losses deepened in the first half of 2025, when the company generated \( \$67.9 \) million in revenue but recorded net losses of \( \$282.5 \) million, as operating and legal expenses remained elevated.

An SEC filing covering full‑year 2025 paints a more complete picture of the company’s scale and cost structure. Total revenue rose to \( \$179.6 \) million, up from \( \$142.2 \) million in 2024, driven by higher trading volumes, expanded services, and fast‑growing credit card revenue. At the same time, net loss widened sharply to \( \$582.8 \) million from \( \$158.5 \) million, as operating expenses surged to \( \$525.2 \) million and net other expense reached \( \$243.1 \) million, including substantial non‑cash crypto and related‑party items. These figures show a business still in heavy investment mode, bearing the costs of becoming and remaining a regulated, multi‑product platform in a volatile market.

By the first quarter of 2026, there were signs that Gemini’s revenue mix was shifting and that losses, while still large, were narrowing. The company reported \( \$50.3 \) million in revenue for the quarter ended March 31, 2026, representing 42% year‑over‑year growth. Services and interest income jumped 122% to \( \$24.5 \) million, while credit card revenue climbed 300% to \( \$14.7 \) million, indicating traction in non‑trading lines of business. The net loss for the quarter narrowed to \( \$109 \) million, an improvement from the \( \$141 \) million loss recorded in the same quarter of 2025, though still a substantial deficit.

A simplified snapshot of Gemini’s recent financial trajectory can be summarized as follows, based on reported figures:

| Period | Revenue (USD millions) | Net Income (USD millions) | Notes |

|---|---|---|---|

| Full year 2024 | 142.2 | −158.5 | Pre‑IPO, Earn fallout ongoing |

| First half 2025 | 67.9 | −282.5 | Rising legal and operating costs |

| Full year 2025 | 179.6 | −582.8 | Large non‑cash and related‑party items |

| Q1 2026 | 50.3 | −109 | 42% YoY revenue growth, loss narrowing |

These numbers position Gemini as a growth‑stage public company still searching for sustainable profitability, a dynamic common among crypto infrastructure firms that prioritize building multi‑product platforms over near‑term earnings. For investors and users, the key question is whether the exchange can leverage its regulatory status, brand, and new product lines quickly enough to justify ongoing losses while weathering crypto’s cyclical downturns.

Strategic Shift: Derivatives, Prediction Markets, And “Markets Company”

In addition to its spot trading, custody, and credit card business, Gemini has pursued a strategy of expanding into derivatives and prediction markets, framing this evolution as a transition from being a pure “crypto company” to a broader “markets company.” A significant milestone in this shift came when Gemini secured a Derivatives Clearing Organization (DCO) license from the U.S. Commodity Futures Trading Commission (CFTC), authorizing it to clear futures and options products. Cameron Winklevoss described this license as central to Gemini’s ambition to broaden its marketplace strategy and compete more directly in derivatives, a segment long dominated by incumbents in both crypto and traditional finance.

The company has also announced plans to enter the regulated prediction markets space, offering trading tied to the outcomes of sports events, elections, and other real‑world occurrences. In February 2025, Gemini combined this strategic pivot with a significant cost‑cutting initiative, including a roughly 25% reduction in its workforce and a wind‑down of operations in the United Kingdom, the European Union, and Australia. These moves were framed as efforts to increase productivity and manage expenses while repositioning the business toward higher‑margin, differentiated products, but they also signaled the difficulty of sustaining a global retail footprint amid regulatory complexity and intense competition.

The retreat from certain international markets created an opening for potential buyers interested in acquiring pieces of Gemini’s infrastructure and regulatory licenses. Reporting in 2025 indicated that unnamed parties were evaluating acquisitions of parts of Gemini Space Station, particularly its shuttered European and U.K. operations, as a shortcut to obtaining local licenses in those jurisdictions. While no definitive transactions have been publicly confirmed, the fact that such discussions were taking place underscored both the value of Gemini’s regulatory footprint and the financial strain that had led it to retrench geographically.

Winklevoss Twins’ Gemini Exchange Faces Hard Landing Risk as Crypto Rout Squeezes Growth Plans and Stability

- 01Gemini regulatory settlement fallout↗

The $1B customer return and $37M NY DFS fine was the single most-clicked story, signaling readers wanted to know who bore the cost of Gemini Earn's collapse.

- 02Warren political counterattack↗

The Elizabeth Warren fundraising campaign against Winklevoss-backed crypto PAC spending drew strong interest as a proxy battle over who controls crypto regulation.

- 03DCG and Genesis fraud accountability↗

Cameron's open letter accusing Barry Silbert of lying to counterparties framed the Genesis collapse as deliberate deception, pulling readers into the who-knew-what question.

- 04Trump orbit regulatory relief↗

The CFTC moving to withdraw Gemini's $5M penalty shortly after a $2M Trump campaign donation made the quid pro quo angle impossible for readers to ignore.

- 05Gemini IPO financial fragility↗

IPO filings revealing lower revenue and wider losses, combined with a hard-landing-risk framing, attracted readers skeptical of the exchange's profitability story.

- 06Voting control concentration post-IPO↗

The twins retaining 94.5% voting power after a $425M IPO signaled to readers that public shareholders get the risk but not the governance.

Regulatory And Legal History

DFS, SEC, And The Earn Precedent

Gemini’s regulatory journey has been unusually public and consequential for the broader crypto industry because of its New York trust charter and the high‑profile Earn collapse. The NYDFS consent order in 2024 detailed what the regulator described as governance and risk‑management failures related to the Earn program, including insufficient due diligence and oversight of Genesis and an inadequate understanding of the counterparty risks Earn customers faced. In response, Gemini agreed to remedial measures and the substantial financial commitments already described, positioning the settlement as a way to make customers whole and preserve its regulatory status.

The SEC’s separate case against Gemini over Earn focused on how the product was offered and whether it constituted an unregistered securities offering under federal law. By agreeing in 2026 to dismiss the action with prejudice, the SEC effectively acknowledged that the combination of state action, bankruptcy outcomes, and customer restitution addressed its main concerns, at least in this instance. The Commission’s filing noted that dismissal reflected the full in‑kind return of Earn investors’ crypto assets and the broader regulatory and bankruptcy settlements involving Gemini and Genesis.

This sequence of events is likely to be studied as a template for how U.S. regulators may handle future cases where yield‑bearing crypto products affect retail investors through complex relationships between exchanges and third‑party lenders. On one hand, aggressive enforcement by state and federal agencies pushed Gemini toward full restitution and structural reforms; on the other, regulators showed willingness to close cases once customers were made whole and the firm accepted substantial penalties. That mix of deterrence and pragmatism will inform how crypto platforms assess regulatory risk when designing new yield and lending products.

The CFTC Fraud Case And Vacated Penalty

Gemini’s interactions with the CFTC followed a different trajectory. The agency previously alleged that Gemini had made false or misleading statements related to a proposed Bitcoin futures contract, a case that culminated in a \( \$5 \) million civil penalty the firm paid in January 2025. However, by May 2025 the CFTC itself had reassessed the matter and joined Gemini in asking a federal judge to vacate the penalty. Court filings revealed that the agency’s Division of Enforcement had “resorted to inappropriate tactics” to bring the case and later to extract a settlement, raising concerns about internal processes and the fairness of the original enforcement action.

In light of those findings, the CFTC concluded that regulators should never have accused Gemini Trust Company of making false statements in the first place, a rare instance of an agency effectively disavowing its own prior case. At the time of the joint motion to vacate, it remained unclear whether the \( \$5 \) million penalty Gemini had already paid would be refunded. For the Winklevoss twins, the episode was significant not only because it potentially removed a blot from Gemini’s compliance record, but also because it fed into a broader narrative they and other industry participants have advanced about overreach and missteps by certain regulators.

The timing of the CFTC’s reversal intersected with political developments as well. Reporting indicated that Trump‑aligned figures in Washington saw the case as an example of prior administration hostility to crypto, while critics worried that the push to vacate the penalty reflected growing industry influence over regulatory appointments and enforcement priorities. Whatever the political interpretation, the legal outcome strengthened Gemini’s argument that some of the regulatory pressure it faced had been unjustified, even as other cases, such as Earn, revealed genuine compliance failures.

Political Donations, Super PACs, And Regulatory Optics

The Winklevoss twins’ increasing involvement in U.S. politics has further complicated perceptions of their regulatory battles. They have become major donors to pro‑crypto political action committees and super PACs, channeling significant sums—often denominated in Bitcoin—into efforts to elect candidates sympathetic to the digital assets industry. In early 2024, public filings showed that Fairshake, a large pro‑crypto super PAC, received \( \$4.9 \) million from Cameron and Tyler Winklevoss, contributing to a cash reserve of more than \( \$70 \) million. Fairshake backs candidates from both major parties who support what it frames as sensible, innovation‑friendly regulation of digital assets.

The twins have simultaneously pursued more overtly partisan efforts. In August 2025, Politico reported that they were committing \( \$21 \) million to a new super PAC called the Digital Freedom Fund, focused on supporting conservative candidates aligned with former President Donald Trump’s pro‑crypto agenda. Tyler Winklevoss stated that the group would identify and support “champions of President Trump’s crypto agenda in primary races and the midterm elections,” signaling an explicit alignment with a particular political faction. This marked a shift from their earlier positioning as relatively nonpartisan advocates for crypto innovation.

Their donations have extended to individual races as well. In 2024, Fox Business reported that the twins donated \( \$500{,}000 \) each in Bitcoin to the Commonwealth Unity Fund, a super PAC supporting John Deaton, a pro‑crypto lawyer challenging Senator Elizabeth Warren in Massachusetts. The same coverage noted that the twins had previously announced a \( \$2 \) million Bitcoin donation to Donald Trump’s presidential campaign, described by them as a move to end what they called the Biden administration’s “war on crypto.” Warren, a prominent critic of the digital assets industry, has used the twins as emblematic of “crypto bosses” funding attack ads and wielding outsized influence over policy debates.

This political activism has clear strategic implications. By helping to finance candidates who are likely to appoint and support crypto‑friendly regulators, the twins are attempting to shape the environment in which Gemini and their broader crypto investments operate. At the same time, the scale and partisanship of their donations raise concerns about regulatory capture and fairness, especially when juxtaposed with outcomes like the CFTC’s decision to walk back a penalty or the SEC’s decision to drop its Earn case after customer restitution. Whether viewed as legitimate political engagement or as an attempt to purchase leniency, their activities ensure that “Winklevoss” is now as much a political brand as a financial one.

Winklevoss Capital And The Investment Portfolio

Family Office, Venture Strategy, And Core Holdings

Winklevoss Capital functions as both a family office for the twins’ personal wealth and a venture capital vehicle for their technology investments. According to its public portfolio information, the firm has invested in foundational crypto assets such as Bitcoin and Ether, in the Gemini exchange itself, and in a range of startups across the digital asset ecosystem. The strategy emphasizes early‑stage bets on what they consider transformative technologies in the “information age,” with crypto and blockchain featuring as central themes rather than peripheral experiments.

This dual role—as both principal investor in Gemini and external backer of other projects—gives the twins a broad view of the crypto landscape and multiple levers of influence. For example, they can steer Gemini’s listing and product strategies in ways that complement or support portfolio companies, while those companies, in turn, can benefit from Gemini’s market access and brand. At the same time, the overlap between personal holdings, corporate governance, and venture investments introduces potential conflicts of interest, especially when related‑party transactions are material enough to appear in Gemini’s financial disclosures. Managing those conflicts transparently is an ongoing governance challenge.

The firm’s portfolio reflects a conviction that crypto infrastructure, privacy‑preserving technologies, and blockchain‑enabled financial services are still in early innings. By allocating to both base‑layer projects and application‑level companies, Winklevoss Capital attempts to capture value across the stack, mirroring the twins’ own journey from token holders to exchange operators and then to ecosystem investors. This positioning also creates multiple paths to benefit from favorable regulation and rising digital asset adoption, independent of Gemini’s specific fortunes.

Bitcoin As Treasury Asset And Strategic Signal

Among the twins’ holdings, Bitcoin remains the centerpiece, serving as both a long‑term store of value and a tactical instrument for corporate and political maneuvers. On‑chain data compiled by Arkham Intelligence and reported in 2025 showed that wallets linked to Winklevoss Capital moved about 1,750 BTC—valued at roughly \( \$130 \) million at the time—into Gemini hot wallets over the course of a week. Analysts interpreted the transfers as presumably preparatory for selling, though that had not been confirmed, and estimated that wallets associated with the twins still held over \( \$764 \) million worth of Bitcoin, with cumulative profits from their Bitcoin positions around \( \$1.8 \) billion.

These transactions were closely watched by traders because they offered a rare, data‑driven glimpse into how one of the largest Bitcoin‑holding family offices manages risk and liquidity. The fact that the twins were willing to move significant amounts of BTC onto an exchange suggested they were not purely “never sell” advocates, but rather active stewards of their holdings, willing to realize gains or rebalance exposure when conditions warranted. At the same time, Arkham’s estimate that they still retained hundreds of millions of dollars in Bitcoin underscored their ongoing conviction in the asset’s long‑term prospects.

Their use of Bitcoin as a corporate funding tool became even more visible in 2026, when Winklevoss Capital Fund invested \( \$100 \) million worth of Bitcoin into Gemini’s own shares. According to reporting, the fund purchased 7.1 million GEMI shares at \( \$14 \) per share, nearly triple the stock’s then‑recent market price around \( \$4.92 \). The announcement coincided with Gemini’s first‑quarter 2026 earnings release and sent the stock up more than 20% in after‑hours trading, as investors interpreted the move as a strong vote of confidence from the controlling shareholders. Tyler Winklevoss framed the investment as a response to what he described as the market’s significant undervaluation of Gemini and expressed belief that both the company and Bitcoin had substantial room to run.

Interestingly, on‑chain data showed that the twins’ relationship with Gemini as a trading venue and custody platform for their own Bitcoin was dynamic rather than static. After the earlier \( \$130 \) million transfer into Gemini, they later pulled funds back, withdrawing about \( \$42.77 \) million in BTC from the platform in April 2026. This pattern suggested that they use exchanges not merely as long‑term storage but as flexible liquidity hubs, deploying or retrieving Bitcoin as needed to support corporate actions, political donations, or portfolio reallocations. In aggregate, these moves underscore how tightly the twins’ personal Bitcoin strategy is interwoven with Gemini’s corporate trajectory and their broader public activities.

Venture Bets: Zcash, Privacy Tech, And N3XT Bank

Winklevoss Capital’s investment activity extends beyond Bitcoin and Gemini into more specialized corners of the crypto ecosystem. In 2024, Zcash Open Development Lab (ZODL), a group dedicated to advancing the privacy‑focused cryptocurrency Zcash, announced that it had raised more than \( \$25 \) million in seed funding. The round was led by prominent crypto venture firms Paradigm and a16z crypto, and included participation from Winklevoss Capital, Coinbase Ventures, Cypherpunk Technologies, Chapter One, and Maelstrom, among others. The financing was earmarked for building self‑custodial ZEC wallet infrastructure and tools to strengthen the Zcash ecosystem.

Following the funding announcement, ZEC, the native token of the Zcash network, climbed more than 8.8% over 24 hours to trade around \( \$215 \), amid a broader recovery in crypto markets. Shares of Cypherpunk Technologies, a ZEC‑focused treasury firm backed by the Winklevoss twins, rose 2.7% during the same period. This episode highlighted how the twins’ venture investments can intersect with token markets and public equities, creating multiple feedback loops between announcement‑driven sentiment, asset prices, and portfolio valuations. It also illustrated their willingness to back privacy‑centric projects despite evolving regulatory scrutiny of privacy coins.

Another notable investment was in N3XT, a blockchain‑powered bank launched by three former Signature Bank executives, including founder Scott Shay. Operating under a Wyoming special‑purpose depository institution (SPDI) charter, N3XT is structured as a full‑reserve bank, meaning each dollar on deposit is backed one‑for‑one by cash or short‑term U.S. Treasuries. The bank does not engage in traditional lending but instead focuses on offering instant, 24/7 business‑to‑business payments via blockchain rails for sectors including cryptocurrency, shipping and logistics, and foreign exchange. Winklevoss Capital joined investors such as Paradigm, HACK VC, and others in backing N3XT, signaling interest in next‑generation financial institutions that blend crypto technology with conservative balance‑sheet management.

These investments demonstrate a thematic throughline in Winklevoss Capital’s portfolio: infrastructure, privacy, and regulatory experimentation. By backing a SPDI‑chartered full‑reserve bank on one hand and a privacy‑coin development lab on the other, the twins are effectively hedging regulatory outcomes while betting that some combination of compliant fintech and robust on‑chain privacy will define the next phase of crypto adoption. The co‑investment with firms such as Paradigm, a16z crypto, and Coinbase Ventures further integrates them into the top tier of crypto venture capital networks.

Zcash privacy wallet ZODL raises $25M seed from Paradigm, a16z crypto, Winklevoss Capital and Coinbase Ventures for self-custodial ZEC development

Good jne here. Project is really got great backings

Gemini Earn halts withdrawals after Genesis freeze

Cameron open letter accuses Barry Silbert of fraud

Fairshake PAC receives $4.9M from Winklevoss twins

NY DFS orders $1B customer restitution, $37M Gemini fine

Winklevoss Capital injects $100M into Gemini ahead of IPO

CFTC moves to withdraw $5M Gemini penalty under Trump admin

Gemini IPO prices at $28/share; Nasdaq invests $50M; twins retain 94.5% vote

Gemini Versus Coinbase And The Exchange Landscape

Regulatory Positioning And Business Models

Gemini and Coinbase are often compared because both are U.S.‑based, regulation‑focused exchanges founded by early crypto believers who sought to build institutional‑grade platforms. Coinbase’s 2021 direct listing put it on the public markets earlier and at a larger scale, while Gemini remained private until its 2025 IPO. Both firms operate centralized order books, custody infrastructure, and increasingly diversified product suites that include staking, credit cards, and developer tools. However, differences in regulatory posture, listing strategy, and geographical focus have led to divergent trajectories.

Gemini’s choice to operate under a New York trust charter from early on subjected it to some of the strictest state‑level oversight in the U.S., while Coinbase initially followed a different licensing path, emphasizing money transmitter licenses and later pursuing federal clarity. This helped Gemini court institutions that valued the New York regulatory imprimatur but also amplified the consequences when things went wrong, as seen in the DFS consent order over Earn. Coinbase, for its part, has faced its own high‑profile disputes with the SEC over staking and token listings, illustrating that no major exchange is immune to regulatory friction.

Business‑model differences also matter. Gemini has leaned into a curated listing strategy, a focus on secure custody, and more recently, a push into derivatives and prediction markets via its DCO license and market pivot. Coinbase, by contrast, has achieved scale partly through a broader array of supported assets, international expansion, and vertical integration around custody, developer tools, and institutional prime brokerage. For investors evaluating the “Winklevoss” brand, these differences frame Gemini as a more narrowly focused, compliance‑intensive exchange still building out its competitive moats.

Scale, Revenue, And Profitability Challenges

In raw financial terms, Gemini remains significantly smaller than Coinbase and many global competitors, which shapes the risk‑reward profile for both its stock and its users. As noted earlier, Gemini generated \( \$179.6 \) million in revenue in 2025 and remained deeply unprofitable, with a net loss of \( \$582.8 \) million driven by high operating expenses and substantial non‑cash items. The first quarter of 2026 showed promising 42% year‑over‑year revenue growth and some narrowing of losses, but the firm still lost \( \$109 \) million in that quarter alone.

This scale gap has two main implications. First, Gemini’s ability to absorb shocks—whether regulatory fines, legal settlements, or market downturns—is more constrained than that of larger exchanges with multi‑billion‑dollar revenue streams. The Earn episode, for example, required significant capital commitments and may have constrained Gemini’s ability to invest aggressively in other areas. Second, competition on fees and spreads is intense, and smaller exchanges often struggle to match the depth and liquidity of larger venues while still covering fixed compliance and infrastructure costs.

On the other hand, Gemini’s smaller scale can also mean more room for growth if its strategic pivots pay off. The surge in services and credit card revenue in early 2026 suggests that the firm is gaining traction in non‑trading businesses that could have higher margins and more stable demand than transaction‑driven revenue. If derivatives and prediction markets mature into meaningful contributors, Gemini could yet evolve into a more balanced platform. However, the path to sustainable profitability remains uncertain and highly sensitive to crypto market cycles.

Strategic Niches: Credit Cards, Derivatives, And Prediction Markets

Where Gemini seeks to differentiate itself is in a combination of product categories that blend traditional finance features with crypto‑native mechanisms. Its crypto‑rewards credit card, which drove a 300% year‑over‑year jump in credit card revenue in Q1 2026, channels everyday spending into digital asset accumulation for users. This positions Gemini not only as a trading venue but as a consumer‑facing financial brand that can capture a share of payment economies, much as traditional banks monetize card and interchange businesses.

In derivatives, the newly acquired DCO license gives Gemini a foothold in an area that has historically been dominated by platforms such as CME in traditional finance and a handful of large offshore crypto exchanges. Being able to clear futures and options under CFTC oversight offers a regulated alternative for institutions that are wary of unregulated or lightly regulated derivatives venues. If Gemini can build meaningful order‑book depth and product variety, this could become a differentiator, though it will require substantial investment and competition against incumbents with entrenched liquidity.

Prediction markets represent a more experimental frontier. By seeking to offer regulated markets tied to the outcomes of sports events, elections, and other real‑world phenomena, Gemini is entering a space that overlaps with both financial derivatives and online betting. The regulatory environment for such products is complex, involving not just securities and commodities law but also gambling regulations at the federal and state levels. Success here would not only open a new revenue stream but also position Gemini at the forefront of tokenized information markets, potentially leveraging its exchange and clearing infrastructure in novel ways. Failure, conversely, could expose the firm to new regulatory risks and reputational challenges.

Hard‑Landing Risk And M&A Speculation

Even as Gemini tries to carve out these strategic niches, it faces what some analysts describe as “hard‑landing risk” if crypto markets remain weak or if regulatory costs continue to rise faster than revenues. The 25% workforce reduction and withdrawal from key international markets in early 2025 were clear signs that the company was under pressure to cut costs and refocus efforts. Those moves may have been necessary to preserve capital and stabilize operations, but they also limited growth options and reduced Gemini’s direct access to users in Europe and Australia.

Amid this retrenchment, reports emerged that potential buyers were evaluating acquisitions of parts of Gemini, particularly its shuttered operations in the U.K. and European Union, as a way to quickly secure regulatory licenses in those jurisdictions. While such transactions could generate one‑time cash inflows and allow Gemini to streamline, they also underline investor concerns about whether the company can independently achieve the scale and profitability needed to compete with larger exchanges over the long term. For the Winklevoss twins, decisions about asset sales, partnerships, or potential strategic combinations will be critical tests of their ability to steer Gemini through a more mature and competitive phase of the crypto exchange sector.

Politics, Culture, And The “Winklevoss” Brand

From “Bitcoin Billionaires” To Crypto Ambassadors

The twins’ story has been told and retold in books, films, and media narratives that cast them as emblematic figures of the digital age. The portrayal of their role in Facebook’s early days in popular culture, followed by coverage of their pivot into Bitcoin, cemented their reputation as both controversial and visionary. As early, high‑net‑worth adopters of crypto who later built a regulated exchange, they became convenient symbols for the promise and peril of digital assets—simultaneously embodying the idea of meritocratic wealth creation and the critique that new elites were simply replacing old ones.

In the crypto community, the twins have often acted as ambassadors, speaking at conferences, offering public price commentary, and engaging on social media to promote Bitcoin and digital asset adoption. Their messaging has typically emphasized themes of financial freedom, technological inevitability, and the need for regulatory clarity that allows innovation without sacrificing consumer protection. Over time, however, their public persona has shifted from that of relatively neutral evangelists to that of overt political actors, especially as their donations to Trump‑aligned and other conservative causes have grown.

Trump, MAGA, And The Crypto Lobbying Machine

The alignment with Donald Trump and the broader “MAGA” political brand marks one of the most significant recent evolutions in the Winklevoss narrative. By donating large sums in Bitcoin to Trump’s presidential campaign and to super PACs supporting Trump‑aligned candidates, the twins have effectively bet that a more sympathetic regulatory environment will emerge under leadership committed to undoing what they characterize as an anti‑crypto stance by the current administration. Their Digital Freedom Fund PAC is explicitly described as aiming to support “champions of President Trump’s crypto agenda” in both primaries and the midterms, indicating a long‑term commitment to shaping the Republican Party’s platform on digital assets.

At the same time, their contributions to Fairshake and other ostensibly bipartisan pro‑crypto groups show that they continue to invest in broad industry lobbying efforts. Fairshake’s large war chest and involvement in multiple Congressional races have made it a central vehicle for crypto’s push to influence legislation and regulatory oversight. By being among its biggest donors, the twins increase their visibility and influence within a coalition that includes exchanges, venture funds, and protocol foundations.

Opponents, including Senator Elizabeth Warren, have seized on the twins’ political spending as evidence that a small number of wealthy crypto executives are attempting to purchase favorable treatment and evade accountability. The juxtaposition of their political influence with regulatory outcomes—such as the CFTC’s move to vacate a penalty or the SEC’s decision to dismiss its Earn case—fuels narratives of soft corruption, even when official justifications for those outcomes are grounded in procedural or restitution‑related arguments. This tension between legitimate political participation and perceived regulatory capture is likely to remain a central theme whenever the name “Winklevoss” appears in future policy battles.

Market Commentary, Social Media, And Narrative Power

Beyond formal politics, the twins exert influence through their commentary on markets and technology. They are active on platforms such as X, where they discuss Bitcoin’s price action, macroeconomic conditions, and regulatory developments. When Bitcoin prices correct sharply, they often frame the moves as rare buying opportunities and reiterate long‑term bullish theses, a stance consistent with their own behavior of adding to their Bitcoin holdings after significant drawdowns, as recent reporting on Winklevoss Capital’s accumulation during price lows suggests.

Their comments can move sentiment, especially among retail traders and Gemini shareholders. The \( \$100 \) million Bitcoin‑funded share purchase by Winklevoss Capital that sent GEMI stock up more than 20% is a clear example of narrative and capital reinforcing each other. Likewise, on‑chain observations of large BTC transfers from their wallets to Gemini have sparked speculation about impending sales and influenced short‑term market psychology. In both cases, the twins’ actions and words operate as signals that traders parse for clues about broader market direction.

As the crypto ecosystem matures, the marginal impact of any single influencer or executive on global markets may diminish, but the Winklevoss name still carries weight, particularly in the U.S. context where Gemini is headquartered and their political activities are concentrated. Their narrative power derives not just from early adopter status, but from their roles as exchange operators, venture capitalists, and donors—positions that give them visibility into flows of both capital and regulation that most market participants do not have.

Gemini has faced simultaneous state (NY DFS $37M fine, $1B restitution order) and federal (CFTC $5M penalty) enforcement actions, with outcome now partly dependent on political relationships with the current administration.

Tyler and Cameron Winklevoss retain 94.5% of voting power in Gemini's post-IPO structure, concentrating all material governance decisions in two individuals with no meaningful shareholder check.

Gemini's IPO filing disclosed lower revenue and wider losses even during a bull cycle, and the exchange required a $100M capital injection from Winklevoss Capital to shore up its balance sheet.

The Genesis/DCG collapse wiped out Gemini Earn customers and triggered years of litigation, exposing Gemini's reliance on a single yield counterparty as a structural flaw.

Deep alignment with Trump-era crypto policy provides near-term regulatory tailwinds but creates binary risk if political winds shift, particularly given documented PAC spending and the CFTC penalty withdrawal optics.

Winklevoss Capital's cross-investments in portfolio companies that also interact with Gemini (N3XT Bank, Zcash ZODL) create potential conflicts of interest that public-market disclosure rules will now scrutinize.

Risk, Critique, And What “Winklevoss” Means For Crypto

The evolving meaning of “Winklevoss” in crypto circles reflects a blend of admiration, skepticism, and concern. Admirers view the twins as disciplined builders who chose the harder path of regulation and transparency rather than chasing easy growth in offshore jurisdictions. From this perspective, setbacks like the Earn collapse or the CFTC case are growing pains in the construction of a durable, regulated crypto financial system, and the willingness to return customer funds and invest personal capital into Gemini is evidence of long‑term commitment.

Critics, however, emphasize recurrent themes: concentrated control over a public exchange, as the twins retain overwhelming voting power; repeated regulatory lapses that contradict the image of pristine compliance; and aggressive political spending that appears designed to secure favorable treatment. Gemini’s ongoing losses and retrenchment from international markets raise additional questions about whether its compliance‑heavy model can compete with larger, more diversified rivals and leaner, more nimble platforms. The risk is that Gemini becomes a case study in how the costs of regulation, when combined with market volatility, can undermine the ambitions of even well‑capitalized founders.

At a more structural level, the twins’ story encapsulates the broader tensions of crypto’s integration into mainstream finance and politics. They illustrate how early adopters can turn technological foresight into vast wealth, how that wealth can be deployed to build regulated institutions and lobby for favorable rules, and how the same processes can invite legitimate scrutiny and backlash. For a crypto news audience, understanding “Winklevoss” is therefore not just about tracking the fortunes of a single exchange or pair of founders, but about grappling with the complex interplay between innovation, regulation, capital markets, and democracy that now defines the digital asset era.

Outlook

The future of the Winklevoss twins’ influence in crypto will depend on three interlocking trajectories: Gemini’s path to sustainable profitability, the regulatory climate for digital assets in the U.S., and the evolving role of money in politics. If Gemini can successfully build out its derivatives and prediction markets businesses, continue growing non‑trading revenue such as credit cards, and manage costs without further major regulatory setbacks, the exchange could mature into a stable, mid‑tier public company that justifies the twins’ recent \( \$100 \) million Bitcoin‑denominated bet on its stock. Conversely, prolonged losses, renewed enforcement actions, or another market downturn could force more drastic restructuring or strategic combinations, testing their resolve and control.

On the regulatory front, much will hinge on whether pro‑crypto political forces, including those backed by the twins, succeed in setting the agenda in Washington. A friendlier SEC and CFTC could accelerate product approvals and reduce enforcement pressure, but would not erase the need for robust risk management or the possibility of future crises like Earn. Meanwhile, privacy‑focused bets such as Zcash, and bank‑like experiments such as N3XT, will live or die on regulatory decisions that balance innovation against concerns about financial stability and illicit finance.

Politically, the twins are likely to remain central figures in debates over the influence of money—especially crypto money—in American democracy. Their support for Trump‑aligned candidates and outspoken criticism of perceived “wars on crypto” guarantee that they will continue to polarize opinion. Whether history ultimately views them as responsible institution‑builders, self‑interested oligarchs, or something in between will depend not only on their own actions, but on how effectively the crypto industry as a whole manages the risks it creates for users, markets, and the political system. For now, the “Winklevoss” name remains a shorthand for the promise and pitfalls of crypto’s collision with mainstream power.

Latest Winklevoss news

3 ex-Signature Bank execs launch blockchain-powered narrow bank backed by Paradigm, Winklevoss. N3XT Bank operates under a Wyoming charter and opened its proverbial doors on Thursday.Winklevoss Twins’ Gemini Exchange Faces Hard Landing Risk as Crypto Rout Squeezes Growth Plans and StabilityZcash privacy wallet ZODL raises $25M seed from Paradigm, a16z crypto, Winklevoss Capital and Coinbase Ventures for self-custodial ZEC development Bitcoin slipping under $90K has Cameron Winklevoss framing it as a rare buy window. Market stress, whale shorts, and ETF outflows continue to weigh on price action.

Bitcoin slipping under $90K has Cameron Winklevoss framing it as a rare buy window. Market stress, whale shorts, and ETF outflows continue to weigh on price action. Winklevoss-founded Gemini moves to enter prediction markets. The move would bring Gemini into the broader rush of financial firms entering the nascent industry developing around prediction markets, which offer a federally regulated way to bet on the outcome of sports games, elections and other events.

Winklevoss-founded Gemini moves to enter prediction markets. The move would bring Gemini into the broader rush of financial firms entering the nascent industry developing around prediction markets, which offer a federally regulated way to bet on the outcome of sports games, elections and other events. Gemini raised $425M in a heavily oversubscribed IPO, pricing shares at $28 each and capping proceeds despite demand exceeding supply 20x, giving the exchange a $3B valuation. The Winklevoss twins retain 94.5% voting power, ensuring tight control as Gemini joins Coinbase and Robinhood among public US crypto exchanges.

Gemini raised $425M in a heavily oversubscribed IPO, pricing shares at $28 each and capping proceeds despite demand exceeding supply 20x, giving the exchange a $3B valuation. The Winklevoss twins retain 94.5% voting power, ensuring tight control as Gemini joins Coinbase and Robinhood among public US crypto exchanges.Sources

- https://bitcoinfoundation.org/news/crypto-companies-news/winklevoss-twins-put-100m-into-gemini-shares/

- https://en.wikipedia.org/wiki/Gemini_(cryptocurrency_exchange)

- https://www.dfs.ny.gov/reports_and_publications/press_releases/pr202402282

- https://www.bankingdive.com/news/cftc-asks-judge-vacate-gemini-5-million-penalty-crypto-winklevoss-trump-quintenz/821325/

- https://www.politico.com/news/2025/08/20/winkelvoss-millions-crypto-super-pac-00516653

- https://blockworks.com/news/gemini-nasdaq-ipo-filing

- https://www.the-independent.com/us/money/tyler-cameron-winklevoss-crypto-fine-trump-b2984989.html

- https://www.winklevosscapital.com/portfolio

- https://en.wikipedia.org/wiki/Cameron_Winklevoss

- https://stocktwits.com/news-articles/markets/cryptocurrency/winklevoss-bitcoin-transfer-gemini-wallets-130m-btc/cZdosauRI73

- https://coinmarketcap.com/academy/article/zcash-dev-lab-raises-dollar25m-from-paradigm-and-a16z

- https://www.bankingdive.com/news/3-ex-signature-execs-start-blockchain-bank/807070/

- https://www.bankless.com/read/news/potential-buyers-evaluate-partial-acquisition-of-gemini-exchange-coindesk

- https://www.bloomberg.com/news/articles/2024-02-21/crypto-super-pac-fairshake-gets-4-9-million-from-winklevoss-twins

- https://www.stocktitan.net/sec-filings/GEMI/8-k-gemini-space-station-inc-reports-material-event-beed5d470378.html

- https://www.sec.gov/enforcement-litigation/litigation-releases/lr-26465

- https://bitcoinmagazine.com/news/gemini-stock-jumps-after-winklevoss-twins

- https://fortune.com/crypto/2024/02/28/winklevoss-gemini-genesis-adrienne-harris-dfs-silbert-dcg/

- https://www.foxbusiness.com/politics/winklevoss-twins-donate-1m-bitcoin-senator-warren-pro-crypto-challenger

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…