In crypto, “seizure” covers government, court, and protocol moves that freeze or take control of BTC, USDT and other assets. This explainer unpacks legal tools, on‑chain mechanics, key cases and what they mean for custody, sanctions and user risk.

+7 sources across the wider coverage universe

AI chats ruled admissible in court as US judge denies legal privilege, prompting law firms to warn clients their conversations with tools like Claude can be seized2026-04

AI chats ruled admissible in court as US judge denies legal privilege, prompting law firms to warn clients their conversations with tools like Claude can be seized2026-04 Propr unveils Hyperliquid trading platform, providing up to $100,000 funding to seize trading opportunities.2026-04

Propr unveils Hyperliquid trading platform, providing up to $100,000 funding to seize trading opportunities.2026-04 Bitcoin linked to suspected steroid distribution conspiracy moved by U.S. authorities to Coinbase Prime, highlighting continued handling of seized crypto assets2026-04

Bitcoin linked to suspected steroid distribution conspiracy moved by U.S. authorities to Coinbase Prime, highlighting continued handling of seized crypto assets2026-04 Arizona passes SB 1649 and SB 1042 to establish a state digital asset reserve funded by seized crypto, avoiding taxpayer costs and advancing public sector adoption2026-04

Arizona passes SB 1649 and SB 1042 to establish a state digital asset reserve funded by seized crypto, avoiding taxpayer costs and advancing public sector adoption2026-04 Lawyer behind Arbitrum asset seizure case now targets Tether in bid to recover $344M in OFAC-frozen USDT linked to Iran’s Revolutionary Guard2026-05

Lawyer behind Arbitrum asset seizure case now targets Tether in bid to recover $344M in OFAC-frozen USDT linked to Iran’s Revolutionary Guard2026-05 US Treasury crosses $1 billion in seized Iranian crypto under Operation Economic Fury, mostly USDT on Tron2026-05

US Treasury crosses $1 billion in seized Iranian crypto under Operation Economic Fury, mostly USDT on Tron2026-05

Seizure In Crypto: How Governments, Courts, And Protocols Take Control Of Digital Assets

In the digital asset world, “seizure” refers to the process by which a government, court, platform, or protocol takes control of cryptocurrency or freezes a user’s ability to move it, usually on the basis of alleged illegality, regulatory breach, or contractual terms. Although crypto is often marketed as unconfiscatable, the last few years of enforcement actions, sanctions campaigns, and bankruptcy cases have shown that Bitcoin, stablecoins, and other tokens are routinely seized, frozen, and redistributed at scales that now reach into the tens of billions of dollars.

What “Seizure” Means In Crypto

At its core, seizure is a legal concept: an authority asserts control over property, depriving the previous holder of the ability to use it, typically pending a court determination about whether that property should be permanently forfeited. In the United States, both federal and state civil forfeiture regimes allow cryptocurrency to be seized based on allegations that it is connected to unlawful activity, even if the owner is never charged with a crime. Under these statutes, the digital asset itself is often treated as the defendant, and the legal question is whether that asset is “guilty” of being proceeds or instrumentalities of crime. For crypto users, this can be counterintuitive, because their focus is usually on account ownership, private keys, and exchange balances rather than on the property-law status of tokens in the eyes of the state.

In crypto markets and media, however, the word “seize” is also used metaphorically, such as when traders “seize” an arbitrage opportunity or when Ethereum advocates “seize on” a competitor’s technical scare to argue for ETH as the dominant venue for censorship‑resistant finance. This figurative usage appears in broader tech and retail coverage as well, for example when Google’s retail leadership talks about conversational search and AI overviews helping merchants “seize untapped opportunity” in digital commerce. The coexistence of literal and metaphorical meanings matters for readers, because headlines about “seized crypto” may refer either to regulatory enforcement or simply to aggressive market positioning. A careful reader needs to distinguish between government‑led asset seizure and rhetorical claims about seizing momentum.

In the narrow sense relevant to law and regulation, seizure is distinct from related concepts such as “freezing” and “forfeiture.” Freezing typically describes a situation where a wallet, account, or specific token balance can no longer move, but formal ownership has not yet changed; forfeiture, by contrast, is the legal process by which a seized asset is permanently transferred to the state or to victims after judicial proceedings. Blockchain law practitioners report that in practice, most real‑world “blockchain law” disputes involving seizure revolve around wallet freezes, exchange account locks, seizure warrants served on custodians, and subsequent forfeiture litigation to determine whether the government may keep or dispose of the assets. Understanding these distinctions is essential to evaluating what any given announcement about seized Bitcoin or USDT actually means for users, creditors, or victims.

The rise of large, custodial intermediaries has made seizure much easier to execute than many early Bitcoin advocates anticipated. Legal scholars have emphasized that cryptocurrency investors often fail to appreciate the credit and insolvency risks associated with custodial holdings and do not price this risk into their behavior. When assets are held on an exchange or in an ETF‑like structure, users frequently hold a contractual claim rather than direct control of on‑chain keys, which means courts and regulators can reach those assets in ways that resemble the seizure of bank deposits or brokerage accounts. This distinction underlies the enduring “not your keys, not your coins” slogan and informs why some long‑time Bitcoiners argue that only cold‑stored BTC in self‑custody is meaningfully outside the easy reach of routine seizures.

AI chats ruled admissible in court as US judge denies legal privilege, prompting law firms to warn clients their conversations with tools like Claude can be seized

Readers click seizure stories not for enforcement mechanics but for the power-inversion: governments are becoming crypto's largest accidental institutional holders, criminal proceeds are being legislated into state budgets, and centralized stablecoins have proven to be direct enforcement instruments of foreign policy — inverting every 'crypto escapes government' premise simultaneously.↗

Legal Foundations: How Authorities Get To Your Coins

Civil And Criminal Asset Forfeiture Basics

Modern crypto seizures sit within the longer history of civil and criminal asset forfeiture, a set of mechanisms that allow governments to confiscate property tied to crime or regulatory violations. In criminal forfeiture, the state typically seeks to take assets after a criminal conviction, arguing that funds are the proceeds of or tools used to commit an offense. Civil forfeiture, which has become prominent in the crypto context, proceeds directly against the property—such as a specific Bitcoin wallet or Ethereum address—without requiring a conviction of the owner, only proof that the property is linked to unlawful conduct. Because the case is nominally against the asset rather than the person, procedural protections for owners can be weaker, and the burden often shifts to them to prove lawful origin and innocent ownership once their tokens are seized or frozen.

In blockchain practice, this legal framework manifests when law enforcement obtains a seizure warrant, serves it on an exchange, and compels the platform to transfer crypto from a user’s account into government‑controlled wallets. A Tampa‑based blockchain law firm notes that agencies frequently rely on blockchain tracing to allege illicit activity, then use those analyses as the basis for seizure warrants or civil forfeiture complaints targeting both hosted and non‑custodial wallets. These actions can unfold even where the nominal owner of the address has not been charged, and in some cases may never be charged, leaving them to navigate a civil litigation process to try to recover their coins. For large cases, the Department of Justice often pairs criminal indictments with separate civil forfeiture complaints, particularly when third‑party interests or overseas assets complicate direct criminal forfeiture.

The now‑famous Silk Road investigations illustrate how the United States has applied traditional forfeiture tools to Bitcoin. In one historic case, federal prosecutors in the Southern District of New York described a “historic” seizure of approximately 50,676 Bitcoin from Georgia resident James Zhong, who had defrauded the Silk Road marketplace. In November 2021, pursuant to a judicially authorized premises search warrant, law enforcement searched Zhong’s Gainesville home and seized Bitcoin then valued at more than 3.36 billion dollars. These coins, held for nearly a decade in hidden stashes and sophisticated address structures, were ultimately transferred to government‑controlled wallets and became subject to forfeiture proceedings. The scale of this action signaled that large Bitcoin holdings, even when dormant for years, remained within reach of determined investigators using on‑chain forensics and traditional search powers.

Civil forfeiture has proven particularly attractive in cross‑border and sanctions‑related contexts, where charging foreign officials or entities in U.S. criminal courts may be politically or practically difficult. In those cases, prosecutors may file complaints against the assets themselves—often denominated as “Defendant Cryptocurrencies”—and seek court orders vesting title in the U.S. government. Once forfeiture is granted, agencies such as the U.S. Marshals Service can dispose of the crypto, typically by selling it on exchanges or via auctions and distributing proceeds according to statutory schemes that may include restitution for victims or deposit into law‑enforcement funds. As a result, seizure and forfeiture have become central tools in the toolkit not only for domestic fraud and hacking cases, but also for geopolitics and sanctions enforcement.

Sanctions, OFAC, And National Security

Beyond conventional crime, seizure powers are now deeply intertwined with sanctions regimes, particularly those administered by the U.S. Department of the Treasury’s Office of Foreign Assets Control (OFAC). OFAC maintains the Specially Designated Nationals (SDN) list, which identifies individuals, entities, and increasingly cryptocurrency addresses with which U.S. persons are generally prohibited from transacting. In April 2026, OFAC updated the designation of the Central Bank of Iran, adding new cryptocurrency addresses associated with the bank to the SDN list as part of a broader clampdown on Iran’s digital asset use. This step formalized what had already been happening on-chain: Tether, the issuer of USDT, announced that it collaborated with U.S. law enforcement to freeze 344 million dollars’ worth of USDT across two Tron addresses tied to the Central Bank of Iran and Iran’s Islamic Revolutionary Guard Corps (IRGC).

Those freezes are one piece of a larger Treasury‑led campaign dubbed Operation Economic Fury, launched around March 2025 under the Trump administration with the explicit goal of cutting Tehran off from overseas revenue streams and digital asset infrastructure. According to Rare Evo’s reporting on statements by Treasury Secretary Scott Bessent, the United States has seized roughly 1 billion dollars’ worth of cryptocurrency from entities linked to Iran’s military since conflict expanded, largely focused on USDT holdings on the Tron blockchain. An asset‑recovery analysis notes that this is part of a coordinated offensive combining sanctions, port blockades, and aggressive use of OFAC tools to shut down Iran’s shadow banking system, including offshore bank and crypto accounts. Commentators aligned with Bessent emphasize that modernized OFAC capabilities not only freeze accounts but increasingly seize them outright, particularly crypto accounts that can be directly transferred or rendered unusable.

The 344 million dollar USDT freeze has also opened new frontiers in the legal treatment of sanctions‑linked crypto. Tether’s move effectively placed those tokens in limbo: they remain visible on-chain but cannot be moved by the sanctioned holders, and their ultimate disposition is subject to ongoing legal and political negotiations. A group of American terrorism victims with unsatisfied court judgments against Iran totaling more than 2.4 billion dollars has asked a Manhattan federal court to order that the 344 million dollars in frozen USDT be transferred to their attorneys to satisfy those judgments. The case forces courts to confront whether OFAC‑frozen stablecoins are attachable assets that can be redirected to private plaintiffs, or whether they must remain blocked under sanctions rules unless and until the U.S. government chooses to seize and redistribute them.

Jurisdiction, Scam Compounds, And International Cooperation

Crypto seizure law is also being shaped by the fight against transnational fraud and human trafficking. In a striking example, U.S. authorities recently indicted Cambodian national Chen Zhi, also known as Vincent, the founder and chairman of Prince Holding Group, for directing forced‑labor scam compounds across Cambodia that engaged in cryptocurrency fraud schemes. Alongside the criminal indictment, the U.S. Attorney’s Office for the Eastern District of New York and the Justice Department’s National Security Division filed a civil forfeiture complaint targeting approximately 127,271 Bitcoin—described as proceeds and instrumentalities of the fraud and money laundering schemes—that had been stored in unhosted wallets controlled by Chen. At current values, those Bitcoin are worth around 15 billion dollars, and the complaint marks the largest single forfeiture action in the Justice Department’s history, with the funds already in U.S. government custody.

This Prince Group case fits within a broader global crackdown on so‑called “scam compounds” operating in Southeast Asia and the Middle East. According to a Fox News report cited by commentators, the FBI has seized more than 8 billion dollars’ worth of cryptocurrency and arrested nearly 300 suspects as part of an operation targeting scam compounds in Myanmar, Cambodia, Thailand, and the United Arab Emirates. The bureau described this as the largest cryptocurrency forfeiture in U.S. government history, a characterization echoed in asset‑recovery commentary that notes the operation also freed close to 2,000 trafficking victims who had been forced to work in these scam centers. That same commentary refers to this enforcement wave as Operation Blackout, and emphasizes that law enforcement seized more than 8 billion dollars in digital assets over the course of just one week, illustrating how quickly the seizure machinery can move once cross‑border coordination is in place.

The Prince Group and scam compound cases highlight the importance of international cooperation in executing seizures. Many of the scam operations reside in jurisdictions with weak rule of law or limited capacity, yet they rely on major global exchanges and stablecoins headquartered in or interfacing with jurisdictions like the United States where enforcement tools are stronger. By tracing flows through these centralized chokepoints, U.S. authorities can often identify points where they can compel custodians or stablecoin issuers to freeze or surrender funds, even if the underlying conduct took place in offshore compounds run by foreign nationals. This dynamic underscores why seizure is not merely a domestic criminal justice issue; it has become a core instrument of international financial regulation and geopolitical strategy in the crypto era.

How Crypto Seizures Actually Work On‑Chain

Custodial Seizures: Exchanges, Brokers, And ETFs

In practice, most high‑profile crypto seizures do not involve brute‑forcing private keys or exploiting protocol‑level vulnerabilities. Instead, they target centralized custodians such as exchanges, brokers, and ETF providers that hold assets on behalf of many customers in omnibus wallets. When law enforcement obtains a seizure warrant or court order, it can serve that order on the custodian, which then freezes specific user accounts and transfers the relevant cryptocurrency to wallets controlled by the seizing agency. From a technical perspective, the transaction looks like any other transfer on the blockchain, but from a legal perspective, it reflects a compelled reallocation of control based on statutory authority and judicial oversight.

The ongoing FTX and Alameda Research saga provides a clear illustration of this custodial seizure pathway. FTX and Alameda filed for bankruptcy on November 11, 2022, triggering investigations into alleged fraud and misuse of customer funds. In the course of those investigations, the U.S. government seized various crypto assets tied to Alameda and FTX, which are now held in wallets labeled accordingly on‑chain. On at least one recent occasion, observers noted that a wallet identified as “U.S. government (FTX Alameda Seized Funds)” deposited 98,590 Chainlink (LINK), worth about 768,000 dollars, to Coinbase Prime. That movement likely reflects the transition from seizure and forfeiture to disposition, with the government transferring tokens to a regulated trading venue where they can be sold, potentially with proceeds eventually directed to the FTX bankruptcy estate for distribution to creditors.

Legal academics note that investors who hold crypto through such intermediaries face unpriced credit and seizure risks because their relationship is often that of an unsecured creditor to the platform rather than direct owner of specific coins. This means their access can be cut off not only by the platform’s own insolvency or hacking, but also by regulators who compel the custodian to surrender assets without negotiating with end‑users. This logic extends to Bitcoin exchange‑traded products, where investors own shares in a fund rather than private keys to on‑chain BTC, leading some veteran Bitcoin advocates to argue that ETF holdings are “paper assets” that can be easily seized in ways that cold‑stored Bitcoin cannot. While seizure of ETF or brokerage positions still requires legal process, the path is far more straightforward than prying a hardware wallet out of an individual’s safe.

Stablecoin Blacklists And The Power To Freeze Tokens

Stablecoins introduce a distinct seizure and freezing vector because many of them are implemented as smart contracts with centralized administrative controls. Tether’s handling of USDT associated with Iran’s Central Bank and IRGC demonstrates how this works. In April 2026, following investigative work linking certain Tron addresses to Iranian entities, Tether announced that it had blacklisted two addresses holding a combined 344 million dollars in USDT, effectively freezing those tokens. Chainalysis notes that this action was taken in close collaboration with U.S. law enforcement and coincided with OFAC’s decision to add those cryptocurrency addresses to the SDN list under the Central Bank of Iran designation. On‑chain trackers confirm that the addresses, identified by their Tron strings, were frozen on April 23, 2026, and their balances remain immobile.

From a technical standpoint, USDT tokens remain in the sanctioned addresses, but the Tether contract simply refuses to process any transfer or redemption involving them, rendering them economically dead. Chainalysis emphasizes that such freezing capabilities allow stablecoin issuers to help law enforcement disrupt illicit activity and prevent further misuse of tokens; in many cases, frozen assets will later be the subject of forfeiture or court‑ordered redistribution. However, for ordinary users, this underscores that holding USDT in a self‑hosted wallet does not fully insulate one from seizure‑like outcomes; if the address becomes associated with sanctions or other enforcement priorities, the issuer can unilaterally immobilize the tokens, regardless of whether the user still controls the private key.

The interplay between OFAC actions and issuer freezes is becoming more intricate as sanctions policy adapts to crypto. In the Iranian context, Treasury officials have identified digital assets as a growing part of Iran’s strategy to circumvent conventional banking channels, with estimates suggesting that Iran’s total digital asset holdings may be around 7.7 billion dollars, roughly half of which are attributed to the IRGC. Operation Economic Fury aims to systematically degrade Tehran’s ability to generate, move, and repatriate funds, and the 344 million dollar USDT freeze is a key component of that effort. Yet the legal status of these frozen stablecoins remains unsettled, particularly as terrorism victims and other claimants seek court orders to seize them from Tether’s control and redirect them to satisfy judgments, moving them from a “freeze” state into outright seizure and eventual forfeiture.

Seizing Self‑Custodied Coins: Keys, Searches, And Operational Errors

For self‑custodied Bitcoin and other cryptocurrencies held in hardware wallets or on air‑gapped devices, seizure is more difficult but not impossible. Law enforcement generally cannot override the cryptography protecting a private key; instead, they rely on the same tools available in traditional investigations: search warrants, subpoenas, informants, and operational mistakes by the target. The James Zhong case is instructive. Zhong had exploited a bug in the Silk Road withdrawal system to obtain Bitcoin, which he then held in various hidden wallets for years. When federal agents executed a search warrant at his Gainesville residence in November 2021, they discovered hardware devices and other storage media containing the private keys to addresses holding nearly 50,676 Bitcoin. Using those keys, the government transferred the BTC into its own wallets, executing one of the largest physical‑world crypto seizures on record.

Blockchain law practitioners emphasize that seizure of self‑custodied assets usually requires either physical access to devices, compelling disclosure of passphrases and seeds, or leveraging human weaknesses such as reuse of passwords, poorly secured backups, or coerced cooperation by insiders. In some jurisdictions, courts have wrestled with whether and to what extent individuals can be compelled to reveal passphrases or mnemonic phrases, given protections against self‑incrimination; the law here is still evolving, and outcomes may vary by country. Regardless, once authorities have keys in hand—whether obtained voluntarily, through plea negotiations, or via investigative work—they can move self‑custodied coins just like any other, demonstrating that “unseizable” is more a matter of practice than of absolute technical guarantee.

Self‑custody can nonetheless meaningfully change the risk profile. Legal scholars point out that when you hold assets directly, the state must find and compel you, while with custodial holdings, it can bypass you and target the intermediary. This helps explain why some long‑time Bitcoiners, including figures like the 70‑year‑old former fighter pilot highlighted in recent coverage, insist that only cold‑stored BTC “truly belongs to you” in a robust sense. That said, physical‑world risks such as theft, coercion, and even violent attacks (“$5 wrench attacks”) persist, and courts can still order individuals to surrender their assets as part of judgments, divorce settlements, or bankruptcy proceedings, making absolute immunity from seizure more aspiration than reality.

Freezing, Seizing, And Forfeiting: Key Distinctions

To understand any particular enforcement action, it is useful to distinguish among freezing, seizure, and forfeiture. A freeze generally means that an asset cannot be moved or accessed, but its ownership has not yet been formally transferred to another party. A seizure refers to the act of taking physical or constructive control of an asset, usually through legal process such as a warrant or court order. Forfeiture is the subsequent judicial declaration that the asset is permanently transferred to the government or another party, often victims, extinguishing the original owner’s rights. These steps may blur in public reporting, but they are distinct phases with different implications for appeal and restitution.

The following table summarizes the differences:

| Concept | Who controls the asset? | Legal status of ownership | Typical examples |

|---|---|---|---|

| Freeze | Original holder or custodian, but constrained | Ownership unresolved; subject to further legal process | OFAC‑blocked USDT in Iranian addresses |

| Seizure | Government or enforcing authority | Ownership presumptively still contested | DOJ taking custody of Zhong’s 50,676 BTC |

| Forfeiture | Government or court‑designated beneficiary | Ownership legally transferred, prior claims extinguished | 127,271 BTC in Prince Group forfeiture complaint |

As Chainalysis notes, freezing can be particularly valuable when law enforcement wants to stop ongoing misuse of funds, for example by preventing stablecoins from being cashed out while investigations continue. In many cases, stablecoin issuers or exchanges will first freeze assets and only later, once court orders are obtained, transfer them to government accounts as part of seizure and forfeiture. The Iranian USDT addresses are a current example: at present, Tether has frozen them, OFAC has designated them, and multiple parties are vying to determine whether they will eventually be seized and forfeited to the U.S. government or reallocated to private claimants.

Legal ambiguity is not limited to sanctions cases. In New York, a plaintiff has attempted to use state lost‑and‑found law to claim nearly 40,000 Bitcoin wallets as lost property, arguing that dormant wallets might be treated analogously to abandoned bank accounts. A New York judge has paused the lawsuit and scheduled a hearing to evaluate whether the lost‑and‑found framework even applies to crypto, highlighting the extent to which basic property‑law questions remain unsettled in the digital asset domain. If courts were to endorse such theories, it could open a new category of quasi‑seizure, where private actors use civil courts to wrest control of long‑inactive crypto from unknown holders.

Propr unveils Hyperliquid trading platform, providing up to $100,000 funding to seize trading opportunities.

$999 buy-in for a $100K account with 6% max drawdown at 5x leverage — one bad wick on a 1.2% move against you and the challenge is over. Onchain execution via Hyperliquid at least solves the payout trust problem that's plagued every TradFi prop firm clone in crypto, though challenge fee economics still heavily favor the house regardless. SwissBorg backing (900K+ users, $1.5B AUM) gives them distribution most onchain prop desks will never have — but Hyperliquid's perps book is going to feel it when a wave of funded traders all pile into the same positions.

- 01US government as Bitcoin whale↗

The headline that federal seizures made the US one of the largest BTC holders drew the highest clicks by directly collapsing crypto's anti-establishment premise into absurdity.

- 02Ransomware and darknet busts↗

LockBit, Silk Road follow-on seizures, and darknet marketplace takedowns each demonstrated that blockchain's forensic permanence catches criminal operations years after the fact, making every bust a lesson in traceability.

- 03Iran sanctions via stablecoins↗

Operation Economic Fury crossing $1 billion and the $344M OFAC-frozen USDT case revealed that Tether and other centralized stablecoin issuers function as de facto arms of US foreign policy enforcement.

- 04Seized crypto as public revenue

Brazil directing seized Bitcoin to police budgets and Arizona establishing a state digital asset reserve from forfeited assets signal that governments have normalized criminal crypto as a recurring funding stream.

- 05No-conviction confiscation laws

Sweden's law enabling seizure of assets with no explainable origin — without proof of a crime — and Brazil's anti-gang law represent a global expansion of civil forfeiture into crypto that readers flagged as a due-process frontier.

- 06Civil asset recovery litigation↗

Lawyers pursuing Tether directly for $344M in OFAC-frozen USDT showed readers that crypto seizure is increasingly contested through novel civil legal theories, not just criminal enforcement.

Case Studies: Seizure In Action

Silk Road, James Zhong, And The Era Of Mega‑Seizures

The Silk Road saga continues to shape how both regulators and the public understand crypto seizure. Silk Road was an early dark web marketplace that used Bitcoin for narcotics and other illicit sales, and its takedown in 2013 sparked waves of enforcement against associated wallets. James Zhong, who pleaded guilty to committing wire fraud against Silk Road, had taken advantage of vulnerabilities in the marketplace’s withdrawal mechanisms around 2012 to generate large BTC payouts. He then scattered these coins across a variety of addresses and, for nearly a decade, avoided detection while Bitcoin’s price rose dramatically, turning what had been millions into billions of dollars.

In November 2021, law enforcement executed a search warrant at Zhong’s home and discovered devices containing private keys to addresses linked to the stolen Silk Road funds. The subsequent seizure of approximately 50,676 Bitcoin—valued at more than 3.36 billion dollars at the time—was hailed by federal prosecutors as one of the largest cryptocurrency seizures in U.S. history. The case illustrated that, despite the pseudonymous nature of Bitcoin addresses, long‑term storage does not guarantee safety from law enforcement tracing, especially when on‑chain analytics can correlate movements, clustering, and interactions with known service providers. It also demonstrated the importance of old‑fashioned investigative work; the breakthrough came not from breaking Bitcoin’s cryptography but from identifying and searching Zhong and his physical environment.

Silk Road‑linked seizures have also provided precedents for how governments dispose of confiscated Bitcoin. In earlier phases of the case, the U.S. Marshals Service auctioned off seized BTC to private investors, including well‑known figures who publicly embraced their new holdings. In newer cases like Zhong’s, sales are more likely to occur via regulated exchanges or OTC desks, sometimes labeled as “U.S. government” wallets on on‑chain analytics platforms and tracked by traders who watch for potential market impact. These high‑visibility disposals have helped normalize the idea that governments not only seize but also manage and trade digital assets, even as policy debates continue over the wisdom and timing of such sales.

Forced‑Labor Scam Compounds, Operation Blackout, And 127,271 Bitcoin

The indictment of Prince Group chairman Chen Zhi and the associated forfeiture complaint against 127,271 Bitcoin mark a new frontier in scale and complexity for crypto seizures. According to the unsealed indictment, Chen allegedly directed forced‑labor scam compounds across Cambodia, where individuals were coerced into operating online fraud schemes targeting victims globally, many involving cryptocurrency transactions. Prosecutors allege that these activities generated enormous Bitcoin holdings funnelled into unhosted wallets whose private keys Chen controlled, making them both proceeds and instrumentalities of wire fraud and money laundering conspiracies. By filing a civil forfeiture complaint in U.S. court, the Justice Department is seeking to convert those holdings—currently in U.S. custody—into government property.

In parallel, the FBI has described a global crackdown on scam compounds operating across Myanmar, Cambodia, Thailand, and the UAE, announcing that it seized more than 8 billion dollars in cryptocurrency and arrested nearly 300 suspects. Asset‑recovery analysis argues that this enforcement wave, dubbed Operation Blackout, is unprecedented in speed, aggregating more than 8 billion dollars in seized digital assets in a single week. The operation is also notable for its human impact, with around 2,000 trafficking victims reportedly freed from forced labor in scam centers as part of the raids. These victims, often lured with promises of legitimate employment, found themselves imprisoned and forced to carry out phishing, romance scams, and fake investment pitches, many denominated in crypto.

The Prince Group Bitcoin and Operation Blackout seizures underscore how deeply digital assets have penetrated transnational crime networks and how central they have become to modern law enforcement narratives. They also highlight the challenge of victim restitution. With so many global victims, varying degrees of complicity among local officials, and complex jurisdictional issues, determining who should ultimately receive the benefit of seized assets is nontrivial. Civil forfeiture proceedings provide one mechanism for courts to consider petitions from victims and other claimants, but they also raise concerns about due process and transparency, especially when much of the investigative record remains sealed due to ongoing operations.

Iran, Operation Economic Fury, And OFAC‑Frozen USDT

The U.S. campaign against Iranian crypto use offers a case study in how seizures and freezes can function as instruments of economic pressure. As noted earlier, Operation Economic Fury is a Treasury‑led initiative started in 2025 to degrade Tehran’s ability to fund military and proxy activities, including through digital assets. Rare Evo reports that by the spring of 2026, U.S. authorities had seized roughly 1 billion dollars in cryptocurrency linked to Iran’s military, including significant USDT holdings on Tron. Scott Bessent, speaking at the Reagan National Economic Forum, framed these actions as part of a broader effort that includes blocking Iranian ports, shutting down shadow banking channels, and modernizing OFAC’s capabilities to freeze and seize offshore bank and crypto accounts.

Chainalysis’s analysis of OFAC’s April 24, 2026 update to the Central Bank of Iran’s designation offers technical detail about how these seizures intersect with sanctions. Treasury added two specific cryptocurrency addresses to the Central Bank’s SDN entry and noted that they had been used to receive and move USDT ultimately tied to Iranian entities. Around the same time, Tether publicly announced that it had frozen 344 million dollars’ worth of USDT across those addresses in coordination with U.S. authorities. U.S. officials told CNN that the seized funds were linked to Iran via transactions involving Iranian exchanges and intermediary addresses that interacted with wallets associated with the Central Bank of Iran. On‑chain monitoring tools corroborate that both Tron addresses were frozen on April 23, 2026, consistent with Tether’s statements.

The political stakes around these frozen stablecoins are high. Asset‑recovery commentary notes that Iran’s estimated total digital asset holdings, at around 7.7 billion dollars, dwarf the 1 billion dollars seized so far, suggesting that Operation Economic Fury is exerting significant but not decisive pressure. Meanwhile, terrorism victims with large unpaid judgments against Iran are asking U.S. courts to treat the frozen USDT as attachable assets that can be seized and handed over to them, effectively turning a sanctions freeze into a private seizure. Lawyers who have previously litigated high‑profile crypto seizure disputes, such as those involving Arbitrum assets, are reportedly testing new theories to compel Tether and other intermediaries to transfer such frozen funds. Although outcomes remain uncertain, the case illustrates how seizure, sanctions, and civil judgment enforcement are converging in the stablecoin era.

FTX, Alameda, And The Government Trader

The bankruptcy of FTX and its sister trading firm Alameda Research has created a sprawling ecosystem of seizures, clawbacks, and asset sales. According to EBSCO’s overview of the case, FTX and Alameda filed for bankruptcy on November 11, 2022, leading to the appointment of new management and extensive investigations into alleged misappropriation of customer funds. In parallel, U.S. prosecutors pursued criminal charges against FTX founder Sam Bankman‑Fried and others, and the Justice Department seized various crypto assets linked to the alleged fraud. Some of these assets are now visible on‑chain in wallets labeled as U.S. government holdings of “FTX Alameda Seized Funds.”

In early 2026, blockchain analysts spotted activity from one of these wallets, noting that it had deposited 98,590 LINK, worth about 768,000 dollars, into Coinbase Prime. This transfer likely reflects the government’s practice of liquidating forfeited assets, either on its own behalf or in anticipation of returning proceeds to victims via the bankruptcy process. Asset‑recovery coverage notes that, in general, many Alameda and FTX assets seized by the Justice Department will eventually be turned over to the FTX estate or directly to creditors as part of restitution, meaning that seizure in this context serves as an intermediate step toward making users whole rather than an end in itself. Nevertheless, the optics of the U.S. government effectively becoming a trader—managing seized LINK, BTC, and other tokens through regulated venues like Coinbase Prime—illustrate how routine crypto seizure has become.

FTX also spotlights the interplay between seizure and the “not your keys, not your coins” principle. Many users who left assets on FTX assumed that, because the exchange dealt in crypto, they retained some form of special protection or separateness from the exchange’s balance sheet. In reality, as legal scholars emphasize, their claims were more akin to those of unsecured creditors of a traditional financial institution, vulnerable not only to mismanagement but also to seizure actions against the platform. When the DOJ seizes exchange‑controlled wallets, it effectively steps into the shoes of the platform, and only later, through bankruptcy and restitution proceedings, do individual customers have the opportunity to recover a share of what remains. This dynamic demonstrates that in the custodial context, seizure risk is collective and mediated through complex insolvency law rather than individualized control of private keys.

Dormant Wallets, Lost Property Laws, And Private Seizure Attempts

Not all seizure‑like efforts originate with governments. The New York lawsuit seeking to claim nearly 40,000 Bitcoin wallets as “lost property” exemplifies a private attempt to use state law to reassign control over dormant crypto. According to a summary posted by CoinMarketCap, the plaintiff argues that these wallets, which have shown no activity for years, should be treated under New York’s lost‑and‑found statutes, analogous to unclaimed safety deposit boxes or abandoned bank accounts. If successful, this theory could allow a private party to obtain court orders directing custodians or other intermediaries to convert crypto in long‑inactive wallets to their benefit.

A New York judge has paused this lawsuit and scheduled a hearing to examine whether the state’s lost‑and‑found law even applies to cryptocurrencies. The hearing, expected to occur in July, will test whether courts view private keys and on‑chain addresses as personal property that can be “lost” in the statutory sense, and whether state escheat or lost‑property frameworks can be extended to assets that may be deliberately left unmoved for ideological or strategic reasons. Many in the Bitcoin community regard such wallets as a form of long‑term cold storage or even deliberate “proof of reserves” by early adopters, and they worry that using dormancy as a proxy for abandonment could set a dangerous precedent.

Whatever the outcome, the case highlights the diversity of seizure mechanisms in the crypto ecosystem. Even without criminal allegations or sanctions designations, plaintiffs and creditors may attempt to use civil courts to gain control over crypto they argue has been abandoned or wrongfully held. In some cases, such as efforts by terrorism victims to attach Iranian assets, these moves may align with broader public policy goals. In others, such as mass claims on dormant Bitcoin wallets, they may be viewed as opportunistic grabs enabled by gaps in existing law. Courts will play a critical role in drawing boundaries around which forms of private seizure the law will tolerate.

Beyond Government: Private And Protocol‑Level Seizures

Exchange Liquidations, Margin Calls, And “Internal” Repossessions

Even when no court orders are involved, crypto users can experience events that feel like seizure when platforms exercise contractual rights to liquidate or repossess assets. On centralized exchanges, margin accounts and leveraged products typically give the platform the right to liquidate a user’s collateral if it falls below certain thresholds, often without prior notice. From the user’s perspective, their crypto disappears from their account, much as it would in a legal seizure. Legally, however, this is a private contractual exercise of security interests, not a state action.

The conceptual boundary matters because legal protections differ. In a government seizure, users may have statutory rights to contest the action, seek hearings, and assert innocent ownership defenses. In a margin liquidation or other “internal” repossession by a platform, their recourse is limited to whatever contractual and consumer protection rights they negotiated or are granted by regulation. Nonetheless, in both cases, the ability to unilaterally reassign control over crypto rests heavily with centralized intermediaries. This shared structural feature reinforces critiques that, despite decentralization rhetoric, much of the crypto economy operates on custodial rails vulnerable to both public and private seizure‑like events.

Decentralized finance (DeFi) protocols can exhibit analogous dynamics when governance mechanisms or smart contract designs allow for emergency pauses or reallocation of collateral. In some protocols, administrators or token‑holder votes can trigger functions that pause withdrawals, adjust haircuts, or even transfer assets from one contract to another in response to hacks or market shocks. While these actions are not “seizures” in the legal sense, they remind users that control over on‑chain assets can be constrained by social and governance structures, not just by private keys.

Protocol Admin Keys, Bugs, And Emergency Pauses

Many smart‑contract systems retain admin keys or privileged roles that can, in effect, seize or freeze user assets. Stablecoins like USDT and many DeFi platforms allow a designated account (often a multisig held by a company or DAO) to blacklist addresses, pause transfers, or upgrade contract logic. In benign scenarios, these powers are used to respond to hacks by freezing stolen funds or to comply with legal orders by blocking sanctioned addresses. In more problematic cases, they could be abused by insiders or captured by hostile actors, leading to unauthorized seizure‑like outcomes.

The choice to include or exclude such administrative controls is a design trade‑off. Systems without admin keys can credibly claim censorship‑resistance and immunity from certain forms of centralized seizure, but they also lose a valuable tool to recover from bugs and thefts. Systems with admin keys can coordinate rapid freezes to assist law enforcement or protect users, as Tether did in the Iranian USDT case, but at the cost of making all users’ tokens subject to potential unilateral action by the issuer. Chainalysis highlights how this trade‑off plays out in practice: by freezing assets at the issuer level, law enforcement can stop illicit activity quickly, but the same mechanism could, in theory, be used to freeze assets for less justified reasons.

Emergency pauses are particularly controversial when invoked in response to perceived protocol exploits. For example, when privacy‑focused projects like Zcash face rumors or partial disclosures about bugs, rivals may “seize on” those scares to argue that systems with more mature or institutionally accepted privacy stacks, such as Ethereum, provide better balances of censorship‑resistance and safety. Although this discourse is largely rhetorical, it interacts with substantive questions about which protocols afford users greater protection against both criminal theft and over‑broad seizure by authorities or administrators. Users choosing where to park their capital are implicitly weighing these trade‑offs.

Counter‑Seizures: Tracking Down Thieves And Recovering Funds

Not all seizures are adversarial to user interests; some are welcomed as successful recoveries of stolen funds. Independent blockchain sleuths, such as the pseudonymous investigator ZachXBT, frequently collaborate with law enforcement and exchanges to trace stolen or extorted crypto across chains. In at least one case highlighted by ZachXBT, law enforcement seized approximately 18.9 million dollars from actors involved in high‑profile social engineering fraud and data extortion targeting crypto users. These “threat actors,” sometimes mislabeled as “crypto entrepreneurs,” had allegedly orchestrated complex scams, and the seizure of their assets was seen as a victory for victims and for the broader ecosystem’s legitimacy.

Such counter‑seizures demonstrate both the strengths and limitations of public blockchains. On the one hand, the transparency of Bitcoin, Ethereum, and similar networks makes it easier to follow the money than with many traditional banking systems, especially when funds are moved across poorly regulated offshore exchanges. On the other hand, once stolen funds pass through mixers, privacy chains, or cross‑chain bridges, tracing can become more complex, and the ability to actually seize assets depends on cooperation from custodial intermediaries or the ability to identify and physically reach the perpetrators. In this sense, seizure is a double‑edged sword: the same techniques and legal tools used to clamp down on sanctions evasion and scam compounds also enable restitution for hacked or extorted users.

Language, Metaphor, And AI‑Powered Opportunity “Seizure”

Finally, it is worth returning to the metaphorical use of “seize” in tech and crypto discourse, particularly as it relates to AI and data. In retail and fintech, industry leaders now talk about conversational search and generative AI as helping firms “seize untapped opportunity” by better understanding customer intent and leveraging data more efficiently. A Google managing director for retail has described how image search and AI overviews in Google Search are transforming how consumers discover products, implying that retailers who adopt these tools will capture a larger share of demand. This rhetorical framing positions “seizure” not as taking property but as rapidly capitalizing on shifting technological landscapes.

In the crypto context, AI and data analytics are increasingly central to both market opportunity and enforcement. Companies like Chainalysis use advanced analytics, often incorporating machine‑learning techniques, to identify suspicious patterns, cluster addresses, and support law enforcement in seizing illicit funds. Regulators, in turn, see AI as a way to keep pace with the speed and complexity of digital asset flows, enhancing their capacity to detect sanctions evasion, fraud, and money laundering. On the market side, trading firms deploy AI‑driven strategies to “seize” fleeting arbitrage or liquidity opportunities across centralized exchanges, decentralized protocols, and layer‑2 networks.

Understanding the dual use of “seizure” in this environment helps readers interpret headlines and policy statements. When officials speak of needing to ensure that the government “can no longer seize people’s crypto assets,” they may be implicitly critiquing existing legal frameworks that allow for extensive seizure powers over custodial holdings and stablecoins. Conversely, when commentators say that “stablecoins and regulated digital asset platforms have seized the spotlight” amid fading altcoin momentum, they are using the term to describe market share gains, not enforcement actions. Clear contextual reading is essential to avoid confusion between legal seizure and metaphorical capture of attention or opportunity.

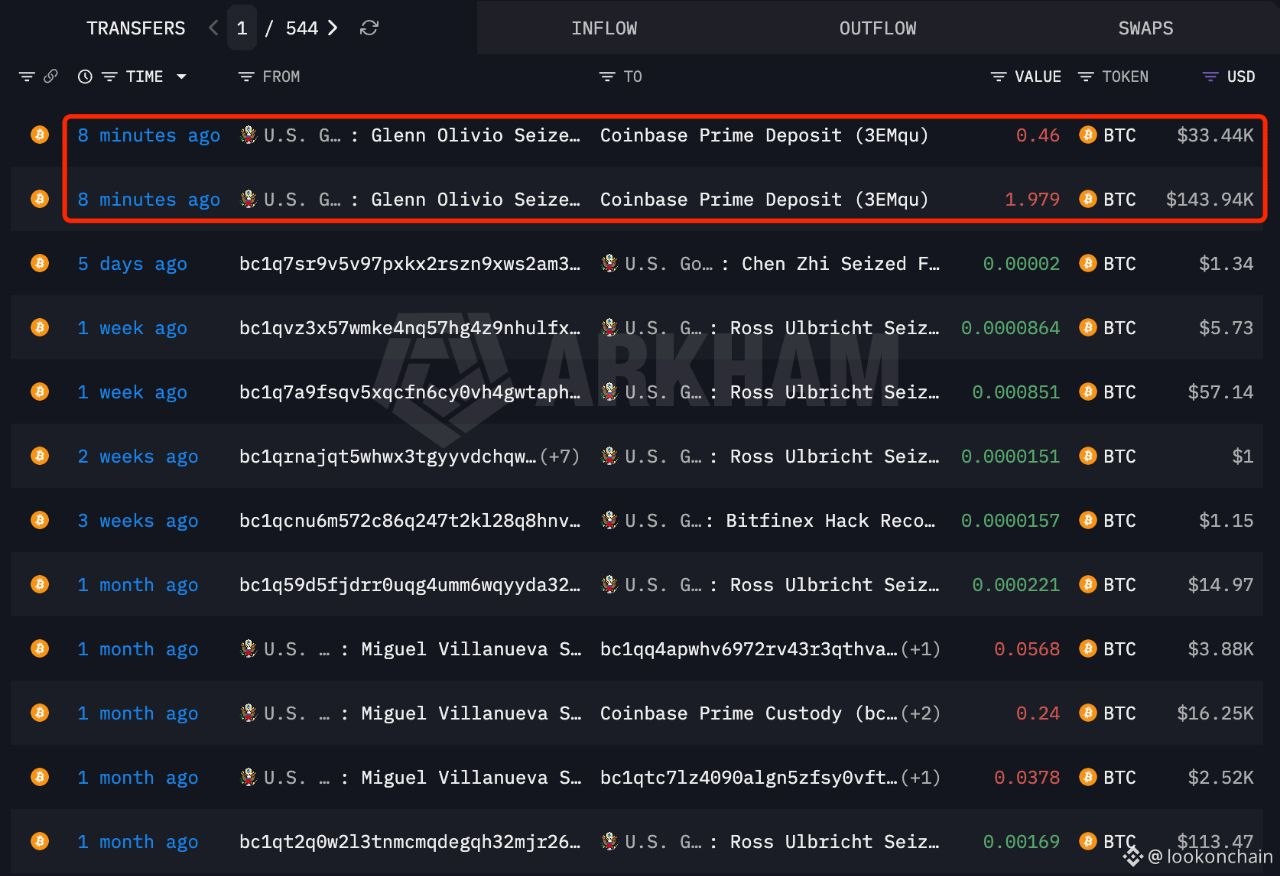

Bitcoin linked to suspected steroid distribution conspiracy moved by U.S. authorities to Coinbase Prime, highlighting continued handling of seized crypto assets

2.4 BTC from a steroid dealer getting the full Coinbase Prime custody treatment tells you how seriously the SBR pipeline is being enforced — every forfeiture, no matter how small, gets routed into the reserve now instead of hitting the USMS auction block. Coinbase is quietly becoming the government's de facto Bitcoin bank under that $32.5M custody contract, and at 328K+ BTC in the stockpile, the U.S. is accumulating faster through criminal forfeitures than most sovereign wealth funds do through open market buys. The old playbook of auctioning seized BTC at a discount (RIP Tim Draper-style deals) is dead.

FBI shuts down Silk Road, seizes ~144,000 BTC from site wallet

DOJ seizes $3.36B in Bitcoin linked to 2016 Bitfinex hack, largest crypto seizure at the time

Operation Cronos dismantles LockBit ransomware network; 200 crypto accounts seized, 10 wallets sanctioned

- 2024-11regulatory

Sweden new confiscation law takes effect, enabling seizure of assets with no explainable origin without conviction

OFAC designates Central Bank of Iran; $344M USDT tranche frozen on Tron network

US Treasury surpasses $1B in seized Iranian crypto under Operation Economic Fury, majority USDT on Tron

- 2025-05regulatory

Arizona passes SB 1649/1042 establishing state digital asset reserve funded by seized crypto

- 2025-06regulatory

Brazil President Lula signs Anti-Gang Law directing seized crypto to police funding without requiring conviction

Implications For Crypto Users And Platforms

Custody Risk: “Not Your Keys, Not Your Coins”

For everyday crypto users, the proliferation of seizure cases underscores the importance of understanding custody. Legal scholarship has argued that cryptocurrency investors generally do not account for the credit and seizure risks they assume when holding assets through custodians. When users deposit Bitcoin, Ethereum, or USDT on exchanges like Coinbase or within broker‑managed products, they often become unsecured creditors, relying on the intermediary’s solvency and compliance posture. In such scenarios, seizures targeted at the platform—whether for its own misconduct, like FTX, or for serving sanctioned or criminal customers—can sweep up user assets, leaving them to seek redress through lengthy bankruptcy and restitution processes.

The “not your keys, not your coins” maxim is a response to this structural vulnerability. In self‑custody, users hold private keys and interact directly with blockchains; while they may still be subject to government seizure, the state must identify and engage them individually rather than simply serving an order on a centralized custodian. This difference is particularly salient for those who fear over‑broad seizure or politically motivated enforcement. It has led some long‑time Bitcoiners, such as the former fighter pilot highlighted in recent coverage, to argue that only cold‑stored BTC genuinely lies outside easy seizure pathways and that ETF shares or custodial balances are at best claims on Bitcoin held by entities that can be compelled to surrender it.

However, self‑custody is not a panacea. Stablecoins like USDT remain vulnerable to issuer‑level freezes regardless of who holds the keys, as the Iranian case illustrates. Many users also rely on centralized venues for liquidity, yield products, and tax reporting, creating points of contact where their self‑custodied assets can become visible and potentially reachable by legal process. Moreover, the risks of loss, theft, or user error in self‑custody can be significant, as evidenced by countless stories of lost hardware wallets and unrecoverable seeds. Rational users must weigh seizure risk against operational risk, recognizing that both custodial and non‑custodial strategies involve trade‑offs rather than absolute security.

Geographic And Political Risk: Sanctions, Wars, And Regime Change

Seizure risk is not evenly distributed across geographies or political contexts. Operation Economic Fury demonstrates how residents of countries subject to sanctions or conflict can find their digital assets caught up in enforcement actions even if they themselves are not directly involved in wrongdoing. Iranian entities have turned to crypto, particularly USDT on Tron, as a way to bypass traditional banking restrictions, making those ecosystems targets for U.S. scrutiny. As OFAC expands its SDN list to include crypto addresses and Treasury coordinates freezes with stablecoin issuers, ordinary users may find themselves holding tainted tokens or transacting with blacklisted addresses unknowingly, with potential consequences for their own accounts.

The same is true, in different ways, for regions hosting scam compounds or other illicit operations. Individuals in Myanmar, Cambodia, Thailand, and the UAE who used certain exchanges or service providers may see withdrawals limited or accounts scrutinized as part of broader enforcement campaigns like Operation Blackout. Conversely, victims in wealthy jurisdictions may benefit from these seizures via restitution, while local workers coerced into scams might receive little direct compensation. These disparities raise questions about how seizure powers intersect with global justice and whether current frameworks adequately reflect the interests of those most harmed by abuse of crypto.

Political risk extends beyond sanctions and scams. Domestic policy shifts, changes in regulatory leadership, and evolving court interpretations can all alter seizure dynamics. For example, aggressive use of civil forfeiture to target crypto mixers or privacy tools could chill legitimate privacy‑seeking behavior, while legislative reforms could curtail certain forms of seizure or enhance procedural protections for owners. As debates unfold about the appropriate balance between law enforcement needs and financial freedom, crypto users must pay attention not just to protocol upgrades but also to legal and geopolitical developments that shape the environment in which seizures occur.

Compliance Burden For Exchanges And Stablecoin Issuers

Exchanges, custodians, and stablecoin issuers sit at the center of seizure and freezing operations and face growing compliance burdens. Tether’s collaboration with OFAC and U.S. law enforcement in freezing 344 million dollars in USDT linked to Iran is emblematic. The company had to rapidly identify relevant addresses, implement blacklists at the smart‑contract level, coordinate public statements, and prepare for litigation involving terrorism victims seeking access to the frozen funds. Exchanges like Coinbase must likewise be prepared to respond to seizure warrants, freezing specific user accounts, preserving records, and sometimes transferring assets to government wallets in a manner that minimizes market disruption while maintaining legal compliance.

Chainalysis notes that effective asset seizure often depends on such cooperation, with investigators relying on exchanges and issuers to rapidly freeze funds once suspicious activity is identified on-chain. These firms, in turn, must invest heavily in compliance infrastructure, including transaction monitoring, sanctions screening, and legal teams capable of handling complex multi‑jurisdictional requests. The costs of these systems are ultimately borne by users, whether through higher fees, more intrusive KYC, or limitations on the types of services platforms are willing to offer.

At the same time, platforms face reputational risks. Over‑zealous freezing or perceived collusion with controversial enforcement actions can alienate privacy‑conscious users and fuel narratives that centralized platforms are little more than extensions of the state. Under‑compliance, on the other hand, can lead to massive enforcement actions, fines, and even shutdowns. Some regulators have suggested that future frameworks should aim to protect genuinely self‑custodied assets from arbitrary seizure while ensuring that intermediaries remain fully accountable for their role in facilitating illicit activity. The precise contours of such a “future‑proof” space for crypto remain contested.

Privacy, Censorship‑Resistance, And The Myth Of “Unseizable” Bitcoin

The cumulative effect of Silk Road, Prince Group, Iranian, and FTX‑related seizures is to puncture simplistic claims that Bitcoin or other cryptocurrencies are intrinsically “unseizable.” As the Zhong case shows, on‑chain transparency combined with traditional investigative powers can lead to the recovery of massive BTC stashes even a decade after the underlying conduct. The Prince Group and Operation Blackout actions demonstrate that law enforcement can identify and take control of billions in crypto held in unhosted wallets across multiple jurisdictions. Operation Economic Fury reveals how stablecoins tied to real‑world reserves can be frozen at the contract level, effectively transforming them into dead assets or eventual government property.

At the same time, these cases also validate aspects of the censorship‑resistance narrative. In each instance, seizure required significant effort: detailed investigations, physical searches, cross‑border coordination, or cooperation from centralized issuers and exchanges. Bitcoin’s base layer was not altered to reverse transactions, and smart contracts were not arbitrarily modified without admin keys. Users who carefully manage operational security, avoid custodial intermediaries, and remain outside the reach of particular legal jurisdictions can reduce, though not eliminate, seizure risk. The myth lies in equating “harder to seize than a bank account” with “unseizable,” a distinction that matters greatly when narratives about Bitcoin as “digital gold” or a hedge against state overreach are deployed.

Privacy technologies and Layer‑2 solutions further complicate the picture. As more activity migrates off‑chain or into privacy‑enhancing environments, seizure may become more challenging, potentially driving a regulatory push for stronger controls at on‑ramps and off‑ramps. Market narratives, such as those where Ethereum bulls “seize on” privacy scares in competing ecosystems to highlight ETH’s institutional compatibility, reflect an ongoing struggle to define which platforms offer sustainable balances between user autonomy and compliance. For a crypto news audience, parsing these narratives requires attention not only to technical features but also to the evolving track record of seizures across different chains and asset types.

Practical Takeaways For A Crypto News Audience

Reading Headlines About Seizures

With seizure stories now a regular feature of crypto news cycles, readers benefit from approaching each headline with a few key questions. First, who controlled the seized asset at the time of the action? If the funds were held on a centralized platform—such as Alameda balances now administered by the U.S. government and transferred to Coinbase Prime for sale—then the seizure likely targeted the custodian rather than individual self‑custodied wallets. In such cases, the implications for users differ from situations where law enforcement has obtained private keys from a suspect’s home or devices, as in the Zhong case. The former underscores custodial risk; the latter highlights operational security and physical‑world vulnerabilities.

Second, is the action a freeze, a seizure, or a forfeiture? The Iranian USDT situation illustrates a freeze: tokens remain in their original addresses, but Tether’s blacklist renders them unusable while OFAC maintains them as blocked property. The Prince Group Bitcoin complaint reflects seizure and pending forfeiture: the funds are currently in U.S. custody, with the government seeking formal judicial transfer of ownership. The FTX and Alameda seizures, followed by moves to return assets to the bankruptcy estate, sit somewhere in between, with initial seizure actions giving way to complex restitution processes. Understanding which phase a case is in helps calibrate expectations about whether victims may eventually be compensated and whether the seized assets might reenter markets.

Third, what legal or geopolitical context is driving the action? Seizures tied to sanctions campaigns like Operation Economic Fury raise different issues than those tied to scam compounds or domestic fraud. In sanctions cases, the main goal may be to deny a state or terrorist group access to resources, with victim restitution taking a back seat, whereas in scam cases, authorities may actively seek to identify and compensate victims. Headlines may not always capture these nuances, but they are critical for understanding the broader significance of each seizure and its potential ripple effects for policy and markets.

Self‑Custody Versus Service‑Based Ownership

For users deciding how to hold assets, the growing body of seizure cases reinforces the central trade‑off between self‑custody and relying on service providers. Legal analysis suggests that custodial arrangements embed unpriced credit and seizure risks because users often do not fully internalize the possibility that their exchange or broker may become insolvent or targeted by law enforcement. FTX’s collapse, followed by DOJ seizures of platform‑controlled assets and a long bankruptcy process, is a vivid illustration of how these risks can materialize. At the same time, custodians provide conveniences that are difficult to replicate in self‑custody, including ease of use, customer support, institutional‑grade security, and in some cases regulatory protections and insurance.

Self‑custody reduces exposure to platform failures and broad seizures aimed at intermediaries, but it introduces its own hazards. Users must protect their private keys against loss, theft, and coercion and navigate complex interfaces for staking, DeFi participation, and tax reporting. They must also recognize that self‑custody does not immunize them from seizure in cases where law enforcement identifies them as suspects and obtains warrants to search their homes or compel disclosure of credentials. Moreover, assets like USDT remain bound by issuer‑level controls even when held in self‑custody wallets, as demonstrated by the Iranian freezes.

In practice, many sophisticated users adopt hybrid strategies, keeping a portion of their holdings in long‑term cold storage for which seizure would be difficult and another portion in custodial or semi‑custodial environments for trading and liquidity. The right balance depends on individual risk tolerance, jurisdiction, and use case. The main lesson from the seizure landscape is not that one approach is categorically safe but that each entails specific vulnerabilities that must be understood rather than ignored.

Navigating A Future Of AI‑Assisted Enforcement

Looking ahead, AI and advanced analytics are poised to make crypto seizures more efficient and more frequent. Chainalysis and similar firms already leverage machine‑learning techniques to detect patterns of illicit activity, cluster addresses, and assign risk scores that exchanges and regulators use in their compliance programs. As these tools improve, they will likely reduce the time between a hack or suspicious transaction and the identification of linked addresses, increasing the chances that funds can be frozen before they are laundered through mixers or off‑ramps. Operations like Blackout and Economic Fury, which already rely heavily on data‑driven tracing, may become faster and more granular, with AI helping to distinguish between coerced scam workers and masterminds, or between innocent users and sanctioned entities.

At the same time, AI is transforming the user‑facing side of crypto and finance. Conversational search, AI overviews, and image recognition are changing how people discover products and information, giving retailers and platforms new ways to “seize” demand. In the crypto world, user‑friendly, AI‑driven interfaces may abstract away transaction details, making it harder for individuals to understand when their actions intersect with seizure risk—for example, when sending USDT to an address that happens to be on an OFAC list. Balancing frictionless user experience with meaningful transparency about regulatory exposure will be an ongoing challenge.

For news audiences, this convergence of AI and enforcement underscores the importance of literacy in both technology and law. Stories about massive seizures will increasingly involve AI‑enabled tracing; debates about privacy and censorship‑resistance will turn on how much visibility regulators should have into on‑chain activity; and headlines about platforms “seizing opportunity” with AI will sit alongside reports of authorities seizing billions in digital assets. Understanding that these phenomena are intertwined rather than isolated is key to making sense of crypto’s trajectory.

The US, EU, UK, Brazil, and Sweden have each expanded seizure powers in 2024–2025, with cross-border coordination (Operation Cronos, Operation Destabilise) now routinely freezing hundreds of wallets across jurisdictions in a single action.

OFAC-directed freezes of Tether USDT — including the $344M Iranian-linked tranche on Tron — confirm that centralized stablecoins carry government-enforced blacklist risk at the issuer level, regardless of user custody.

Exchange-held assets are seized via subpoena and cooperative transfers to Coinbase Prime; self-custody is the only structural barrier, yet courts are developing legal theories to compel key disclosure under criminal statutes.

US authorities seized Iranian-linked USDT on Tron, Australian federal police targeted global darknet markets, and Europol cracked Irish dealer wallets — enforcement is no longer bounded by where the operator physically resides.

Chainalysis-assisted investigations traced Silk Road funds through hundreds of hops years after the original seizure, and Europol cracked a wallet believed permanently lost — blockchain forensics lag is narrowing, not zero.

US Marshals Service auctions of seized Bitcoin have historically created supply overhangs; recurring transfers of seized assets to Coinbase Prime signal structured government liquidation as a persistent market variable.

Outlook

Seizure has moved from the margins to the center of the crypto story. What began as occasional headlines about Silk Road coins has evolved into a steady drumbeat of enforcement actions: 3.36 billion dollars in Bitcoin recovered from a Georgia home, 127,271 BTC tied to forced‑labor scam compounds now in U.S. custody, more than 8 billion dollars seized from scam operations across Southeast Asia, and roughly 1 billion dollars in Iranian crypto holdings frozen or seized under Operation Economic Fury. These cases reveal both the power and the limits of state action in the face of decentralized technologies and offer a preview of how digital assets will be governed in the coming decade.

For users, the message is nuanced. Bitcoin and other cryptocurrencies do provide tools to resist arbitrary confiscation and capital controls, especially when held in well‑designed self‑custody setups. Yet they are far from unseizable. Custodial platforms remain vulnerable to legal compulsion; stablecoins can be frozen at the issuer level; and even self‑custodied assets can be taken through physical search, coercion, or court‑ordered surrender. At the same time, seizure powers have been used not only to exert geopolitical pressure but also to free trafficking victims, dismantle scam compounds, and recover funds for fraud victims. The challenge for policymakers will be to refine legal frameworks so that seizure is targeted, accountable, and accompanied by robust due process.

From an industry perspective, exchanges, custodians, and stablecoin issuers will continue to be the front line in this evolving landscape. Their decisions about when to cooperate, how quickly to freeze assets, and how transparently to communicate will shape both enforcement outcomes and user trust. AI and advanced analytics will only deepen this entanglement, making it easier to track illicit flows but also raising new questions about surveillance, error, and bias. For crypto to fulfill its promise as a more open, resilient financial system, its participants must grapple with seizure not as an aberration but as a structural reality—one that can both protect and endanger, depending on how it is wielded.

Latest Seizure news

AI chats ruled admissible in court as US judge denies legal privilege, prompting law firms to warn clients their conversations with tools like Claude can be seizedPropr unveils Hyperliquid trading platform, providing up to $100,000 funding to seize trading opportunities.Bitcoin linked to suspected steroid distribution conspiracy moved by U.S. authorities to Coinbase Prime, highlighting continued handling of seized crypto assetsArizona passes SB 1649 and SB 1042 to establish a state digital asset reserve funded by seized crypto, avoiding taxpayer costs and advancing public sector adoptionLawyer behind Arbitrum asset seizure case now targets Tether in bid to recover $344M in OFAC-frozen USDT linked to Iran’s Revolutionary GuardUS Treasury crosses $1 billion in seized Iranian crypto under Operation Economic Fury, mostly USDT on TronSources

- https://criminaldefenseattorneytampa.com/asset-seizure-asset-forfeiture/blockchain-law/

- https://www.justice.gov/usao-sdny/pr/us-attorney-announces-historic-336-billion-cryptocurrency-seizure-and-conviction

- https://www.justice.gov/opa/pr/chairman-prince-group-indicted-operating-cambodian-forced-labor-scam-compounds-engaged

- https://rareevo.io/news/us-seizes-1-billion-crypto-iran-irgc-operation-economic-fury

- https://rareevo.io/news/us-treasury-freezes-344m-usdt-iran-ofac-tether

- https://x.com/lookonchain/status/2064718059601022986

- https://www.facebook.com/CoinMarketCap/posts/latest-%EF%B8%8F-a-new-york-judge-has-paused-a-lawsuit-claiming-nearly-40000-bitcoin-wal/1420179120139477/

- https://www.chainalysis.com/blog/cryptocurrency-asset-seizure/

- https://x.com/WuBlockchain/status/2060516474599698752

- https://x.com/zachxbt/status/2063612722315681914

- https://texaslawreview.org/not-your-keys-not-your-coins-unpriced-credit-risk-in-cryptocurrency/

- https://www.chainalysis.com/blog/central-bank-of-iran-designation-ofac-update-april-2026/

- https://recoveris.io/the-344m-tether-case-what-seizing-9-billion-in-a-week-means-for-asset-recovery-lawyers/

- https://www.youtube.com/watch?v=MTJG4LQZhS8

- https://www.ebsco.com/research-starters/law/ftx-bankruptcy

- https://www.foxbusiness.com/politics/larry-kudlow-reaganesque-trumpian-optimism

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…