Deep dive into Hyperliquid’s HIP‑3 framework for builder‑deployed perpetuals, covering mechanics, RWA and pre‑IPO markets, AI‑driven trading, risks, and how HIP‑3 is reshaping on‑chain perps and CEX–DEX dynamics.

+5 sources across the wider coverage universe

Hyperliquid HIP-3 surpasses $2B in open interest as tokenized equities displace metals2026-04

Hyperliquid HIP-3 surpasses $2B in open interest as tokenized equities displace metals2026-04 TradeXYZ buys $SPCX HIP-3 ticker for 500 HYPE ahead of likely SpaceX pre-IPO perp2026-05

TradeXYZ buys $SPCX HIP-3 ticker for 500 HYPE ahead of likely SpaceX pre-IPO perp2026-05 Hyperliquid RWA open interest surpasses $2.3B as HIP-3 commodity perps hit new all-time high2026-04

Hyperliquid RWA open interest surpasses $2.3B as HIP-3 commodity perps hit new all-time high2026-04 Hyperliquid HIP-3 prints record $5.4B daily volume with $1.3B in silver and $1.2B in crude oil perps2026-03

Hyperliquid HIP-3 prints record $5.4B daily volume with $1.3B in silver and $1.2B in crude oil perps2026-03

On Hyperliquid, HIP-3 is the “builder-deployed perpetuals” framework that lets third‑party teams permissionlessly list and operate perpetual futures markets, including real‑world assets and pre‑IPO stocks, directly on-chain. By handing control of listings, oracles, and fee structures to external builders, HIP‑3 has become a core engine behind Hyperliquid’s rise as a 24/7, multi‑asset perp venue that now competes with major centralized exchanges on volume and market share.

What Is HIP‑3?

HIP‑3 is a Hyperliquid Improvement Proposal that formalized a new class of markets on the Hyperliquid Layer 1: “builder‑deployed” perpetual futures, often shortened to HIP‑3 markets. In contrast to Hyperliquid’s original “native” perps, where the protocol team controlled listings and price feeds, HIP‑3 opens the door for independent teams to deploy their own perpetual futures for almost any asset with a reliable price oracle. Builders stake HYPE, Hyperliquid’s native token, to gain deployer rights and are then responsible for configuring the market’s parameters, securing its oracle infrastructure, and maintaining its uptime. This shift from centrally curated listings to permissionless market creation is a key step toward decentralizing the exchange’s product surface while preserving a unified liquidity and risk engine.

The economic and governance design of HIP‑3 is meant to balance openness with skin in the game. To launch markets, a builder must stake a significant amount of HYPE—commonly cited as 500,000 HYPE—which both throttles spam and creates a bond that can be slashed or politically penalized if markets are mismanaged. In turn, deployers receive a share of the fees that their markets generate, aligning their incentives with the long‑term health and volume of those markets. Hyperliquid’s core chain handles matching, risk, liquidations, and cross‑margining across all markets, while HIP‑3 pushes the responsibility for price discovery and data infrastructure to the perimeter. This division of labor lets the base protocol remain lean and neutral, while specialized builders experiment with new assets, oracle designs, and fee models at the edge.

From a user’s point of view, a HIP‑3 market looks and feels like any other Hyperliquid perp. Traders still see order books, funding rates, cross‑collateralization and the familiar interface, whether they are trading BTC, crude oil, or a pre‑IPO stock index. Under the hood, however, the listing, pricing, and fee revenue for that market may be controlled by an independent builder rather than the core Hyperliquid team. This structure blurs the line between a single exchange and a marketplace of exchanges built atop a shared settlement layer, and it helps explain why HIP‑3 has emerged as a magnet for real‑world asset (RWA) perps, tokenized equities, and more exotic markets.

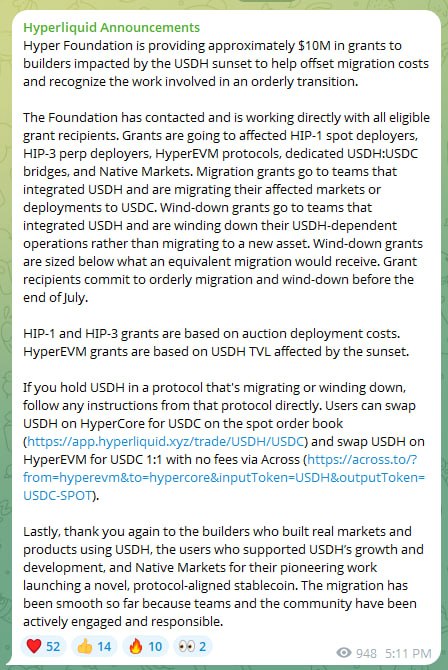

Hyper Foundation offers $10M in USDH sunset grants to HIP-1, HIP-3, and HyperEVM builders

Promoting from Tsunami auto-feed. Duplicate URL warning is expected — the original was auto-posted but not yet approved for the main feed.

Readers click HIP-3 for the assets, not the architecture — the spike on commodity and pre-IPO equity milestones reveals that the real draw is 24/7 onchain access to markets traditionally gated by TradFi hours and broker relationships, with volume records serving as proof that retail demand for those assets is real.↗

How HIP‑3 Works Under the Hood

Builder‑Deployed Markets and HYPE Staking

The starting point for understanding HIP‑3 is the builder role. To deploy a HIP‑3 market, a team must first stake a fixed quota of HYPE—identified in early documentation and reporting as 500,000 HYPE. This stake functions as a security bond and a gatekeeping mechanism. It is large enough that casual or malicious deployers face a substantial economic hurdle, but attainable enough that specialist RWA teams, trading firms, and DeFi projects can still participate. Some reports also note that stakers receive a share of transaction fees on their markets—often quoted as fifty percent of trading fees—with the remainder accruing to protocol stakeholders and the Hyperliquid ecosystem.

Once a builder has staked HYPE and been recognized as a deployer, they can configure the parameters of each perpetual contract they wish to launch. This includes basic settings such as the base asset, quote asset (typically a stablecoin), minimum tick size, leverage caps, and other trading rules. Crucially, deployers can also set a custom open interest cap per asset, limiting the maximum notional exposure that traders can take long or short in that market. By tuning these caps, builders can scale markets carefully as their oracle, liquidity, and risk infrastructure mature, and avoid taking on systemically dangerous exposures too early.

Deployers are also responsible for defining the market’s fee structure within the bounds allowed by the protocol. Maker and taker fees, as well as any rebate or incentive programs, can be adjusted to attract certain kinds of flow or to mimic the pricing of centralized exchanges. Because deployers share in the revenue a market generates, they have a direct interest in optimizing fees for both competitiveness and sustainability. Over time, this creates a competitive landscape where builders vie to launch the most compelling and liquid markets, while traders gravitate toward those with the best combination of spreads, depth, and fee schedules.

Oracles and Pricing: The Core Responsibility

The single most important responsibility HIP‑3 pushes to builders is oracle design. In Hyperliquid’s native HyperCore markets, the protocol team runs and curates the price infrastructure that feeds into the risk engine and liquidation system. With HIP‑3, the deployer must supply and maintain their own oracle stack, ensuring accurate, timely, and manipulation‑resistant prices for the underlying asset. This is straightforward for large crypto assets with deep on‑chain liquidity but becomes significantly more complex when the underlying is a U.S. stock, a commodity that trades on limited hours, or a pre‑IPO equity with fragmented secondary markets.

The RedStone “HyperStone” stack is an illustrative example of the sophistication emerging around HIP‑3 oracles. To power some of the earliest HIP‑3 markets, the Felix team and RedStone built a three‑tier oracle system optimized specifically for Hyperliquid’s latency and architecture. At its core is a 4‑of‑6 multisig verification quorum, chosen explicitly as a counter‑example to the weaker 1‑of‑1 and 2‑of‑5 multisig configurations that had contributed to more than \(\$600\) million in DeFi losses from oracle failures, compromised keys, and single points of failure in early 2026. The HyperStone design incorporates dual‑state pricing to handle the fact that many equities and commodities do not trade 24/7, offering robust handling of weekends and market closures while keeping perps open around the clock.

This emphasis on oracle robustness is not optional. Because HIP‑3 markets share a risk engine and collateral pool with the rest of Hyperliquid, a mispriced or stale market can trigger cascading liquidations, bad debt, and loss of confidence across the entire exchange. Deployers who cut corners on oracle infrastructure may see their markets shunned by sophisticated traders or, in extreme cases, face social or governance pressure from the Hyperliquid community. Conversely, teams that invest in resilient, geographically distributed data pipelines and multi‑party signing setups can turn HIP‑3 markets into credible substitutes for major centralized venues, particularly in RWA segments where on‑chain competition is still thin.

Risk Controls, Funding, and Liquidations

Beyond oracles, HIP‑3 markets plug into the same margining, funding, and liquidation machinery that powers Hyperliquid’s native perps. Traders typically post collateral in stablecoins or other accepted assets and can take leveraged long or short positions without ever owning or handling the underlying asset itself. The protocol continuously marks these positions to the oracle price and enforces maintenance margin requirements; if a position’s equity falls below a threshold, it is liquidated automatically. This logic abstracts away the complexity of delivery, custody, and settlement that characterizes traditional futures markets, making HIP‑3 perps accessible to any user with a supported wallet.

Funding rates play a central role in keeping HIP‑3 perp prices in line with their underlying spot or reference prices. When the perp trades above the reference, longs pay shorts via periodic funding payments; when it trades below, the reverse occurs. For RWA markets that reference centralized venues with fixed trading hours, such as U.S. equities or commodities futures, builders must ensure their oracles and funding mechanisms behave sensibly during off‑hours and around major macro events. Systems like HyperStone’s dual‑state oracle logic are one approach to bridging this gap, but design choices vary across deployers.

Open interest caps are another crucial risk control. Since HIP‑3 deployers can set per‑asset caps, they effectively choose how much systemic exposure their market can contribute to the broader platform. Low caps are common for newly launched or experimental markets, while large‑cap RWAs with deep TradFi markets can support higher caps as confidence and liquidity grow. When combined with portfolio margining, cross‑collateralization, and the ability to hedge across related HIP‑3 and native markets, these controls allow Hyperliquid to scale from crypto‑only perps toward a more generalized, multi‑asset derivatives platform.

Fees, Revenue Sharing, and Incentives

The fee and incentive structure around HIP‑3 is designed to create a marketplace of specialist exchanges atop Hyperliquid’s shared L1. According to early coverage and documentation, deployers who stake HYPE to launch markets earn a substantial share of the trading fees generated by those markets—commonly cited as fifty percent—while the remainder flows back to the protocol, HYPE stakers, and ecosystem participants. This revenue share creates a powerful incentive for trading firms, RWA specialists, and DeFi projects to assume the operational burden of running high‑quality markets. In effect, HIP‑3 lets Hyperliquid outsource product expansion while keeping liquidity and risk centralized.

As HIP‑3 volumes have grown, so too has their contribution to Hyperliquid’s overall fee and revenue profile. Analytics dashboards and third‑party data providers track “Perps” fees on Hyperliquid as including both native and HIP‑3 markets, alongside the builders’ fee share. This creates a dual stake in HIP‑3’s success: deployers profit from the performance of their individual markets, while HYPE holders and protocol stakeholders benefit from aggregate growth across the entire perps complex. The combination of fee sharing, HYPE staking, and protocol‑level rewards has made HIP‑3 an attractive venue not only for traders but also for a growing class of on‑chain “market operators” whose business is effectively to run their own sub‑exchange atop Hyperliquid.

HIP‑3 in the Context of Hyperliquid

From Crypto‑Native Perps to a Multi‑Asset Exchange

Hyperliquid itself is a Layer 1 blockchain purpose‑built for trading, best known for its decentralized perpetual futures exchange and supporting spot market. Running its own chain allows Hyperliquid to tailor block times, fee structures, and system design around high‑throughput order book trading. Over time, the ecosystem has expanded to include borrowing and lending, real‑world assets, and a full EVM environment, but perps remain its flagship product. Before HIP‑3, those perps were largely crypto‑native: BTC, ETH, and a growing roster of altcoins, all with prices primarily derived from on‑chain activity and large centralized crypto exchanges.

HIP‑3 marked a decisive pivot toward becoming a multi‑asset derivatives venue. Because the framework allows deployers to bring their own oracles and list virtually any asset with a trustworthy price feed, the catalog of HIP‑3 markets quickly expanded beyond crypto into real‑world assets. Builders launched perps on commodities like gold and crude oil, foreign exchange pairs such as EUR/USD, major equity indices like the S&P 500 and Nikkei 225, and single stocks including marquee names like NVIDIA and Tesla. In these markets, traders gain leveraged, long‑or‑short exposure to the price movements of traditional assets while all settlement and margining remain entirely on-chain, typically in stablecoins.

The result is that Hyperliquid increasingly resembles an always‑on alternative to traditional derivatives exchanges such as the CME, but with a much lower barrier to entry and a far broader asset menu for small traders. DeFi‑native wallets can access the same macro exposures that previously required brokerage accounts, futures permissions, and complex KYC processes. At the same time, HIP‑3 markets maintain the UX and composability of DeFi: positions can be used as collateral in other protocols, integrated into automated strategies, or accessed through aggregators and wallets that abstract away the protocol details.

Volume, Open Interest, and Market Share

The impact of HIP‑3 on Hyperliquid’s growth is visible in both volume and open interest (OI) metrics. Shortly after launch, HIP‑3 markets reached daily volumes of more than \(\$500\) million, with a majority of activity concentrated in synthetic perps tied to equities and equity indices. As builders iterated and more RWA markets came online, HIP‑3 open interest climbed sharply, with one early milestone marking a peak of \(\$1.84\) billion and a 200% month‑on‑month increase. HIP‑3 daily trading volumes subsequently crossed the \(\$1\) billion threshold on consecutive days in January 2026, signaling that these markets were no longer experimental sidelines but core liquidity venues on the platform.

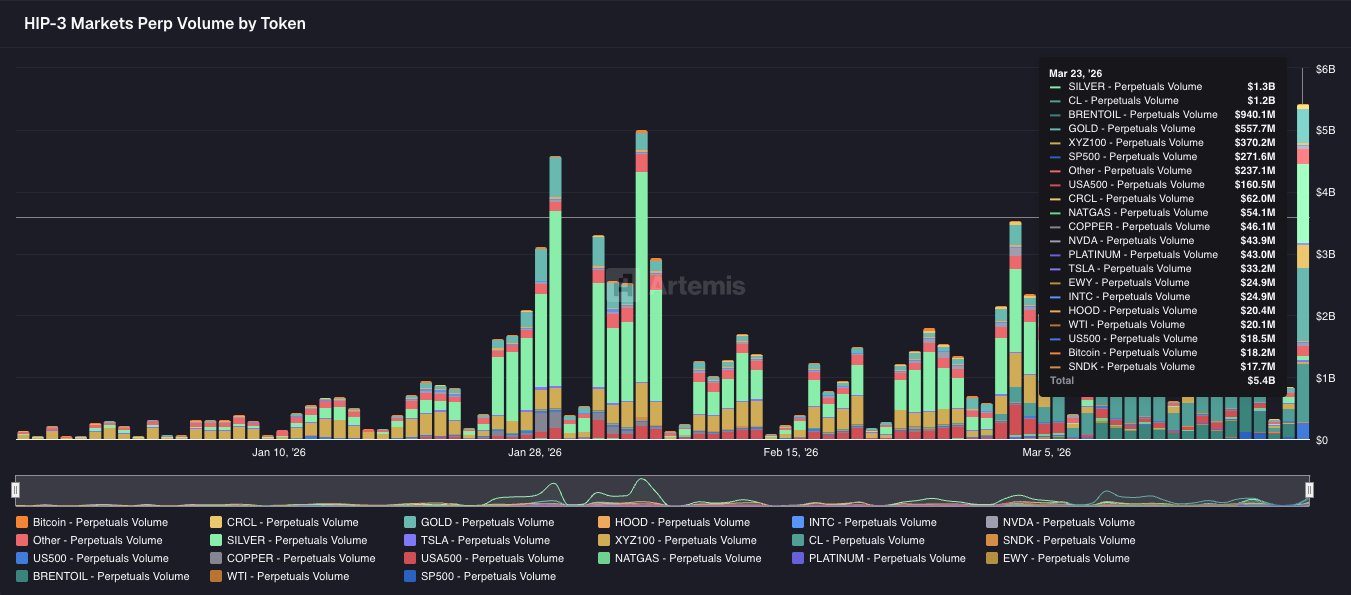

By March 2025, commodity‑heavy HIP‑3 flows pushed the framework to a then‑record daily trading volume of \(\$5.4\) billion, according to Artemis data cited in exchange reporting. Silver and crude oil perps alone accounted for around \(\$1.3\) billion and \(\$1.2\) billion of that day’s volume, underscoring trader demand for leveraged commodity exposure in an on‑chain venue. In the months that followed, analytics from industry outlets like The Defiant and data from Artemis showed HIP‑3 clearing roughly \(\$62\) billion in monthly volume, driving Hyperliquid to a record share of the global perpetuals market.

That market share is not limited to DeFi. In May, aggregated metrics showed Hyperliquid’s perps volume—heavily driven by HIP‑3—reaching approximately 6.63% of global centralized exchange perpetual futures volume, and around 14.4% relative to Binance alone, another all‑time high. For real‑world asset perps specifically, CoinGecko’s RWA report found that HIP‑3’s share of monthly RWA perp volume rose from 2.8% at launch in October 2025 to 28.6% by March 2026, reflecting its emergence as a leading on‑chain venue for tokenized equity and commodity exposure. By early June 2026, the open interest in RWA markets on Hyperliquid reached a new all‑time high around \(\$3\) billion, with the protocol noting that HIP‑3 had set a fresh OI record every month since launch.

These figures sit alongside a rapid expansion in the platform’s user base. Hyperliquid’s active perpetual traders climbed to roughly 231,000 at one point, up from about 127,000 less than a year earlier, with coverage attributing much of that growth to HIP‑3’s permissionless RWA markets. When combined with newsroom reporting that HIP‑3 markets have surpassed \(\$2\) billion in open interest at times and processed over \(\$130\) billion in cumulative volume across more than 100 markets, the picture that emerges is of a framework that has transitioned from experimental add‑on to central growth pillar.

To make this shift concrete, it is useful to contrast a traditional venue like CME’s WTI crude oil futures, long billed as the world’s most liquid oil contract, with a HIP‑3 crude oil perp. Both offer leveraged exposure to oil prices; both attract sophisticated traders and hedgers. Yet only the HIP‑3 market operates fully on-chain, settles in stablecoins, and is accessible to anyone with a DeFi wallet, twenty‑four hours a day, including weekends, via a DEX interface. That combination—open access, multi‑asset coverage, and growing depth—underpins HIP‑3’s role in Hyperliquid’s evolving identity as an on‑chain competitor to both crypto CEXs and TradFi derivatives exchanges.

HIP‑3 Versus Centralized Exchanges

From a structural perspective, HIP‑3 sits somewhere between a centralized exchange and a traditional on‑chain DEX. Like CEXs, HIP‑3 markets can mirror a wide range of assets, from BTC and ETH to U.S. equities and commodities, with order book trading and high leverage. Like DEXs, traders retain self‑custody of funds, transactions settle on-chain, and listings are no longer controlled by a single corporate entity. The permissionless nature of HIP‑3 listings stands in sharp contrast to the curated product menus of major CEXs, where new perps and RWA offerings are limited by regulatory regimes, licensing, and internal risk committees.

In practice, HIP‑3 and CEXs are increasingly interdependent. Many HIP‑3 RWA perps take their reference prices from centralized markets—equity exchanges, commodity futures venues, or large crypto exchanges—via sophisticated oracle stacks. At the same time, HIP‑3 has begun to influence price discovery itself, particularly in pre‑IPO and off‑hours trading, where on‑chain markets may be the only venue trading a given asset around the clock. This feedback loop is most obvious in high‑profile cases like SpaceX’s SPCX perp, where on‑chain pricing and volume have become inputs into broader market sentiment ahead of a public listing.

- 01Commodity perps volume records↗

Silver and crude oil perpetuals printing a $5.4B daily volume record — dwarfing prior benchmarks — made HIP-3 legible to readers as a genuine macro trading venue, not a crypto novelty.

- 02SpaceX pre-IPO perp SPCX↗

The prospect of trading a SpaceX perp before the company IPOs crystallised HIP-3's unique value proposition — onchain price discovery for assets TradFi explicitly locks away from retail.

- 03RWA open interest milestones↗

Sequential OI all-time highs ($2B → $2.3B → $3B) gave readers a compounding growth narrative that framed HIP-3 as the dominant venue for tokenized real-world assets.

- 04Tokenized equities displacing metals↗

The compositional shift — equities overtaking silver and gold in open interest — signalled a maturation of the product mix and attracted readers tracking which asset class captures the next wave of capital.

- 05Leverage risk and storm warnings↗

The Bitget Wallet piece foregrounded the systemic danger of high leverage on 24/7 markets with no circuit breakers, drawing readers who wanted a risk-adjusted view of the opportunity.

- 06HIP-3 share of global perps market↗

HIP-3 accounting for 90%+ of perp DEX volume and Hyperliquid reaching a record share of global CEX perps gave readers a competitive-positioning angle on the protocol's growth trajectory.

Real‑World Asset Perps and Pre‑IPO Trading

What Are RWA Perpetuals?

Real‑world asset perpetuals are derivative contracts that track the price of traditional financial instruments—such as commodities, foreign exchange pairs, equity indices, or single stocks—while settling entirely on-chain in crypto collateral, usually stablecoins. Unlike tokenized securities, which represent actual ownership or claims on underlying assets, RWA perps are purely synthetic. Traders are simply speculating on, or hedging against, the direction of the underlying price; they never take delivery of oil barrels, treasury bonds, or corporate shares. Profit and loss are paid out in the collateral asset, and positions can be opened and closed at any time, subject to market liquidity and protocol rules.

This model has several advantages. First, it allows for extremely fast listing of new markets, since the protocol does not need to arrange custody, settlement, or legal treatment for the underlying assets. Second, it eliminates many operational headaches associated with cross‑border securities trading, as users interact only with on‑chain contracts and collateral. Third, it enables both long and short positions with leverage, allowing traders to implement hedging, arbitrage, and directional strategies that would otherwise require margin accounts and complex brokerage setups. From a regulatory standpoint, however, RWA perps inhabit a gray area because they mirror regulated instruments without directly touching them, a tension that is likely to intensify as volumes grow.

HIP‑3 has become one of the primary frameworks through which RWA perps have moved on-chain. Builders use the standard to deploy markets that reference everything from major commodities to niche equity indices, relying on carefully curated price feeds from centralized venues. Some specialized RWA perp DEXs, such as Ostium, have appeared alongside Hyperliquid, but reporting frequently describes Hyperliquid, via HIP‑3, as the dominant on‑chain perp venue and the base layer for much of the tokenized‑equity and pre‑IPO activity. The combination of a robust L1, a flexible listing framework, and a growing ecosystem of oracle providers has helped HIP‑3 carve out a central role in this emerging category.

HIP‑3 as a Base Layer for Tokenized Equities and RWAs

The scale of HIP‑3’s RWA footprint is increasingly visible in analytics and market commentary. CoinGecko’s 2026 RWA report notes that HIP‑3’s share of monthly RWA perp volume rose from 2.8% at launch in October 2025 to 28.6% by March 2026, marking it as one of the fastest‑growing venues in the sector. Hyperliquid’s own communications and third‑party coverage have highlighted that HIP‑3 RWA open interest has set fresh all‑time highs month after month, surpassing \(\$2\) billion, then \(\$2.3\) billion, and eventually \(\$3\) billion in notional exposure as commodity perps and tokenized equities draw in more traders.

Within that RWA universe, tokenized equities and equity indices play a particularly prominent role. Early HIP‑3 market activity clustered around synthetic perps tied to U.S. stock indices and individual large‑cap names, allowing traders to express views on companies and sectors without leaving the on‑chain environment. Over time, this expanded into more specialized themes, such as pre‑IPO baskets and frontier tech segments. Meanwhile, commodity perps on silver, crude oil, and other raw materials have posted some of HIP‑3’s biggest single‑day volumes, reflecting both macro hedging demand and speculative interest in global events.

At a structural level, HIP‑3 effectively turns Hyperliquid into a base layer for RWA experimentation. Builders can deploy perps on traditional assets without building their own chain, matching engine, or settlement technology. Instead, they tap into Hyperliquid’s existing user base, liquidity, and composability, while differentiating themselves through novel asset lists, branding, and risk management approaches. For traders, the result is a unified interface where crypto perps, tokenized equities, and commodity markets coexist, all collateralized in the same margin system. For the broader DeFi ecosystem, HIP‑3 markets act as building blocks for structured products, indices, and yield strategies that span both on‑chain tokens and off‑chain economic exposures.

Case Study: SPCX and Pre‑IPO SpaceX Trading

Perhaps the clearest illustration of HIP‑3’s role in price discovery is the SPCX perp, a market that tracks SpaceX’s valuation in the run‑up to, and aftermath of, its widely anticipated IPO. Even before listing, Hyperliquid’s HIP‑3 framework emerged as a venue for pre‑IPO trading and price discovery for SPCX, giving traders a way to express views on SpaceX’s value long before most traditional investors had access. A dedicated ticker, SPCX, was acquired via HIP‑3 by an on‑chain trading group ahead of the likely listing, signaling market expectations that SpaceX’s eventual public debut would be one of the defining events of the cycle.

When the IPO finally arrived, SPCX became HIP‑3’s largest market by volume. Newsroom reporting notes that on IPO day alone, trading volume in the SPCX perp on Hyperliquid hit roughly \(\$1.4\) billion, with total cumulative volume of around \(\$3.1\) billion across the nine‑day window spanning pre‑ and post‑IPO trading. In effect, HIP‑3 turned an illiquid, private‑market asset into a highly liquid, 24/7 tradable contract that both anticipated and then mirrored the company’s public market performance. Because on‑chain perps never close, the SPCX market had “no closing bell,” continuing to trade through after‑hours and weekend periods when traditional exchanges were shut, potentially influencing sentiment about SpaceX’s fair value even when cash equities could not respond.

The SPCX case underscores both the promise and controversy of HIP‑3‑style markets. On the one hand, they democratize access to pre‑IPO exposure and make price discovery more continuous and transparent. On the other, they operate outside the usual securities issuance and disclosure frameworks, raising questions about information asymmetry, regulatory oversight, and the legal status of synthetic exposure to private companies. How regulators ultimately treat such markets—whether as swaps, security‑based derivatives, or entirely new categories—will shape the future of HIP‑3 and similar frameworks across DeFi.

Beyond Finance: Niche and Thematic Markets

Although RWA and crypto perps dominate current volume, HIP‑3 is also being positioned as an infrastructure layer for more unconventional markets. One example comes from the gaming and collectibles world, where projects like Based Launchpool are incubating trading card game (TCG) ecosystems on Hyperliquid with a long‑term path toward TCG perps via HIP‑3 and associated cloud infrastructure. In this model, real card inventories and platform revenues could feed into perpetual markets that track the value of specific card collections, sets, or even entire game franchises, blurring the line between financial derivatives and fandom‑driven assets.

By allowing any sufficiently resourced builder to deploy and maintain markets, HIP‑3 creates room for a long tail of thematic derivatives—ranging from eSports performance indices to creator‑economy baskets and beyond. While many of these experiments may remain niche, they illustrate the breadth of what “markets” can mean in an on‑chain context. The same infrastructure that powers SPCX and crude oil perps can, in principle, be used to synthesize exposure to entirely new digital‑native phenomena. As with RWAs, the constraint is less technical than it is about data quality, oracle robustness, and the alignment of economic incentives between traders, builders, and the underlying communities.

HIP‑3, AI Agents, and Autonomous Trading

Virtuals EconomyOS and LLM‑Native Strategies

A second major trend intersecting with HIP‑3 is the rise of AI‑driven, fully autonomous trading agents. Virtuals, an agent‑focused ecosystem, has been integrating tightly with Hyperliquid and HIP‑3 through its EconomyOS, effectively enabling any large language model—such as ChatGPT, Claude, or other LLMs—to trade Virtuals agents, Hyperliquid perps, and HIP‑3 markets programmatically. In this setup, a user can connect an AI assistant to EconomyOS, define high‑level goals or constraints, and let the agent execute strategies across multiple markets, from BTC perps to pre‑IPO SPCX contracts and RWA indices.

To secure this agentic activity, the Virtuals community has proposed and co‑authored new Ethereum standards like ERC‑8126, an AI agent verification standard that allows agents to prove security audits, wallet control, and identity without exposing private data. Complementary efforts such as ERC‑8183, an open standard for agent commerce, and the Agent Payments Protocol (APP) aim to provide a structured framework for how agents hold funds, sign transactions, and interact with DeFi protocols. Within this architecture, HIP‑3 markets serve as a rich action space: dozens or hundreds of liquid perp pairs that agents can long, short, hedge, or arbitrage around the clock.

The combination of HIP‑3’s 24/7, multi‑asset markets with AI agents capable of continuous monitoring and execution amplifies both the benefits and risks of on‑chain perps. For sophisticated teams, it unlocks the ability to run market‑making, statistical arbitrage, and cross‑asset hedging strategies that were previously the domain of proprietary trading firms and hedge funds. For retail users leveraging “set and forget” agent configurations, it raises the specter of opaque strategies, hidden leverage, and unexpected liquidation cascades. As AI‑native trading grows, transparency around strategy parameters, risk limits, and agent verification will become increasingly important for user protection.

Wallet Integrations and “Always‑On Macro”

Parallel to AI agents, wallet integrations are making HIP‑3 markets accessible to a far broader audience. Bitget Wallet, for example, has integrated Hyperliquid HIP‑3 to offer users 24/7 “macro markets” directly from a non‑custodial interface, letting them trade tokenized commodities, indices, and equities without leaving the wallet environment. For many retail traders, this is their first exposure to RWA perps on a DEX: they see familiar tickers like gold, S&P 500, or crude oil, but all trades, margining, and settlements happen on-chain through HIP‑3.

Such integrations compress the UX gap between CEXs and DEXs. From the user’s perspective, trading a HIP‑3 crude oil perp via Bitget Wallet may feel little different from trading a futures contract on a centralized app, but the underlying structure is radically different: there is no centralized custodian, no omnibus account, and no single matching engine that can be halted by a corporate decision. Instead, the wallet orchestrates interactions with a permissionless, globally accessible DEX whose markets have been deployed by a decentralized set of builders. At the same time, the ease of one‑tap access to high‑leverage RWA markets introduces new risks, particularly when users may not fully understand funding, liquidation, or the nuances of synthetic exposure.

In this sense, HIP‑3 sits at the confluence of three powerful currents: the tokenization of real‑world financial exposures, the agentization of trading via AI and automation, and the progressive abstraction of DeFi complexity behind wallet‑level UX. How responsibly these layers are combined—whether through clear disclosures, sane default leverage limits, or community norms around oracle quality—will shape whether HIP‑3’s growth curve continues smoothly or is punctuated by high‑profile blow‑ups.

HIP-3 framework launches on Hyperliquid mainnet

Active trader count hits record 231,000 as RWA perps boom

HIP-3 open interest crosses $2B; tokenized equities overtake metals

Felix selects RedStone oracle for HIP-3 perp markets citing $600M DeFi loss landscape

Hyperliquid May perps volume reaches record 6.63% of global CEX total, driven by HIP-3

SPCX SpaceX pre-IPO perp generates ~$1.4B on IPO day, $3.1B cumulative over 9 days

HIP-3 daily volume hits $5.4B record; RWA open interest surpasses $2.3B ATH

RWA open interest on Hyperliquid reaches new ATH of $3B

Risks, Challenges, and Criticisms

Oracle and Infrastructure Risk

Despite its successes, HIP‑3 significantly expands the attack surface for oracle and infrastructure failures. Because deployers are free to choose their own oracle providers and configurations, the quality of price feeds can vary widely across markets. While pioneering stacks like RedStone’s HyperStone have set a high bar—with a three‑tier design, geographically distributed infrastructure in Asia to match Hyperliquid node latency, and a 4‑of‑6 multisig quorum—there is no guarantee that all builders will adopt similar standards. In practice, some may opt for cheaper, less redundant setups using weaker multisigs or even single operators, re‑introducing the very single points of failure that have caused hundreds of millions of dollars in DeFi losses.

The stakes are particularly high for RWA markets referencing thinly traded or off‑hours assets. A misconfigured oracle for a pre‑IPO equity or emerging‑market commodity could publish stale or manipulated prices for hours, leading to erroneous liquidations and windfall gains or losses for counterparties. Because HIP‑3 markets share a unified collateral pool, such failures can propagate beyond a single asset and destabilize the broader platform. While social recovery mechanisms—such as manual position adjustments or governance‑driven compensation—are possible, they undermine the predictability that professional traders demand. As HIP‑3 continues to scale, market participants are likely to scrutinize deployers’ oracle choices more closely, and high‑reputation oracle providers may become de facto gatekeepers for institutional capital.

Market, Leverage, and Liquidity Risk

All perp trading carries inherent leverage risk, but HIP‑3 magnifies this by bringing leveraged exposure to assets that traders may not fully understand. RWA perps tied to bond yields, commodity curves, or idiosyncratic pre‑IPO valuations can behave very differently from crypto spot or BTC perps during stress events. An unexpected geopolitical shock that moves oil prices, or a regulatory announcement affecting a major tech stock, can trigger rapid repricing in HIP‑3 markets. When combined with high leverage, tight collateral buffers, and AI‑driven liquidity that can vanish as algorithms flip risk‑off, the result can be sudden liquidation cascades.

Liquidity is another key variable. While headline figures for HIP‑3 volume and open interest are impressive, flows are often concentrated in a handful of marquee markets: large‑cap crypto, top commodities, and high‑profile equity names like SPCX. Long‑tail markets may see much thinner order books, wider spreads, and sporadic activity, making them vulnerable to manipulation and slippage. Analytics from Artemis and other data providers show that HIP‑3’s share of total Hyperliquid volume varies by day and asset class, and internal dashboards and coverage like “HIP‑3 Volume by Asset: Hidden Risks Lurking in Daily USD Flows” emphasize that not all volume is created equal. For traders and risk managers, this means that careful attention to depth, OI distribution, and time‑of‑day liquidity is essential, especially in RWA and niche markets.

Regulatory and Compliance Uncertainty

The regulatory status of HIP‑3 markets is a looming, unresolved question. Synthetic perps that reference regulated securities, commodities, or pre‑IPO equities may fall within the purview of securities or derivatives regulators, even if the underlying assets never touch the blockchain. From the perspective of agencies like the SEC or CFTC, a HIP‑3 perp referencing a U.S. stock could be viewed as a security‑based swap or future, potentially subject to registration, reporting, and KYC/AML requirements for the entities offering or facilitating it. The fact that HIP‑3 markets are deployed by decentralized builders, run on a permissionless L1, and accessed via non‑custodial wallets complicates the traditional framework for enforcement but does not necessarily eliminate regulatory risk.

At the same time, HIP‑3 markets that trade around the clock and influence pre‑IPO price discovery may attract scrutiny from both securities and banking regulators. Questions around fair disclosure, insider trading, and information asymmetry become more acute when on‑chain markets respond instantly to rumors, leaked documents, or unverified social media posts. Builders and oracle providers may find themselves in ambiguous positions, simultaneously operating technical infrastructure and shaping economically significant reference prices for traditional markets. How regulators choose to interpret these roles—whether as unregistered exchanges, data vendors, or something entirely new—will have profound implications for the long‑term viability of HIP‑3‑style frameworks.

Systemic Considerations and CEX–DEX Interplay

Finally, as HIP‑3 grows, it becomes part of a broader systemic ecosystem that spans CEXs, DEXs, and TradFi venues. Recent episodes have shown that daily trading volume in TradFi perpetual bonds on centralized exchanges can exceed \(\$16\) billion, with Binance capturing the majority, while perp DEXs as a category have posted days with over \(\$6\) billion in volume, with Hyperliquid HIP‑3 accounting for a dominant share on some occasions. When liquidity and leverage are this tightly coupled across siloed but interdependent systems, shocks in one venue can rapidly spill into others.

Because HIP‑3 relies on CEX and TradFi prices for many RWA oracles, extreme events on centralized venues can produce violent moves on-chain, even if DeFi participants have no direct exposure to those off‑chain platforms. Conversely, if HIP‑3 markets become large enough to shape expectations about future spot prices—as in the SPCX pre‑IPO case—on‑chain sentiment may start influencing off‑chain order books and OTC flows. Managing this feedback loop will require not only robust oracle design but also thoughtful interactions between on‑chain builders, off‑chain data providers, and, eventually, regulators.

How Traders and Builders Use HIP‑3

Strategies for Traders: Macro, Hedging, and Cross‑Asset Plays

For traders, HIP‑3 markets open a wide array of strategies that blend crypto‑native and traditional exposures. A DeFi user who holds a portfolio of ETH and DeFi tokens, for example, can now hedge macro risks by shorting a HIP‑3 S&P 500 or crude oil perp, without ever opening a brokerage account. Conversely, a TradFi‑oriented trader who is bullish on tech equities but bearish on BTC can express that view entirely on-chain by going long a HIP‑3 Nasdaq‑style index while shorting BTC perps on the same platform. Because Hyperliquid’s risk engine can cross‑margin positions across HIP‑3 and native markets, traders can treat the whole platform as a unified book rather than juggling multiple venues and collateral balances.

RWA perps also facilitate more nuanced hedging. A user who holds tokenized treasuries or RWA yield products can hedge duration or credit risk using HIP‑3 fixed‑income or macro indices, assuming builders bring such markets online. Commodity producers or exporters who receive stablecoin payments might use HIP‑3 FX perps to lock in exchange rates between their local currency exposures and their on‑chain assets. While most of these use cases remain early, the basic ingredients—infrastructure, liquidity, and composability—are now present in a way that was unthinkable during the first DeFi cycle.

At the speculative end of the spectrum, HIP‑3 has become a playground for thematic and event‑driven trading. The SPCX perp is a prime example, but similar dynamics can apply to elections, regulatory decisions, product launches, or macro data releases that affect specific sectors or assets. As HIP‑3 expands into binary options and prediction‑style contracts via related proposals like HIP‑4 on testnet, the boundary between perps and prediction markets may blur further, giving traders even more avenues to express views on real‑world events directly from a DeFi wallet.

Opportunities for Builders: Launching Markets and Products

For builders, HIP‑3 offers a turnkey path to launching sophisticated derivatives markets without building base‑layer infrastructure from scratch. A team specializing in Latin American equities, for example, could develop a robust oracle stack for regional stocks, stake HYPE, and deploy a suite of index and single‑name perps tailored to their niche. They would immediately benefit from Hyperliquid’s existing liquidity, user base, and tooling while differentiating themselves via market coverage, branding, and fee incentives. Likewise, gaming or social‑fi projects can explore bespoke perp markets for in‑game assets, content creator metrics, or other vertical‑specific KPIs.

Ecosystem‑level initiatives like Based Launchpool illustrate how HIP‑3 can fit into broader product roadmaps. By incubating a TCG trading and gacha platform with real card inventory and revenue, and explicitly planning a path toward TCG perps via HIP‑3 and associated cloud infrastructure, builders can tie primary product utilization to derivative markets that provide both speculative and hedging functionality. HIP‑3 in this model becomes not just an exchange feature but a core monetization and engagement layer for entire on‑chain economies.

Builders can also stack additional protocols on top of HIP‑3 markets, such as structured products, vaults, or automated strategies that bundle multiple perp exposures into a single token. For example, a “global macro basket” vault could allocate capital across HIP‑3 FX, commodity, and equity perps, rebalancing programmatically and tokenizing the resulting strategy for secondary trading. Because all of these components live on-chain, they can compose with lending protocols, governance systems, and agent platforms like Virtuals, creating an increasingly intricate financial graph anchored around HIP‑3 liquidity.

HIP‑3 in the Competitive Landscape

HIP‑3 does not exist in a vacuum. Other RWA perp DEXs, such as Ostium, have launched with a focus on commodities, FX, indices, and stocks, often emphasizing dedicated UX and specialized risk models. Meanwhile, emerging venues like Canborsa are deploying perpetual RWA DEXs on networks like Canton, offering tokenized equities, commodities, and crypto under a non‑custodial interface tailored to institutional users. At the same time, major centralized exchanges have rolled out their own RWA derivatives, including perpetual bonds, tokenized treasuries, and synthetic macro indices, capturing daily volumes in the tens of billions.

In this landscape, Hyperliquid’s HIP‑3 has carved out a distinct niche as both the dominant on‑chain perps venue and the primary base layer for tokenized‑equity and pre‑IPO markets. Its strengths lie in a combination of deep crypto liquidity, a performant L1 optimized for order‑book trading, and a permissionless yet economically bonded listing framework. Competitors may offer tighter integration with specific institutional workflows or regulatory regimes, but HIP‑3’s open architecture and rapid iteration cycle appeal strongly to DeFi‑native builders and traders. Over time, it is plausible that HIP‑3, other RWA DEXs, and CEX offerings will form a continuum, with capital flowing between them based on regulation, liquidity, and counterparty preferences.

Builder-deployed markets rely on third-party deployers choosing their own oracle setups; the RedStone integration for Felix's markets highlights that oracle quality is deployer-dependent and inconsistent across the 100+ live markets.

Hyperliquid's validator set remains small relative to its trading volume, concentrating consensus risk even as HIP-3 market deployment is permissionless at the application layer.

Offering perpetuals on pre-IPO equity (e.g., SPCX/SpaceX) and registered commodities to global retail without KYC creates direct exposure to securities and derivatives regulation in multiple jurisdictions.

Open interest is heavily concentrated in a handful of marquee assets (crude oil, silver, SPCX); tail markets could face severe illiquidity and wide spreads during stress events.

24/7 perpetual trading of assets that only price during TradFi hours (equities, commodities) creates gap-open risk on Monday opens and after macro shocks when underlying spot markets are closed but the perp continues trading.

High leverage available on illiquid commodity and pre-IPO markets raises the probability of cascading liquidations that can temporarily disconnect the perp price from fair value with no exchange-level circuit breaker.

Outlook

Looking ahead, HIP‑3 is likely to remain a central driver of Hyperliquid’s evolution from a crypto‑native DEX into a general‑purpose, on‑chain derivatives exchange spanning both digital and traditional assets. The framework has already demonstrated its ability to host large, economically significant markets—from commodities like silver and crude oil to marquee equity exposures like SPCX—with volumes and open interest that rival mid‑tier centralized venues. If current trends continue, HIP‑3’s share of RWA perps volume and global perp trading activity could grow further, especially as more builders bring new asset classes and geographies on-chain.

At the same time, the very factors that make HIP‑3 powerful—permissionless listings, RWA exposure, AI‑driven trading, and tight CEX–DEX linkages—also heighten systemic risk. Oracle failures, liquidity shocks, and regulatory interventions are no longer hypothetical edge cases but real possibilities that participants must price in. The ecosystem’s response will likely involve continued professionalization of oracle providers, more stringent informal standards for HYPE deployers, and deeper collaboration between data vendors, builders, and risk managers. Projects like HyperStone show one path forward, but scaling such practices across dozens or hundreds of HIP‑3 markets remains a substantial challenge.

For traders and builders, the practical takeaway is twofold. First, HIP‑3 has opened up a genuinely new frontier: 24/7, on‑chain access to a broad spectrum of real‑world and digital assets, with leverage, composability, and self‑custody. Second, navigating that frontier safely requires a level of sophistication commensurate with the tools at hand. Understanding oracle design, funding dynamics, liquidity distribution, and regulatory headwinds is no longer optional for serious participants; it is part of the baseline skill set for operating in this new, hybrid market structure.

Whether HIP‑3 ultimately becomes a template for other chains, a proving ground for RWA derivatives before they migrate to more regulated venues, or a long‑term pillar of DeFi’s financial stack, its influence is already evident. It has reshaped how markets are launched, who controls price discovery, and where the boundary between crypto and TradFi is drawn. In that sense, HIP‑3 is not just a feature of Hyperliquid but a case study in how permissionless infrastructure can pull traditional finance one step closer to an always‑on, programmable, and globally accessible future.

Latest HIP-3 news

Sources

- https://hyperliquid.gitbook.io/hyperliquid-docs/hyperliquid-improvement-proposals-hips/hip-3-builder-deployed-perpetuals

- https://x.com/Grayscale/status/2067336590326911093

- https://defieducation.substack.com/p/understanding-hyperliquids-expansion

- https://bitsgap.com/blog/trading-gold-oil-and-stocks-on-chain-how-rwa-perps-work-in-2026

- https://hyperliquid.gitbook.io/hyperliquid-docs/for-developers/api/hip-3-deployer-actions

- https://classic.artemis.ai/asset/Hyperliquid?tab=deep_dives

- https://www.cmegroup.com/markets/energy/crude-oil/light-sweet-crude.html

- https://defillama.com/protocol/hyperliquid

- https://ourcryptotalk.com/news/hyperliquid-rwa-hip-3-3b-open-interest

- https://www.mexc.com/news/981977

- https://thedefiant.io/news/defi/builder-deployed-perp-markets-push-hyperliquid-to-record-share-of-global-perps-volume

- https://www.cryptopolitan.com/hyperliquid-hip-3-custom-markets-trades/

- https://blog.redstone.finance/2026/05/15/the-600m-warning-why-felix-chose-a-redstone-for-hip-3-perp-markets/

- https://x.com/virtuals_io/status/2066171168986644821

- https://www.mexc.co/en-NG/news/1157689

- https://x.com/WuBlockchain/status/2062413948985713097

- https://x.com/TheBlockCo/status/2062216782174187662

- https://www.cryptotimes.io/2026/03/24/hyperliquid-hits-record-231000-active-traders-as-rwa-perpetuals-boom/

- https://assets.coingecko.com/reports/2026/CoinGecko-2026-RWA-Report.pdf?ctcid=e00bb436-105d-427d-8c7e-e2c19a299cca

- https://x.com/BasedOneX/status/2040048826762072401

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…