Deep dive explainer on Fraxtal, Frax Finance’s OP Stack Layer 2 for stablecoins and DeFi, covering architecture, FXTL points, FRAX/FXS tokenomics, governance, security, Leviathan SQUID, and key ecosystem protocols like Fraxlend, Velodrome, Boardwalk, and IQ AI.

- x.com20

- app.frax.finance2

- coindesk.com1

- platform.spotonchain.ai1

- gov.frax.finance1

- curve.convexfinance.com1

- fraxscan.com1

+1 sources across the wider coverage universe

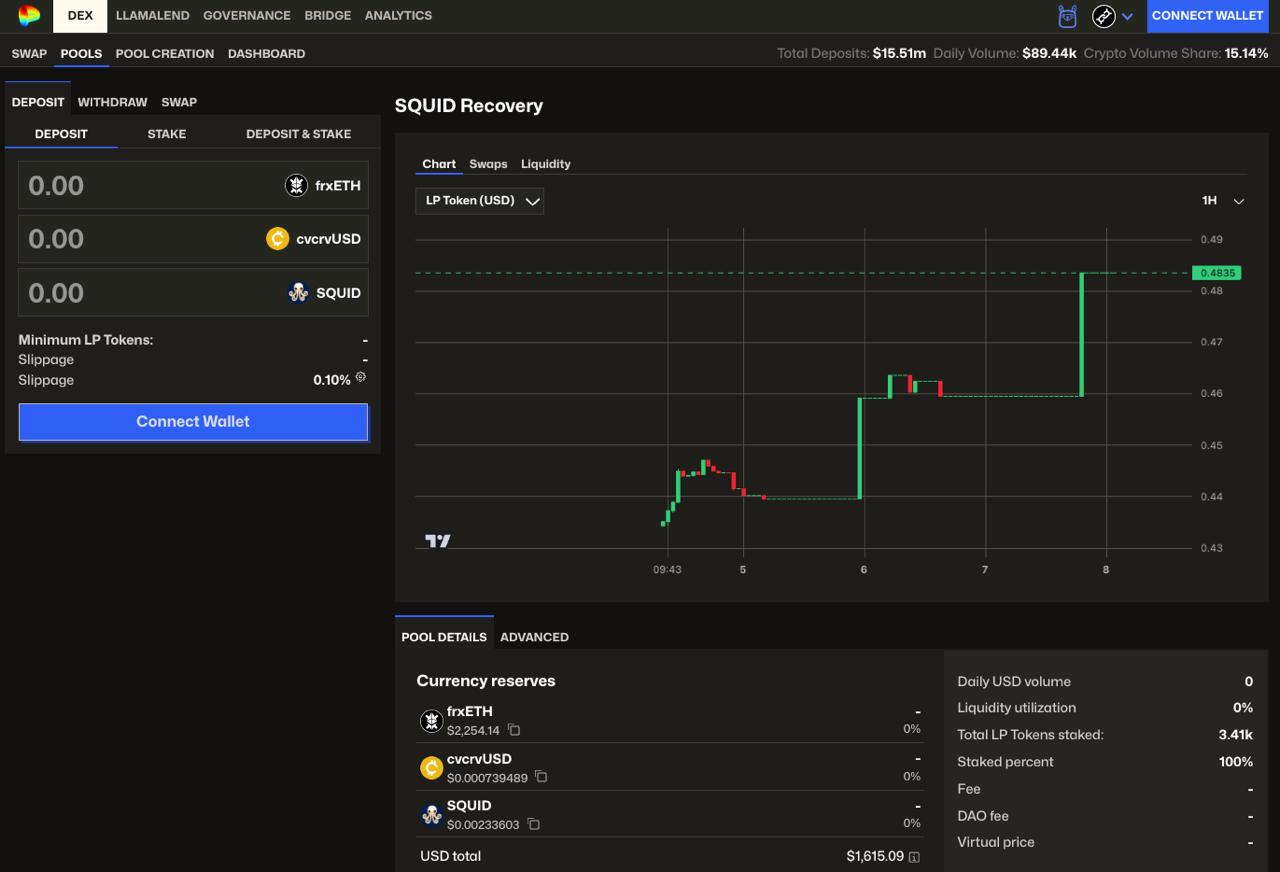

Leviathan SQUID DAO launches recovery pool for lenders affected by Llama Lend bad debt on Fraxtal2026-04

Leviathan SQUID DAO launches recovery pool for lenders affected by Llama Lend bad debt on Fraxtal2026-04 Curve DAO voting opens on the SQUID Recovery pool on Fraxtal2026-05

Curve DAO voting opens on the SQUID Recovery pool on Fraxtal2026-05 Convex adds support for Curve pools on Fraxtal chain, the third sidechain supported after Arbitrum and Polygon2024-03

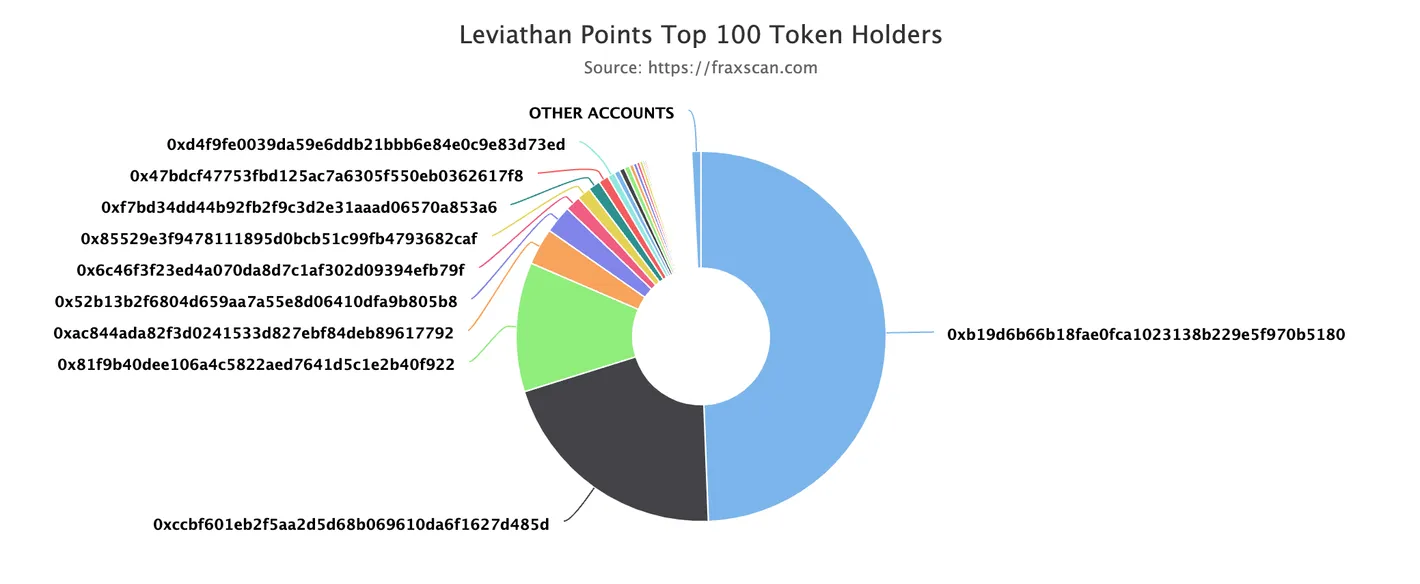

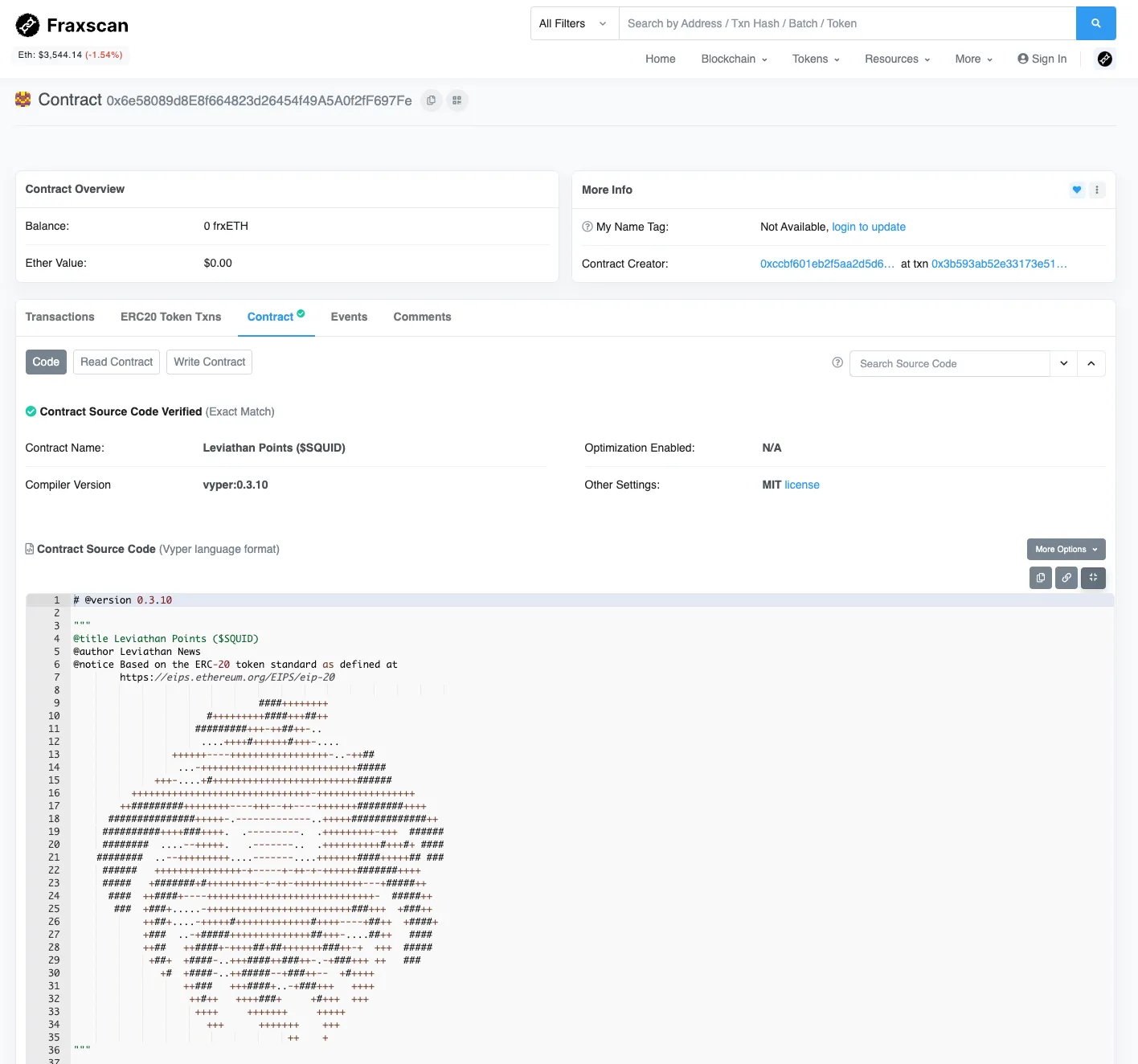

Convex adds support for Curve pools on Fraxtal chain, the third sidechain supported after Arbitrum and Polygon2024-03 Leviathan Points ($SQUID) first airdrop live. Check your wallet to confirm on Fraxtal:

0x6e58089d8e8f664823d26454f49a5a0f2ff697fe

Thanks for your help in building Leviathan!2024-04

Leviathan Points ($SQUID) first airdrop live. Check your wallet to confirm on Fraxtal:

0x6e58089d8e8f664823d26454f49a5a0f2ff697fe

Thanks for your help in building Leviathan!2024-04 Leviathan Points contract ($SQUID) deployed to Fraxtal, triggering fevered rush to gain eligibility2024-03

Leviathan Points contract ($SQUID) deployed to Fraxtal, triggering fevered rush to gain eligibility2024-03 veFXS is live for Fraxtal2024-04

veFXS is live for Fraxtal2024-04

Fraxtal: A Frax-Native Layer 2 for DeFi

An Ethereum Layer 2 built on the Optimism stack, Fraxtal is a modular rollup chain designed by Frax Finance to concentrate its stablecoins, staking products, lending markets, and liquidity infrastructure into a single, high-throughput DeFi hub. It combines full EVM equivalence with a novel blockspace incentive and points system, aligning the chain’s growth with Frax’s broader token and governance roadmap.

What Is Fraxtal?

Fraxtal is an EVM-equivalent optimistic rollup that runs as a Layer 2 on Ethereum, constructed using the OP Stack (Bedrock) and designed to feel like a familiar Ethereum environment for both developers and users. In practice, this means that contracts deployed on Ethereum mainnet can generally be deployed on Fraxtal with minimal or no changes, while transactions are executed off-chain by Fraxtal’s sequencer and settled periodically to Ethereum. Fraxtal was conceived as the “operating system” for the Frax ecosystem, providing a dedicated blockspace substrate for the protocol’s stablecoins, ETH staking products, automated market makers, and lending markets. Rather than being a generalized L2 without a native economic focus, Fraxtal is intentionally specialized around the Frax monetary stack and the protocols that build on top of it.

Frax Finance, founded by Sam Kazemian, began as one of the earliest algorithmic or partially algorithmic stablecoin experiments, gradually evolving into a more conservative, fully collateralized, and multi-asset protocol. Over time, Frax expanded from a single stablecoin into a family of products including dollar-pegged assets, ETH staking (frxETH), lending (Fraxlend), and other subprotocols. Fraxtal is the culmination of that evolution: an execution environment designed to host and coordinate these products natively, rather than relying solely on external chains and liquidity venues. In interviews and governance documents, the Frax team has framed Fraxtal as the missing piece that completes Frax’s “core product offerings,” allowing the protocol to express its monetary policy and incentive design directly in blockspace.

At launch, Fraxtal adopted frxETH, Frax’s liquid staking–style ETH derivative, as its native gas token, aligning transaction fees with the protocol’s own ETH staking system rather than with raw ETH. This design created a tight feedback loop between the use of Fraxtal, demand for blockspace, and demand for frxETH liquidity. Over time, Frax governance has moved toward an even deeper integration by proposing that the Frax governance token (formerly FXS) itself be rechristened as FRAX and become the gas token on Fraxtal, replacing frxETH. This “North Star” upgrade positions Fraxtal not only as a host chain for Frax assets but also as the primary venue where the Frax token accrues value via gas fees, staking, and emissions.

Crucially, Fraxtal is not just “another OP-chain.” The chain’s design is tightly bound to a blockspace incentive system called FXTL, often referred to as a “point system” that tracks and rewards on-chain activity at the contract level. Rather than treating transaction fees as purely a user cost, Fraxtal recycles a portion of value back to apps and users based on their contribution to network usage, with FXTL points intended to be tokenized within a defined timeframe after genesis. In combination with emissions of the Frax token itself under the North Star monetary schedule, this creates a layered system where blockspace consumption, liquidity provisioning, and governance participation are all financially interconnected.

From a user perspective, Fraxtal aims to function as the default home for the Frax ecosystem: the place where stablecoins like frxUSD, staking vaults like sfrxUSD, and lending pairs via Fraxlend live closest to their source and enjoy the tightest integration. Early ecosystem developments, such as the launch of Velodrome’s DEX infrastructure with a dedicated Fraxtal incentive program and the deployment of Fraxlend markets with fxb (fixed-maturity) pairs, have reinforced this identity as a DeFi-first chain. As the ecosystem matures, Fraxtal’s success will depend on whether this specialization can attract sufficient external capital and builders to make it not only the “pillar” of the Frax protocol, but also a competitive venue within the broader Layer 2 landscape.

Leviathan SQUID DAO launches recovery pool for lenders affected by Llama Lend bad debt on Fraxtal

Great. As a squid holder, news contributor & voter, I'm happy that Leviathan is restoring faith in its community. It's very unfortunate that the bad debt incident occur.

Fraxtal readers are driven primarily by personal financial stake — airdrops, token eligibility rushes, and recovery pools dominate clicks over technology or ecosystem announcements, revealing that Fraxtal's traction is inseparable from its incentive layer rather than its L2 infrastructure merits.↗

Architecture and Rollup Design

Technically, Fraxtal inherits many of its core properties from the OP Stack, the technology powering Optimism and a growing family of “Superchain” rollups. The OP Stack’s optimistic rollup design allows Fraxtal to execute transactions off-chain while posting compressed data and periodic state roots to Ethereum, enabling cheaper and faster transactions than on L1 while still inheriting Ethereum’s security model for final settlement. In an optimistic rollup, transactions are assumed to be valid unless proven otherwise, and the system relies on a challenge mechanism during a designated window to catch fraudulent state commitments.

On Fraxtal, as with other OP Stack chains, deposits from Ethereum to the Layer 2 are handled through a canonical bridge built on contracts like the L1StandardBridge and L1CrossDomainMessenger. When users deposit assets, including ETH or ERC-20 tokens, those deposits are batched into L2 blocks that correspond to particular L1 “epochs,” and become available on Fraxtal once included in the canonical chain. Withdrawals in the other direction follow a three-stage process: initiation on L2, proof submission to L1 once a new output root is posted, and finalization after the challenge period elapses. This model introduces a characteristic seven-day delay for native withdrawals on mainnet, a property that has led to a flourishing ecosystem of third-party bridges and messaging systems aiming to provide faster exits.

Fraxtal’s architecture layers its own economic design on top of this shared rollup foundation. Initially, the chain used frxETH as its gas token, meaning that the unit in which users paid transaction fees was itself a derivative representing staked ETH in the Frax system. This choice effectively turned gas consumption into a demand driver for Frax’s staking program, since frxETH is paired with sfrxETH, an interest-bearing staking token, in the Frax ETH product suite. As governance shifted toward the North Star vision, however, Frax proposed to transition gas to the Frax governance token (rebranding FXS as FRAX) and introduce a structured inflation schedule in which annual emissions start at approximately 10% and decay by 0.7 percentage points each year over a decade until reaching a 3% floor. These emissions are earmarked for DAO operations, team incentives, community and liquidity programs, veFRAX stakers, and conversions of FXTL points into FRAX, embedding the rollup directly into the protocol’s tokenomics.

Because Fraxtal is fully EVM-equivalent under OP Bedrock, it can support tools, libraries, and wallets that already work with Ethereum and other OP-based chains. Thirdweb, for example, exposes Fraxtal as an EVM-equivalent chain and allows developers to deploy contracts via familiar workflows, while its bridge interface lets users move assets like frxETH onto Fraxtal by selecting a source chain, token, and destination and delegating the cross-chain transfer to a bridging backend. The chain’s compatibility has also made it a natural target for infrastructure providers like Alchemy and various wallets to add support, reducing the friction for both new and existing DeFi applications to experiment with the Fraxtal environment.

Security for Fraxtal is ultimately anchored in Ethereum, but the chain’s specific risk profile also depends on its sequencer design and any potential upgrade authority exercised by the Frax DAO. Like other optimistic rollups, Fraxtal relies on a challenge window—currently envisioned as a week on mainnet-equivalent networks—during which erroneous or malicious state roots can be contested, preventing invalid withdrawals from finalizing. This architecture places a premium on off-chain monitoring and on the integrity of the code that posts roots to Ethereum. In addition, any centralized or multisig-controlled upgrades to the OP Stack contracts or Fraxtal’s own system contracts introduce governance and operational risk until the chain achieves a higher degree of permissionless control.

From an architectural standpoint, Fraxtal’s most distinctive innovation is not in consensus or execution, but in how it treats blockspace as a programmable, incentivized resource. By measuring and rewarding contract-level activity through FXTL points, and by designing emissions of the Frax token to flow to both governance stakers and active participants in the Fraxtal ecosystem, the chain attempts to knit together the economic fabric of its applications, liquidity providers, and governance process. This philosophy, combined with the shared OP Stack base, positions Fraxtal as something akin to a “monetary rollup” where economic policy and technical infrastructure evolve together.

The Frax Ecosystem on Fraxtal

To understand Fraxtal’s role, it is useful to map the Frax product suite and see how these components can be re-centered on a dedicated Layer 2. Frax USD began as an algorithmic/partially collateralized stablecoin but has evolved into a fully collateralized system with multiple representations, including frxUSD and its staked vault, sfrxUSD. The sfrxUSD vault is structured as an ERC-4626 token that distributes protocol yield to stakers, with shares denominated in frxUSD, effectively turning sfrxUSD into a yield-bearing stablecoin. On Fraxtal, these stablecoins become native settlement assets for DeFi, powering everything from AMM pairs and lending markets to launchpad-style token economies.

One early example of this integration is Boardwalk, a token economy and launch platform that has deployed on Fraxtal with support from the frxUSD stablecoin. In public communications, Frax has framed frxUSD as “the best stablecoin for DeFi economies,” emphasizing that its integration with Boardwalk allows value generated by token launches and economic activity to be routed back to the underlying projects as they grow. In this framing, Fraxtal serves as the settlement and execution environment in which Boardwalk’s token economies live, while frxUSD provides the numeraire for pricing and liquidity. Such arrangements illustrate Fraxtal’s potential to become a specialized environment where project launches, stablecoin infrastructure, and yield mechanisms can be tightly coupled.

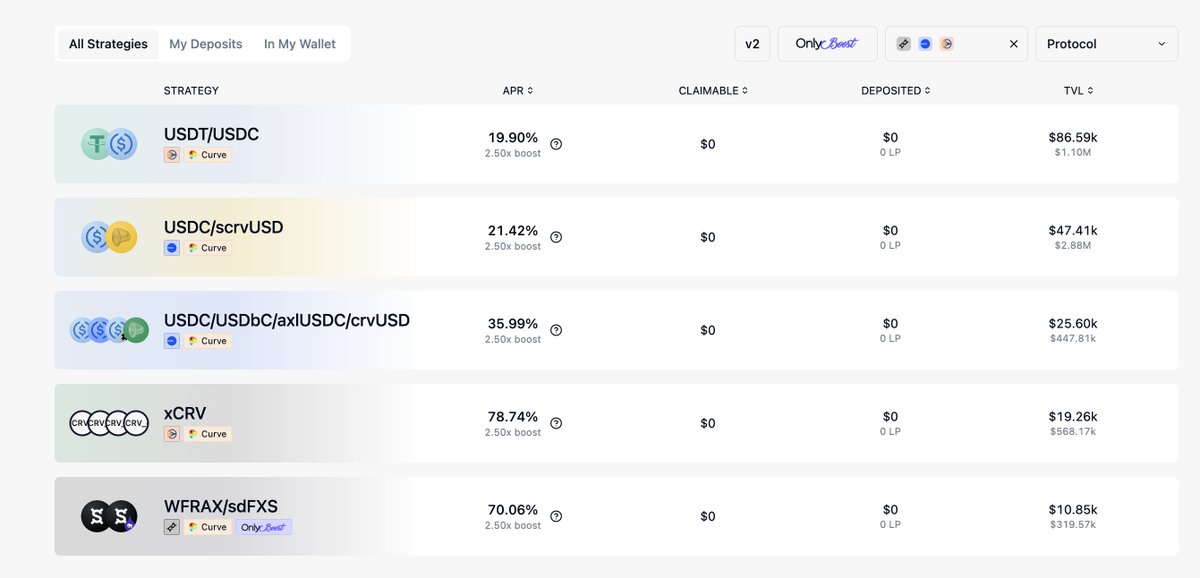

Lending is another critical pillar of Fraxtal’s ecosystem. Fraxlend, the Frax-native lending protocol, is built around pairwise markets: each lending pair is deployed as a separate contract instance managed by a factory and tracked in a pair registry. This architecture allows bespoke risk parameters and interest rate curves for specific asset pairs, rather than a monolithic pool model. On Fraxtal, Fraxlend has deployed markets including those that reference fxb, Frax’s fixed-maturity, bond-like instruments, allowing sophisticated duration and yield strategies tailored to the Frax monetary system. By consolidating Fraxlend activity on Fraxtal, the protocol can more easily coordinate incentives, monitor risk, and integrate lending with other chain-native primitives like AMMs and staking.

For spot and liquidity management, Fraxtal has attracted external DEX infrastructure, most notably Velodrome, a ve(3,3)-style automated market maker originally built on Optimism. A Frax governance proposal sought to allocate roughly one million dollars’ worth of incentives to support Velodrome’s expansion on Fraxtal, with funds earmarked as voting incentives that, by Velodrome’s design, translate into amplified VELO rewards for liquidity providers. The expectation was that each dollar of voting incentives would generate approximately 1.5 dollars of VELO emissions for LPs, effectively bootstrapping deep liquidity in key Frax pairs such as FRAX–ETH, frxETH–ETH, and various stablecoin and governance token combinations. By hosting Velodrome as a primary DEX, Fraxtal leans into a liquidity model that is highly compatible with vote-escrowed tokenomics and gauge-based emissions—an approach that dovetails with veFXS/veFRAX and FXTL-based incentives.

On top of lending and AMMs, yield aggregators and optimizers are beginning to integrate Fraxtal, promising to turn native yields into simpler products for end users. Beefy Finance, a multichain yield optimizer that offers auto-compounding “vaults” for LP and single-asset positions, has signaled plans to support Fraxtal, positioning itself to wrap Fraxtal-native yields into automated strategies. Because Fraxtal concentrates Frax’s own incentive programs and protocol rewards, such integrations could significantly increase the chain’s attractiveness for yield-focused users, though they also layer additional smart contract and strategy risk on top of core protocol risk.

Fraxtal has also become a deployment venue for more experimental or emerging categories of protocols, including AI-driven DeFi systems. IQ AI, built on Fraxtal, describes itself as an Agent Tokenization Platform (ATP) that allows developers to create tokenized AI agents capable of autonomously managing assets, executing strategies, and interacting with decentralized economies. The platform is powered by the IQ token, which serves as both the fee token for ATP usage and the governance token for the system, with each tokenized agent paired against IQ. Fraxtal’s low fees, EVM equivalence, and DeFi-centric user base make it a logical environment for such DeFAI experiments, in which AI agents need continuous, inexpensive access to on-chain data and trading venues.

Ecosystem development on Fraxtal has been encouraged not just through token incentives but also through structured programs like the Fraxtal Hackathon 2024, organized in partnership with DoraHacks. The hackathon’s stated vision is to transform the DeFi landscape on Fraxtal by fostering restaking-based architectures and “robust and flexible” DeFi primitives that leverage the chain’s modular rollup design. Events of this kind are often less about short-term TVL growth and more about seeding a developer culture around the chain, encouraging builders to treat Fraxtal as a first-class environment rather than an afterthought deployment.

Beyond the Frax-native stack, Fraxtal is steadily integrating into the broader DeFi and L2 infrastructure network. Curve Finance has introduced pools and strategies that touch Fraxtal, including recovery and incentive structures coordinated with DAOs like Leviathan’s SQUID DAO, while Stake DAO and Convex have provided yield and governance aggregation across Frax-related assets such as cvxFXS and associated point airdrops. Bridges and cross-chain messaging protocols are working to reduce friction in moving assets like crvUSD and Frax stablecoins between Fraxtal, Ethereum, and other L2s, with designs like FastBridge specifically targeting the seven-day withdrawal delay inherent in native optimistic rollup bridges by using off-chain messaging and liquidity provisioning to provide near-instant exits. These developments highlight Fraxtal’s dual identity: it is both a specialized chain for the Frax ecosystem and a node in a larger multi-chain DeFi graph where liquidity and users flow continuously.

- 01SQUID airdrop eligibility rush↗

The deployment of the $SQUID contract and subsequent live airdrop generated the two highest click counts, signaling readers tracked Fraxtal primarily as the chain hosting a claimable token event.

- 02DeFi protocol expansion↗

Convex, Velodrome, Fraxlend, and Beefy all deploying to Fraxtal drew sustained reader interest as each arrival signalled whether the chain was attracting real liquidity infrastructure.

- 03veFXS and tokenomics shifts↗

veFXS going live and the North Star rebranding of FXS as the native gas token pulled readers tracking how governance power and token value accrual would evolve on Fraxtal.

- 04Frax Singularity roadmap↗

Sam Kazemian's unveiling of future L3s, FPIS merger, and native Frax minting attracted readers seeking a forward-looking thesis on whether Fraxtal was a destination or a stepping stone.

- 05Institutional staking signal↗

Brevan Howard Digital staking over 1% of FXS supply ahead of launch gave readers a credibility signal they used to assess whether the chain had serious backing.

- 06Security incidents and bad debt recovery↗

The dTrinity swap adapter exploit and the Llama Lend bad debt recovery pool showed readers that Fraxtal's growing DeFi stack carried real smart-contract and credit risk they needed to monitor.

Token Economics, FXTL, and the Role of Points

The economic model around Fraxtal revolves around three intertwined components: the Frax token (governance and gas), the Frax stablecoin family (monetary base), and FXTL points (blockspace incentives). Understanding how these elements interact is crucial for evaluating Fraxtal’s long-term sustainability and the behavior it encourages from builders and users.

Historically, FXS served as the governance and value accrual token for the Frax protocol, with holders able to lock FXS for up to four years to receive up to four times the amount of voting-escrowed veFXS. This veFXS system, inspired by Curve’s veCRV design, tied governance power and yield boosts to time-locked commitments, rewarding long-term alignment with the protocol. With the North Star roadmap, this mechanism is evolving into veFRAX, reflecting the rebranding of FXS into FRAX as the governance and gas asset of the Frax ecosystem, and extending its reach into Fraxtal-specific dynamics. In practice, veFXS/veFRAX holders are positioned to be the primary beneficiaries of Fraxtal’s growth, both through direct emissions and through point-based airdrops.

The North Star proposal sketches a detailed emission schedule and allocation for the FRAX (formerly FXS) token once it becomes Fraxtal’s gas asset. Annual emissions are set initially around 10% of supply, declining by 0.7 percentage points per year over a decade to a terminal rate of approximately 3%. These emissions are split across categories such as the Frax DAO (for grants, audits, partnerships), team incentives and expansion, community programs including liquidity incentives and boosts for internal Frax projects, base emissions for veFRAX stakers, and conversions from FXTL points into FRAX. This structure effectively turns FRAX into both the “fuel” of the Fraxtal network and the reward currency for those who help secure and grow it, with veFRAX locks acting as a central gating mechanism for governance and boosted earnings.

FXTL, the Fraxtal point system, occupies a different but complementary role. According to Frax documentation, FXTL points are awarded to participants based on their on-chain activity on Fraxtal, including creating and interacting with smart contracts. These points are designed to be accrued by both users and protocols, making FXTL a contract-level metric of engagement and blockspace consumption rather than a simple per-address loyalty score. In community-oriented commentary, FXTL has been compared to “recurring incentives for usage and block space consumed,” highlighting that it is meant to track the ongoing contribution of apps and users to the chain rather than serve as a one-off airdrop mechanism.

One key feature of FXTL is its explicit pathway to tokenization. Frax-aligned commentary has stated that the FXTL or “FLOX” incentives will be tokenized no later than twelve months after Fraxtal’s genesis, with the point system serving as a claim on future token distribution. At genesis, an airdrop of FXTL points was planned for veFXS stakers, and Frax’s North Star proposal further specifies that a portion of annual FRAX emissions will be dedicated to FXTL conversions, with around 2% of outstanding FXTL points redeemable for FRAX per week. This redeption mechanic both limits the pace at which points can be converted into liquid tokens and provides an ongoing sink for emissions, incentivizing continuous use of Fraxtal over a prolonged period rather than a short-lived speculative spike.

Because FXTL is contract-aware, it becomes possible for Fraxtal to incentivize specific categories of activity, such as sustained liquidity provision, lending, or complex DeFi interactions, rather than simply rewarding raw transaction count. Protocols that deploy on Fraxtal can in principle earn FXTL alongside their users, and then decide how to distribute those points or their eventual tokenized form to their communities. This opens the door to meta-governance and cross-incentive structures: for example, a protocol like Velodrome could integrate FXTL rewards into its own gauge voting, while yield aggregators like Beefy could build vaults that optimize not only for token yield but also for points accrual. In such a scenario, Fraxtal’s blockspace market becomes intertwined with a points market, where protocols compete not only for TVL but also for the right kind of on-chain activity that maximizes FXTL earnings.

Fraxtal’s emphasis on points dovetails with broader DeFi trends, where points programs have become a de facto standard for bootstrapping usage and expectations of future token distributions. Within the Fraxtal ecosystem, Leviathan’s SQUID points and token, used to coordinate a DAO focused on recovery pools and risk management, and points minted for powered launchpads and media auctions, play into this culture of pre-tokenized participation. However, Fraxtal’s own FXTL system has one crucial difference: it is chain-native and protocol-level, defined in governance proposals and docs rather than being idiosyncratic to any single application. That gives it the potential to serve as a unifying metric and reward channel across multiple apps, provided that governance maintains credibility around the promised tokenization timeline and conversion mechanics.

The interplay between FRAX (governance gas), frxUSD and frxETH (monetary and staking base), and FXTL (activity points) creates an intricate incentive lattice on Fraxtal. Users might hold FRAX to pay gas and participate in governance, deploy frxUSD or frxETH into DeFi positions to earn yield, and simultaneously chase FXTL accrual through high-value activity. Protocols might lock veFRAX for boosted emissions and voting rights, while also optimizing their architecture to maximize FXTL earnings for their contracts and communities. For observers, this raises important questions about sustainability and complexity: does such a layered system genuinely align incentives toward productive economic activity, or does it risk amplifying speculative behavior and short-term yield farming? The answer will depend on how Frax governance calibrates emissions over time and how aggressively it uses FXTL to reward long-term, sticky contributions rather than purely transactional churn.

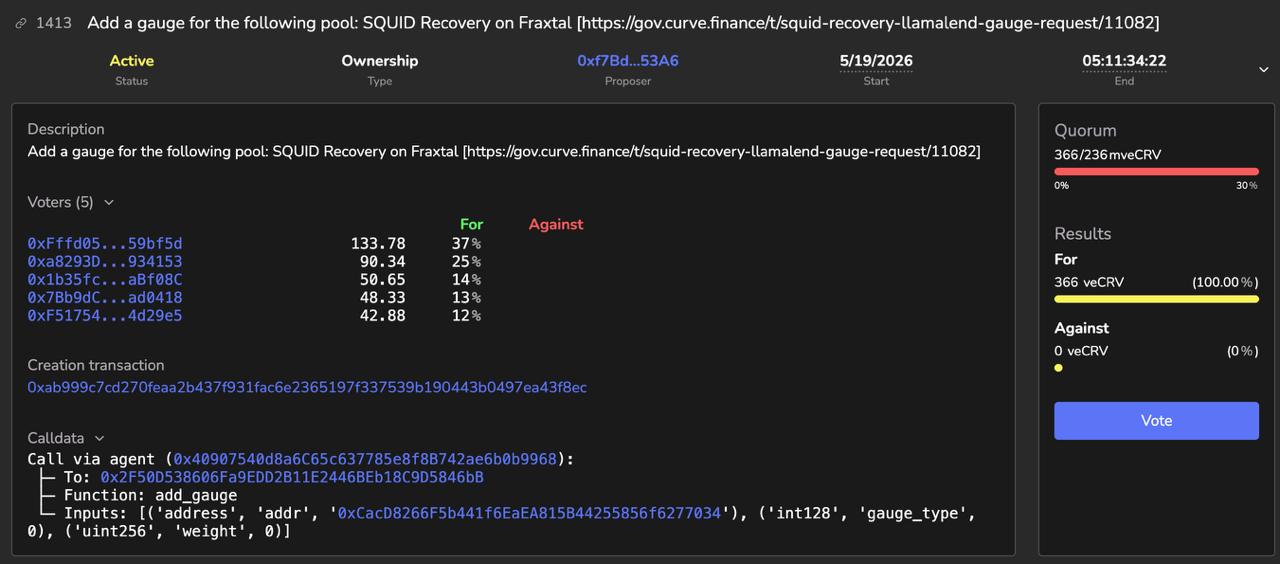

Curve DAO voting opens on the SQUID Recovery pool on Fraxtal

$1.3k in SQUID-rec liquidity is the constraint, not gauge whitelisting: a weight=0 Curve gauge just gets the Fraxtal pool into the emissions machine. If veCRV/vlCVX voters route CRV to a pool holding frxETH, cvcrvUSD, and SQUID, this becomes a live test of whether distressed LlamaLend claims can bootstrap depth without a treasury backstop. If they do not, affected lenders still just have an onchain exit door with no bid behind it.

Governance, DAOs, and the Leviathan Connection

Fraxtal sits at the intersection of several governance frameworks: the Frax DAO, veFRAX/veFXS holders, external DAOs like Curve and Convex, and emerging ecosystem DAOs such as Leviathan’s SQUID DAO. This multi-DAO environment is both a strength, in terms of decentralized decision-making and capital sourcing, and a source of potential complexity for users navigating governance and risk.

Within the Frax protocol, governance is driven by tokenholders who lock their FXS (and in the future FRAX) into veFXS/veFRAX to obtain voting power over proposals and to direct emissions and incentives. The Frax Singularity roadmap, which introduces Fraxtal as the substrate that completes Frax’s core product portfolio, is itself articulated in governance proposals that frame Fraxtal as the “operating system” for the protocol’s various subcomponents. Decisions such as the North Star emissions model, the transition of gas from frxETH to FRAX, and the allocation of significant incentive budgets to partners like Velodrome have all been tabled as Frax Improvement Proposals (FIPs) requiring community approval. This means Fraxtal’s tokenomics, fee structure, and ecosystem incentives are, at least in principle, subject to on-chain governance rather than being fixed by a centralized development team.

Curve DAO plays an important external governance role in Frax’s orbit, particularly in the realm of stablecoin and governance-token liquidity. The Curve DAO controls gauge weights and incentives for pools that often include Frax-related assets, and has considered proposals related to recovery pools and liquidity strategies that touch Fraxtal, including SQUID recovery structures for lenders affected by protocol failures. In parallel, Convex Finance has emerged as a meta-governance layer for Curve and Frax assets, accumulating CVX and FXS exposures and allowing users to stake derivative tokens such as cvxFXS while still participating in governance and earning rewards. Convex’s integration with Frax’s “Road to Singularity” update and with Fraxtal’s FXTL point airdrops demonstrates how governance and incentives can propagate across DAOs, bridging Fraxtal with a wider ecosystem of vote-escrowed and meta-governed protocols.

Leviathan’s SQUID DAO represents a newer kind of governance actor on Fraxtal: a community organized around risk management, recovery, and potentially insurance-like functions. Using SQUID points and token incentives, Leviathan has coordinated recovery pools for lenders impacted by events such as Llama Lend bad debt, often using Fraxtal as the venue for these pools and working with Curve DAO to structure voting and incentive alignment around them. In this context, Fraxtal becomes not only a platform for new DeFi deployments but also a home for post-incident recovery and war-room style coordination, with Leviathan describing itself as a “pillar of Fraxtal” through its SQUID-based DAO. The distribution of Leviathan Points ($SQUID) via airdrops to participants who contribute to building and supporting the ecosystem exemplifies the alignment of social capital, on-chain activity, and point-based incentives that Fraxtal’s design encourages.

Frax governance has also cultivated direct relationships with launch and liquidity platforms such as Fjord Foundry, offering additional benefits and incentives to projects that choose to deploy their tokens and liquidity on Fraxtal via Fjord’s launch platform. Such partnerships shift part of the governance and discovery process off-chain, into curated launch frameworks where Frax-aligned teams can gain early support in the form of FRAX emissions, FXTL point alignment, and community exposure. Combined with sponsored-content auctions and marketing slots accessible via SQUID or wETH on Fraxtal, these structures start to look like a layered governance and media stack in which access to Fraxtal’s users and capital becomes a resource governed by multiple DAOs and coordination games.

This multi-layered governance environment has clear advantages. It allows specialized expertise to emerge; Curve DAO can optimize stablecoin pools, Convex can aggregate governance power, Leviathan can focus on risk and recovery, and Frax DAO can steer the monetary and protocol-level parameters that shape Fraxtal. At the same time, it adds a cognitive load for users and builders, who must understand not only Fraxtal’s own governance but also the interplay of external DAOs whose decisions affect liquidity, incentives, and safety on the chain. For example, a liquidity provider on Fraxtal may be influenced by Frax DAO’s decision to fund Velodrome incentives, Curve DAO’s vote on a recovery pool, Convex’s allocation of boosted emissions, and Leviathan’s SQUID distributions, all at once.

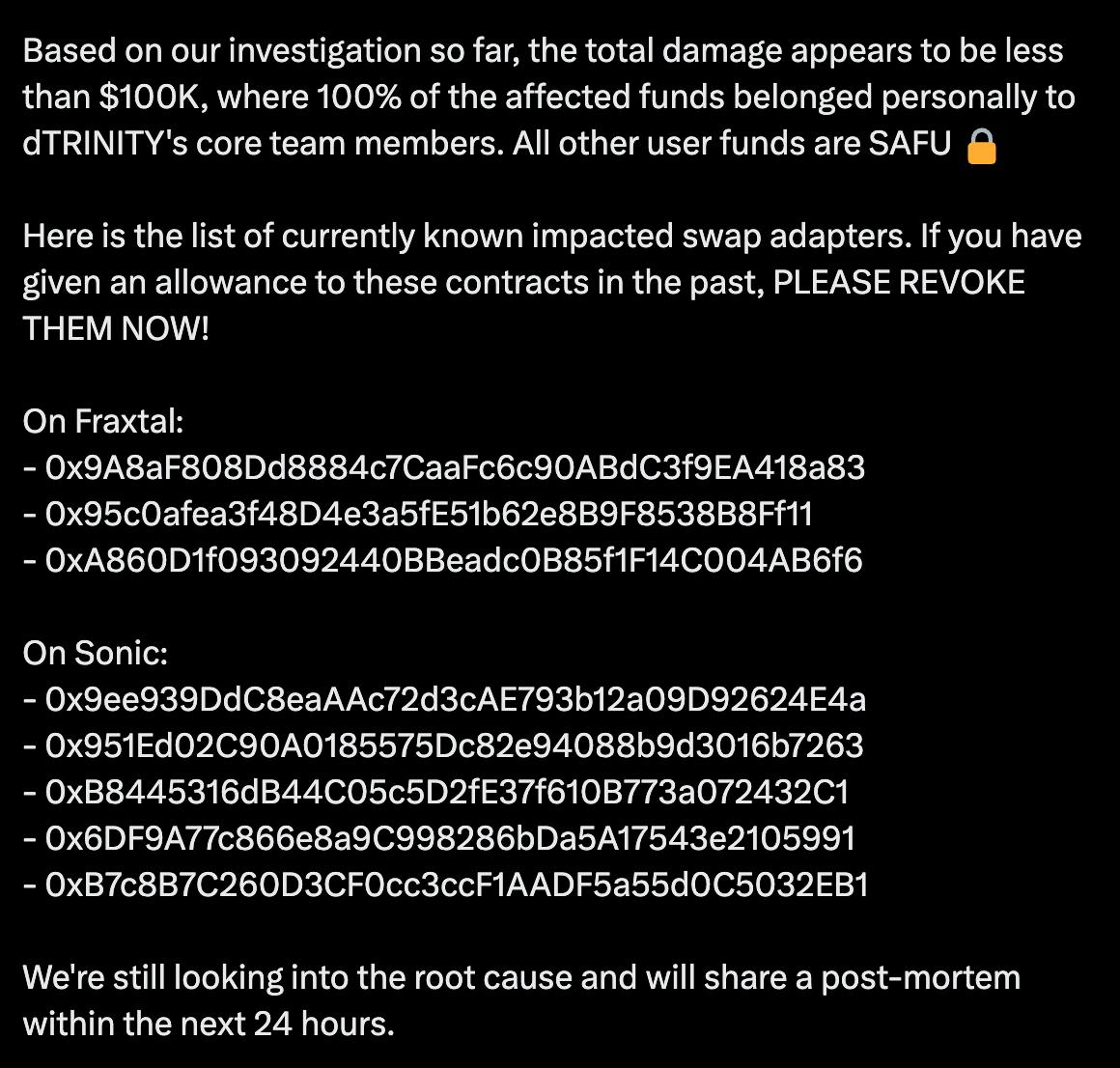

In an evergreen sense, the long-term test for Fraxtal’s governance model will be whether these overlapping DAOs can coordinate effectively in the face of stress, such as smart contract exploits, unforeseen macro events, or contentious tokenomics debates. Early experiences—such as Leviathan’s recovery pool for Llama Lend–related bad debt, Curve DAO’s involvement in recovery pools, and coordinated messaging around security incidents like the exploitation of dTrinity’s swap adapter contracts on Sonic and Fraxtal—provide partial evidence of a governance culture that is willing to engage with risk and recovery publicly rather than ignoring or minimizing them. However, as Fraxtal’s TVL and systemic importance grow, the stakes of such coordination will increase, making robust governance processes and clarity of responsibilities even more crucial.

Brevan Howard stakes 1.1M FXS ($9.8M) ahead of Fraxtal launch

Fraxtal L2 mainnet goes live; airdrop snapshot announced

veFXS governance live on Fraxtal

FLOX blockspace incentive points system activated

Convex adds Fraxtal as third supported sidechain after Arbitrum and Polygon

Frax Singularity roadmap unveiled: L3s, FPIS merge, native Frax minting

North Star Upgrade: FXS rechristened as FRAX, becomes Fraxtal gas token

- 2025-05exploit

dTrinity swap adapter exploit hits Fraxtal and Sonic; users warned to revoke

Developer and User Experience

From the perspective of a developer, Fraxtal aims to be a low-friction extension of the Ethereum development environment, with the added attraction of Frax-centric incentives and user flows. Its full EVM equivalence under the OP Bedrock stack means that Solidity contracts, common tooling, and frameworks such as Hardhat, Foundry, and thirdweb can be used without chain-specific rewrites. For many teams, this makes deploying to Fraxtal a matter of configuration rather than a deep architectural port, which lowers the barrier to experimentation. Thirdweb, for instance, exposes Fraxtal in its dashboard as an OP Stack rollup with frxETH as the gas token, and provides a bridge UI where developers and users can fund their Fraxtal addresses by bridging frxETH or other tokens from supported source chains. This abstraction allows teams to focus on application logic while relying on existing SDKs and deployment pipelines.

For users, onboarding to Fraxtal typically involves a few steps: adding the chain configuration to a wallet, bridging assets such as frxETH, FRAX, or frxUSD from Ethereum or other chains, and then interacting with DeFi protocols on the network. Because Fraxtal is part of the broader OP Stack, many wallets and infrastructure providers can integrate it relatively easily once they support other OP-based chains, and integrations with wallets like Rabby have been publicly highlighted as milestones for SQUID holders and Fraxtal users. As wallet and RPC support matures, the difference between using Fraxtal and interacting with more established L2s such as Base or Optimism shrinks, leaving incentives, liquidity, and application quality as the main differentiators.

Account abstraction and tooling support further shape the user experience. Infrastructure providers like Alchemy have announced support for account abstraction (AA) on OP Stack chains including Zora and Fraxtal, indicating a trajectory toward embedded smart accounts and gas abstraction that could make Fraxtal more accessible to non-technical users. In an AA paradigm, users might interact with Fraxtal through “email-style” logins or app-native wallets, while sponsored gas and batching allow complex DeFi interactions to be executed via a single click. Given Fraxtal’s emphasis on points and on-chain activity, AA could become a double-edged sword: it lowers friction and could increase FXTL accrual, but it also raises questions about who controls user keys, how gas sponsorship is funded, and whether Sybil-resistant identity systems are needed for point distribution.

On the data side, Fraxtal is exploring integrations with modular data and ZK coprocessor systems. Lagrange, a ZK coprocessor framework, has reported an integration with Fraxtal designed to enable cheap and fast cross-chain queries, effectively letting Fraxtal applications pull in and verify big data from other chains with cryptographic guarantees. This opens up design space for sophisticated dApps that need cross-chain portfolio views, risk analytics, or historical data without relying entirely on centralized indexers. For a DeFi-centric chain, having robust, verifiable data infrastructure is critical for building trust-minimized lending markets, risk engines, and AI agents like those on IQ AI’s platform.

Development support is also being formalized through programs like the Fraxtal Hackathon 2024, which emphasizes restaking and advanced DeFi architectures built on the chain. Hackathons and grant programs, funded partly by Frax DAO allocations under the North Star emission plan, serve as pipelines for new teams to join the Fraxtal ecosystem and experiment with novel primitives such as modular lending, restaking-based security, and AI-governed strategies. By combining grant funding, FXTL points, and potential FRAX emissions, Fraxtal can offer a more structured and measurable incentive stack to early-stage teams than a generic chain without a well-defined ecosystem fund.

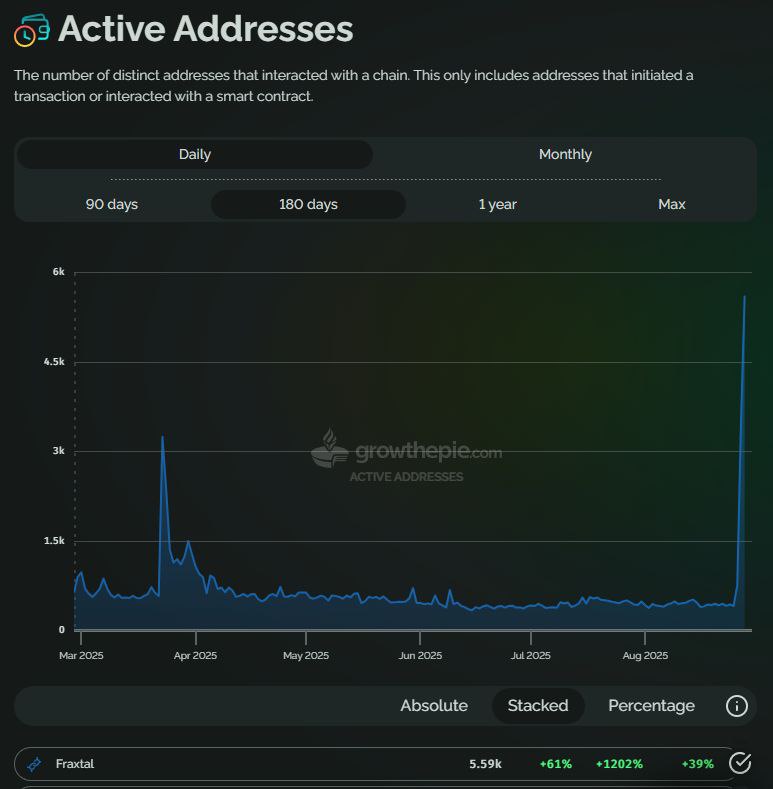

For end users, the growth in daily active addresses and bridge deposits into Fraxtal suggests increasing organic activity, although such metrics can be distorted by points and emissions campaigns. Reports of Fraxtal and chains like Ink leading weekly bridge deposit charts highlight the ability of strong token and points narratives to drive cross-chain capital flows, particularly when combined with concentrated incentives in protocols like Velodrome, Fraxlend, and Boardwalk. Users seeking to evaluate Fraxtal from an evergreen standpoint should therefore look beyond raw TVL or address counts and consider factors such as the diversity of applications, depth of native liquidity, robustness of risk management (including Leviathan-led recovery efforts), and the sustainability of emissions over time.

Security, Risks, and Incident Response

No overview of Fraxtal can be complete without a clear assessment of its security model and the types of risk its users and builders face. At the base layer, Fraxtal shares the optimistic rollup security assumptions of the OP Stack: correctness depends on the integrity of L2 execution, the honesty of at least one party monitoring and challenging invalid state roots, and the secure operation of contracts that govern deposits, withdrawals, and state commitments. The seven-day challenge window used in many OP-based deployments means that final settlement to Ethereum is deliberately delayed, providing time for fraud proofs but also creating UX friction that third-party bridges attempt to mitigate. Users who rely on fast bridges effectively trade some trustlessness for convenience, introducing additional counterparty and liquidity risks.

On top of these generic rollup risks, Fraxtal adds protocol-specific attack surfaces associated with its ecosystem. DeFi protocols deployed on Fraxtal—whether Frax-native or external—can be vulnerable to smart contract bugs, oracle failures, economic exploits, and governance attacks. An example is the exploitation of dTrinity’s swap adapter contracts on Sonic and Fraxtal, where users were advised to revoke approvals to affected contracts while teams investigated and prepared post-mortems. Incidents like this underscore that, even on a relatively new and curated chain like Fraxtal, the composability and complexity of DeFi can introduce non-obvious risk vectors, and that users need to actively manage contract approvals and counterparty exposure.

Fraxlend, by design, introduces protocol risk associated with lending between pairs of ERC-20 assets, which can be magnified on a chain where Frax-native instruments like fxb and staked tokens are widely used as collateral. Liquidity crunches, cascading liquidations, and peg instabilities can interact in ways that are more severe on a specialized chain where many protocols share common collateral types. Similarly, AMMs like Velodrome concentrate risk in their contract code and their governance processes, particularly in gauge and emissions decisions that can shift economic incentives quickly and affect pool health. While these are not unique to Fraxtal, the chain’s tight integration with Frax’s monetary stack means that failures in one protocol can propagate into others via shared assets and governance.

Fraxtal’s governance and economic design create additional risk dimensions. The transition from frxETH to FRAX as gas, the decaying emission schedule, and the conversion mechanics between FXTL and FRAX all involve complex tokenomics that must be implemented correctly and transparently. Bugs or misconfigurations in emission contracts, reward distribution, or FXTL accounting could lead to misallocations, unfair distributions, or even systemic imbalances in incentive structures. Moreover, governance decisions about emissions, treasury deployment, and recovery measures—made by veFRAX holders and Frax DAO delegates—can have large impacts on protocol behavior and user outcomes. Concentrated governance or low voter participation could increase the risk of capture or misaligned decisions, especially if external DAOs with large holdings (such as Convex) play a dominant role.

Incident response is therefore a key part of Fraxtal’s security story. The presence of Leviathan’s SQUID DAO as a dedicated recovery and risk-oriented entity is one example of ecosystem-level response coordination, as seen in its launch of recovery pools for Llama Lend–related bad debt on Fraxtal and Curve DAO’s subsequent involvement in SQUID Recovery pool voting. The Leviathan Points airdrops to supporters who help build and stabilize the ecosystem reflect an approach where reputational and financial incentives are aligned toward collective risk management. Combined with public communication during incidents—such as advising users to revoke approvals to vulnerable contracts and promising detailed post-mortems—these practices help build a culture of transparency and mutual support.

Nonetheless, users should treat Fraxtal as an evolving, experimental environment rather than a risk-free extension of Ethereum. While the chain inherits many of Ethereum’s security guarantees via the OP Stack, it also introduces additional governance, contract, and economic layers that must be evaluated on their own terms. Pragmatically, this means being cautious with position sizing, carefully reviewing protocols’ audits and codebases, monitoring governance decisions that affect collateral and incentives, and staying informed about security advisories from Frax, Leviathan, and other ecosystem teams. Over time, if Fraxtal’s security record remains strong and its incident response processes prove effective, confidence in the chain’s resilience will grow—but this is something that can only be earned through experience, not designed in advance.

An attacker has exploited dTrinity's swap adapter contracts on Sonic and Fraxtal, recommend to revoke access to their adapter contracts while the team prepares a post-mortem

Sad day for sonic and fraxtal chains. My heart to those affected

The dTrinity swap adapter exploit on Fraxtal and the Llama Lend bad debt incident requiring a community recovery pool demonstrate that deployed protocols on Fraxtal have suffered material losses.

Fraxtal is built on the OP Stack and sequencer control is centralized with the Frax team, meaning censorship resistance and upgrade authority depend heavily on a single team's governance decisions.

Ecosystem liquidity depends on sustained FLOX blockspace incentives and protocol-specific deployments; loss of incentive momentum could rapidly drain TVL given the chain's early stage.

FRAX stablecoin underpins the network's economic model, and evolving stablecoin regulation — particularly the GENIUS Act — creates headline risk for the entire Frax ecosystem including Fraxtal.

FLOX incentive value and validator economics are denominated in FXS/FRAX; a sustained FXS price decline compresses incentive rewards and reduces the marginal benefit of deploying to Fraxtal over competing L2s.

veFXS holders vote on-chain for Fraxtal proposals and the Singularity roadmap passed through public governance forums, giving the chain a more structured community input layer than most early-stage L2s.

Fraxtal in the Broader L2 and DeFi Landscape

Fraxtal operates in a crowded and rapidly evolving Layer 2 ecosystem, populated by generalized rollups like Optimism and Base, app-specific chains, and modular rollups built on stacks such as OP, Arbitrum Orbit, and zkSync. Its distinguishing feature is not technical novelty in the rollup design, but deep integration with the Frax protocol and an explicit focus on DeFi and stablecoin economics. In this respect, Fraxtal can be compared to other protocol-centric chains—for example, a lending protocol building its own app chain or a DEX launching an L2 dedicated to order flow—but with a broader monetary scope, given Frax’s role as a stablecoin and staking platform.

Fraxtal’s participation in the OP “Superchain” vision gives it a natural interoperability story with other OP Stack chains. Bridges, shared tooling, and cross-chain messaging frameworks can treat Fraxtal, Base, Optimism, Zora, and other OP chains as part of a common environment, making it easier for users to move assets and for protocols to deploy multi-chain strategies. Fast bridging solutions, such as FastBridge for crvUSD, explicitly target the latency problem of native OP withdrawals by using off-chain messaging and liquidity provisioning to reduce withdrawal times from a week to roughly fifteen minutes, including for transfers from Fraxtal back to Ethereum. This kind of bridging infrastructure makes Fraxtal more usable as a hub for crvUSD and other stablecoins, facilitating arbitrage, liquidation, and cross-chain strategy execution.

Within DeFi, Fraxtal’s specialism may give it a competitive edge in areas where tight coupling with Frax is valuable. For example, protocols that build complex stablecoin-backed structured products, modular credit markets, or restaking-based risk tranching might prefer to deploy on Fraxtal to take advantage of direct access to Frax’s monetary instruments, emissions, and FXTL incentives. The presence of meta-governance players like Convex and infrastructure providers like Lagrange and Beefy further enhances Fraxtal’s attractiveness as a base for advanced strategies, while launch platforms like Boardwalk and Fjord Foundry provide a path for new tokens to access Fraxtal-native liquidity and marketing channels.

At the same time, Fraxtal competes for attention, liquidity, and developer mindshare with more generalized L2s that may offer larger user bases, more diverse ecosystems, or different security trade-offs. For a DeFi project considering where to launch, the decision to prioritize Fraxtal may hinge on how important Frax integrations are to its design, how compelling the FXTL and FRAX emission incentives are relative to grants and rewards on other chains, and how it evaluates Fraxtal’s security and governance maturity. Projects with strong existing user bases on Ethereum mainnet or other L2s may choose to treat Fraxtal as one deployment among many, focusing Fraxtal-specific features on Frax-related collateral and user segments.

Early metrics suggesting that Fraxtal has at times led weekly bridge deposits and posted yearly highs in daily active addresses indicate that the chain has succeeded in capturing at least periodic waves of user interest, often correlated with incentive campaigns, point airdrops, or high-profile launches. The integration of staking V2 infrastructure on aggregators like Stake DAO for Fraxtal and other chains demonstrates that Fraxtal is being woven into multi-chain yield and governance strategies, not just treated as an isolated experiment. However, as with any chain experiencing growth driven by emissions and points, the critical question is how much of that activity will persist once early incentives taper off according to the North Star emission decay.

From an evergreen lens, Fraxtal’s most durable competitive advantage is likely to be its role as the canonical execution environment for the Frax protocol itself. As Frax continues to iterate on its stablecoins, ETH staking, lending, and restaking architectures, Fraxtal can act as the testbed and production venue where these components are integrated most deeply. The Road to Singularity framing underscores this: Fraxtal is the substrate through which Frax seeks to unify its subprotocols into a coherent, self-referential monetary and financial system. If that vision resonates with enough capital, developers, and governance participants, Fraxtal may carve out a distinct niche as a “monetary L2” within the broader L2 and DeFi landscape.

Conclusion

Fraxtal represents a strategic shift in how protocol-native blockspace is conceived and implemented. Rather than building purely on third-party chains, Frax Finance has constructed an OP Stack–based Layer 2 that serves as the operational core for its stablecoins, ETH staking products, lending markets, and DeFi integrations. By tying gas, emissions, and blockspace incentives directly to the Frax governance token (formerly FXS) and by introducing FXTL as a chain-level point system for contract activity, Fraxtal embeds economic policy into the fabric of the chain itself. This design aligns the interests of Frax governance, Fraxtal users, and ecosystem builders in a way that is difficult to replicate on neutral, general-purpose L2s.

At the same time, Fraxtal inherits the benefits and trade-offs of optimistic rollups: lower fees and higher throughput than Ethereum mainnet, but with delayed finality and reliance on off-chain actors to monitor and challenge invalid state roots. It adds additional layers of complexity through its multi-DAO environment, where Frax DAO, Curve DAO, Convex, Leviathan’s SQUID DAO, and others interact to shape liquidity, incentives, and risk management. Security incidents affecting protocols deployed on Fraxtal, such as the dTrinity exploit, illustrate that building on a curated, Frax-centric chain does not eliminate DeFi risk, even if ecosystem actors respond with recovery pools and governance coordination.

From a user and developer perspective, Fraxtal’s value proposition lies in its combination of familiar EVM tooling, specialized DeFi infrastructure, and rich incentive design. Developers can port existing Solidity contracts and leverage tools like thirdweb, Alchemy, and Lagrange, while users benefit from integration with Frax stablecoins, Velodrome liquidity, Fraxlend markets, yield aggregators like Beefy, and experimental platforms like IQ AI. Points systems—FXTL at the chain level and SQUID, Boardwalk, and other points at the application level—further shape behavior and attract attention, though they also introduce speculative dynamics that must be carefully managed to avoid unsustainable boom-and-bust cycles.

Ultimately, Fraxtal should be viewed as an ongoing experiment in protocol-native blockspace and monetary design rather than a finished product. Its success will hinge on how effectively Frax governance can balance emissions with sustainability, how robustly DAOs like Leviathan can manage risk and recovery, and how attractive Fraxtal remains to builders once early incentives normalize. For crypto news readers and DeFi participants, Fraxtal is worth watching not only as a new L2, but as a case study in how a mature protocol attempts to consolidate its ecosystem and express monetary policy directly in blockspace.

Outlook

Looking ahead, Fraxtal’s trajectory will likely be shaped by three forces: the maturation of the North Star tokenomics and FXTL conversion mechanics, the depth and resilience of its DeFi ecosystem, and its integration into the broader OP Superchain and multi-chain DeFi environment. As FRAX emissions decay and FXTL tokenization progresses, the chain will need to pivot from incentive-driven growth to more organic, utility-driven adoption, relying on the strength of its Frax-native products and the quality of third-party protocols like Velodrome, Fraxlend markets, IQ AI, and future entrants.

If Fraxtal can maintain security, coordinate effective responses to inevitable incidents, and continue to attract builders through hackathons, grants, and a clear value proposition, it has the potential to solidify its role as the primary “home chain” for the Frax monetary system and a significant DeFi hub in its own right. Conversely, if governance fragmentation, overly complex incentives, or security lapses undermine confidence, Fraxtal may struggle to retain users and liquidity in the face of competition from more generalized and deeply liquid L2s. For now, Fraxtal stands as one of the most ambitious attempts to marry protocol-native blockspace with stablecoin and staking economics—a development that will inform how other major DeFi protocols think about their own chain strategies in the years ahead.

Latest Fraxtal news

Leviathan SQUID DAO launches recovery pool for lenders affected by Llama Lend bad debt on FraxtalCurve DAO voting opens on the SQUID Recovery pool on Fraxtal An attacker has exploited dTrinity's swap adapter contracts on Sonic and Fraxtal, recommend to revoke access to their adapter contracts while the team prepares a post-mortem From CRCL to FRAX: The Next GENIUS Act Play

From CRCL to FRAX: The Next GENIUS Act Play Fraxtal just put in a yearly high for Daily Active Addresses

Fraxtal just put in a yearly high for Daily Active Addresses Staking V2 now live on @CurveFinance: Fraxtal, @base, and @SonicLabs Experience Stake DAO's upgraded infrastructure: + Instant boosted reward distribution + No reward dilution + Re...

Staking V2 now live on @CurveFinance: Fraxtal, @base, and @SonicLabs Experience Stake DAO's upgraded infrastructure: + Instant boosted reward distribution + No reward dilution + Re...Sources

- https://frax.com

- https://thirdweb.com/fraxtal

- https://www.youtube.com/watch?v=W0oK5FEDqMc

- https://gov.frax.finance/t/frax-north-star-proposal-v1-0/3628

- https://docs.frax.finance/fxs-and-vefxs/vefxs

- https://docs.optimism.io/op-stack/protocol/overview

- https://docs.frax.com/fraxtal/fraxtal-incentives/fraxtal-point-system

- https://steamcommunity.com/app/1962700/discussions/0/834999271307648198/?l=polish

- https://docs.frax.com/protocol/subprotocols/fraxlend/overview

- https://gov.frax.finance/t/fip-362-velodrome-on-fraxtal-proposal-for-incentives-for-liquidity-growth/3083

- https://gov.frax.finance/t/fip-341-frax-singularity-roadmap-part-1/2987

- https://docs.frax.com/protocol

- https://www.curve.finance/dao

- https://dorahacks.io/hackathon/fraxtal/buidl

- https://fraxcesco.substack.com/p/everything-you-need-to-know-on-frax

- https://beefy.com

- https://x.com/fraxfinance/status/2061488214645338302

- https://iqai.com

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…