Explainer on “trial” in crypto, covering criminal and civil court cases (FTX, Tornado Cash, Binance), product free trials and promotions, and regulatory pilots for stablecoins and tokenization, and why they matter to investors and builders.

+16 sources across the wider coverage universe

Appeals court upholds Sam Bankman-Fried's 25-year sentence, rejecting bid for new trial in landmark FTX fraud case2026-06

Appeals court upholds Sam Bankman-Fried's 25-year sentence, rejecting bid for new trial in landmark FTX fraud case2026-06 U.S. soldier accused of $410K Polymarket insider trading gets Dec. 7 trial date in Manhattan2026-06

U.S. soldier accused of $410K Polymarket insider trading gets Dec. 7 trial date in Manhattan2026-06 Judge Tells Ex-FTX Chief Sam Bankman-Fried’s Mom She Can’t Contact Court or Seek More Time in His Bid for a New Trial2026-03

Judge Tells Ex-FTX Chief Sam Bankman-Fried’s Mom She Can’t Contact Court or Seek More Time in His Bid for a New Trial2026-03 Sam Bankman-Fried withdraws new-trial motion but still seeks to remove Judge Kaplan for 'extreme prejudice2026-04

Sam Bankman-Fried withdraws new-trial motion but still seeks to remove Judge Kaplan for 'extreme prejudice2026-04 Federal Judge denies Sam Bankman-Fried’s request for new trial, calling it a reputational rescue attempt and rejecting claims of new evidence in latest blow to former FTX CEO2026-04

Federal Judge denies Sam Bankman-Fried’s request for new trial, calling it a reputational rescue attempt and rejecting claims of new evidence in latest blow to former FTX CEO2026-04 Donald Trump found guilty in New York hush money trial.2024-05

Donald Trump found guilty in New York hush money trial.2024-05

Trials in Crypto: Courts, Products, and Regulatory Experiments

In digital assets, the word “trial” spans very different worlds: from high‑stakes courtroom battles that can decide the future of exchanges and developers, to limited‑time product offers and regulatory pilot programs that test new technologies. Understanding how these different kinds of trials work is essential context for anyone trading, building, or regulating in crypto, because they shape everything from legal risk and precedent to user acquisition strategies and market structure.

The Many Meanings of “Trial” in Crypto

The starting point for any explainer on trials is the legal meaning. In law, a trial is a formal proceeding in which parties present legal claims, evidence, and witness testimony to a judge, jury, or other adjudicator, who then decides facts and applies the law to reach a verdict. Trials are governed by detailed procedural rules and evidence standards, and they are fundamentally adversarial: each side presents its case and challenges the other’s, under the supervision of a court. In crypto, we have seen this classic notion of trial play out in marquee cases like the FTX fraud prosecution and the ongoing Tornado Cash litigation, where the outcome does not just determine one person’s guilt but also influences how the industry understands the law.

Equally important is the distinction between criminal and civil trials. Criminal trials occur when the government prosecutes an individual or entity for an alleged crime such as fraud, money laundering, or sanctions violations, and must prove guilt “beyond a reasonable doubt,” a high standard that reflects the severity of potential punishments such as imprisonment. Civil trials, by contrast, resolve disputes between private parties, including investors, customers, or shareholders, and generally apply a lower “preponderance of the evidence” standard—meaning one side’s version of events is more likely than not. In crypto, both types of trials appear: criminal cases like Sam Bankman‑Fried’s prosecution for wire fraud and money laundering, and civil or regulatory cases such as securities lawsuits against exchanges or AI‑and‑crypto adjacent suits like Elon Musk’s failed claim against OpenAI.

Outside the courtroom, trial has a very different connotation in technology and financial services: it often means a free trial or pilot access to a product. In the Software‑as‑a‑Service world, a free trial lets users experience software for a limited time or with restricted features before committing to a paid subscription, functioning as a key customer acquisition tool. SaaS marketplaces like AWS allow vendors to configure free trials that last between a set number of days—typically 7 to 90—and to define what product dimensions are available during the trial period. This logic has migrated directly into crypto, where exchanges, wallets, and gaming platforms use trials to lower the barrier for new users, for example by offering promotional “trial protection” on first trades or short‑term access to premium features.

A third important meaning of “trial” in the crypto context arises in regulatory and market infrastructure experiments. Central banks, securities regulators, and large financial institutions increasingly describe early‑stage pilots of tokenization, stablecoins, or new collateral systems as trials or “proof‑of‑concept” projects. When the SEC green‑lights a tokenized trading trial for an established exchange, or when Swiss banks collaborate on a trial of a franc‑pegged stablecoin, the word signals controlled experimentation within regulatory guardrails. In the United States, senators like Elizabeth Warren have pressed Big Tech companies such as Meta about reported stablecoin trial programs and potential rollouts, warning that experimental digital currencies could pose risks to financial stability, privacy, and competition if not adequately supervised. These regulatory trials often precede full‑scale launches, making them critical bellwethers for the future of digital assets infrastructure.

Because the same word “trial” is used for criminal prosecutions, marketing campaigns, and regulatory sandboxes, miscommunication is easy. A “trial” stablecoin operated under central bank oversight, a “trial” period on a prediction‑markets app with limited loss protection, and a criminal trial over sanctions evasion are fundamentally different creatures. Yet all three influence how crypto evolves: legal trials set precedents, product trials accelerate or test adoption, and regulatory trials determine which innovations are allowed to scale. The rest of this explainer unpacks each of these dimensions and shows how they intersect.

Appeals court upholds Sam Bankman-Fried's 25-year sentence, rejecting bid for new trial in landmark FTX fraud case

98% of FTX creditors being lined up for up to 118% of allowed USD claims never cleaned up the criminal case; BTC, SOL, and ETH balances were frozen at petition-date prices while the estate monetized Anthropic and other venture bags. The appeals loss preserves the hard line after Celsius, Voyager, and BlockFi: a bull-market recovery cannot retroactively sanitize customer-fund rehypothecation. The path left is political clemency, with SBF’s pardon push now doing more work than his “FTX was solvent” appeal theory.

Readers are not clicking to follow the crimes — they are clicking to watch courts decide whether writing privacy code, exploiting on-chain mechanics as written, or propping up an algorithmic peg constitutes a crime at all, making every verdict a live referendum on the legal definition of crypto itself.↗

How Legal Trials Work — And Why They Matter for Crypto

To understand the courtroom side of trials in crypto, it helps to walk through the basic lifecycle of a case, from investigation to verdict. In the United States, a criminal crypto case usually begins with an investigation by agencies such as the Department of Justice (DOJ), the Securities and Exchange Commission (SEC), the Commodity Futures Trading Commission (CFTC), or the Treasury Department’s Office of Foreign Assets Control (OFAC), sometimes working with foreign counterparts. Investigators may examine blockchain transactions, internal company communications, exchange records, and witness statements to determine whether conduct such as fraud, market manipulation, unregistered securities offerings, money laundering, or sanctions violations has occurred.

Once prosecutors believe they have sufficient evidence, they may seek an indictment from a grand jury in federal cases, formally charging individuals or entities. This happened, for example, when the DOJ charged Tornado Cash developer Roman Storm with conspiracy offenses tied to money laundering and sanctions violations, as well as operating an unlicensed money‑transmitting business. Similarly, the Justice Department unsealed an indictment against U.S. Army soldier Gannon Ken Van Dyke, alleging he used classified information to place profitable bets on a Polymarket prediction market related to a planned U.S. operation to capture Venezuelan leader Nicolás Maduro, charging him under the Commodity Exchange Act, wire fraud statutes, and laws governing unlawful monetary transactions.

The distinction between criminal and civil trials shapes both strategy and consequences. Criminal cases are brought by the government, and if the defendant is convicted, judges can impose imprisonment, supervised release, fines, forfeiture of assets, and other conditions. In civil cases, including many securities and consumer protection disputes tied to crypto, plaintiffs seek monetary damages, injunctions, or declaratory judgments, but losing the trial does not, by itself, send anyone to jail. The SEC’s litigation against Kraken, for instance, is a civil enforcement action; a federal judge recently rejected Kraken’s attempt to invoke the “major questions doctrine” as a defense in that case, narrowing the arguments the exchange can make as the matter proceeds. That ruling illustrates how pre‑trial motions in civil cases can set the contours for a potential trial even before a jury is seated.

Inside the courtroom, whether criminal or civil, the trial is the structured process in which each side presents its case. In criminal court, the prosecution must present evidence and call witnesses to prove each element of the charged offenses beyond a reasonable doubt, while the defense can cross‑examine those witnesses, introduce its own evidence, and argue that the government has not met its burden. Trials follow detailed rules of evidence and procedure designed to ensure fairness and reliability. In civil court, the plaintiff bears the burden of proving their claims by a preponderance of the evidence, a lower standard reflecting that the stakes, while often financially significant, are generally less severe than the loss of liberty in criminal cases. Whether in a securities‑fraud suit tied to an alleged failure to disclose crypto‑related risks, or a class action over exchange outages during market crashes, these standards guide how evidence is weighed.

Most crypto cases, like most cases generally, never make it to a full jury trial. Parties often settle or, in criminal matters, reach plea agreements. For example, the DOJ’s Fraud Section, which handles many complex financial and crypto‑related cases, reported conducting 25 trials in 2025 and convicting 31 individuals, numbers that are modest compared to the volume of investigations and charging decisions it handles each year. Corporate defendants frequently prefer to negotiate resolutions instead of risking the unpredictability of a jury and the potential collateral consequences of a conviction. This dynamic is visible in Binance’s case: rather than proceed to trial, the exchange and its founder pleaded guilty to charges including failures in anti‑money‑laundering controls, operating an unlicensed money‑transmitting business, and sanctions violations, agreeing to a multibillion‑dollar resolution that included monitorship and compliance obligations.

Sentencing is the phase that follows a criminal conviction, whether after a jury trial or a guilty plea. In crypto, the most prominent example is Sam Bankman‑Fried. The FTX founder was convicted in 2023 on multiple counts of wire fraud, securities and commodities fraud conspiracies, and money laundering conspiracy after a one‑month jury trial in New York federal court. In 2024, the judge sentenced him to 25 years in prison, followed by supervised release, and ordered him to forfeit $11 billion intended to compensate victims, reflecting the billions in customer funds prosecutors proved he misappropriated. Sentencing decisions like this send signals to the market about how severely courts will punish crypto‑related misconduct, influencing how executives, developers, and intermediaries assess risk.

Post‑trial, appellate courts and post‑conviction motions add another layer of complexity. Defendants can challenge legal rulings, the sufficiency of evidence, jury instructions, or newly discovered information. Bankman‑Fried’s legal team sought a new trial, claiming that new witnesses could offer exculpatory testimony, but the trial judge rejected those arguments as baseless and refused to grant a second trial. More recently, an appeals court has upheld his 25‑year sentence, rejecting an effort to overturn the outcome of the landmark FTX fraud case. These developments underscore that while trials are central, they are only one stage in a multi‑year legal process that can shape industry behavior long after the courtroom lights go off.

Landmark Crypto Criminal Trials

Some trials become emblematic of an entire era in crypto, crystallizing public debates about fraud, privacy, money laundering, and the responsibilities of developers and exchanges. Three sets of cases—FTX, Tornado Cash, and Binance—illustrate different dimensions of this phenomenon, while emerging matters like the Polymarket insider trading case hint at the next frontier of courtroom battles.

FTX and Sam Bankman‑Fried: Fraud at Scale

The FTX saga is by now the canonical example of a crypto criminal trial. Prosecutors alleged that Sam Bankman‑Fried, founder of FTX and trading firm Alameda Research, orchestrated multiple fraudulent schemes by misappropriating billions in customer deposits, lying to investors, and deceiving lenders. According to the Justice Department, he diverted customer funds deposited with FTX to cover Alameda’s losses, make risky investments, purchase real estate, and fund political donations, while falsely assuring users that their assets were safe and fully backed. The government also charged him with defrauding equity investors of more than $1.7 billion and lenders to Alameda of more than $1.3 billion, framing the case as one of the largest financial frauds of the modern era.

Bankman‑Fried’s trial unfolded over several weeks in late 2023. Jurors heard testimony from former FTX and Alameda insiders, including executives who had entered into cooperation agreements, as well as from customers and investors who described their reliance on FTX’s representations. Prosecutors presented internal chats, spreadsheets, and code‑level evidence showing how special privileges allegedly granted to Alameda allowed it to withdraw customer funds surreptitiously. The defense attempted to argue that Bankman‑Fried acted in good faith, was overwhelmed by rapid growth, and did not intend to defraud anyone, but the jury ultimately convicted him on all seven counts, including wire fraud, conspiracies to commit wire, securities, and commodities fraud, and money laundering conspiracy.

Sentencing cemented the trial’s symbolic weight. The court imposed a 25‑year prison sentence, below the theoretical maximum but still severe, along with three years of supervised release and an $11 billion forfeiture order intended for victim restitution. In his unsuccessful bid for a new trial, Bankman‑Fried argued that new witnesses could offer exculpatory testimony, but the judge dismissed those claims as lacking merit and characterized the attempt as an effort to rehabilitate his reputation rather than a genuine presentation of newly discovered evidence. An appeals court’s decision to uphold his sentence signals judicial willingness to treat crypto fraud on par with traditional financial crimes, undermining narratives that digital assets exist in a grey area.

Beyond the dramatic courtroom scenes, the FTX trial has enduring doctrinal effects. It illustrates that existing fraud and money‑laundering statutes are flexible enough to cover complex crypto structures without new, crypto‑specific laws, and that judges and juries are prepared to work through technically dense evidence such as exchange matching engine behavior and on‑chain transaction flows. For builders, it underscores that using customer assets without consent, even in highly intermediated or algorithmically managed systems, will be treated as straightforward theft and fraud, not as a benign liquidity practice. For regulators and legislators, the case bolsters arguments that more explicit customer‑asset protections and segregation rules are necessary in the exchange sector.

Tornado Cash and Roman Storm: Privacy, Sanctions, and Developer Liability

If FTX is the archetypal exchange fraud case, the Tornado Cash litigation is the defining trial over privacy tools and developer liability. Tornado Cash is a virtual currency mixer, a protocol designed to break on‑chain links between sending and receiving addresses to enhance financial privacy. According to the U.S. Treasury, the service was used to launder more than $7 billion worth of virtual currency since its launch in 2019, including funds tied to North Korean hacking groups and other illicit actors. In response, the Treasury’s Office of Foreign Assets Control sanctioned Tornado Cash in 2022, effectively prohibiting U.S. persons from using the protocol and blocking property interests in the mixer that are subject to U.S. jurisdiction. That move sparked intense controversy about whether sanctioning open‑source software infrastructure is consistent with U.S. law and constitutional protections.

In 2023, the DOJ indicted Tornado Cash co‑founder Roman Storm and his colleague Roman Semenov on charges including conspiracy to commit money laundering, conspiracy to violate the International Emergency Economic Powers Act (IEEPA) by helping sanctioned entities, and operating an unlicensed money‑transmitting business. Prosecutors argued that the founders actively promoted the mixer to criminal users, failed to implement adequate controls, and thus bore responsibility for facilitating billions in illicit transactions. Critics countered that Tornado Cash’s smart contracts were immutable and that holding developers criminally liable for how others use autonomous code would chill innovation and undermine civil liberties.

Storm’s trial began in July 2025 in the Southern District of New York before Judge Katherine Polk Failla. After weeks of testimony and expert evidence about how the protocol functioned and what the defendants knew, the jury returned a mixed verdict in August 2025. It convicted Storm of conspiracy to operate an unlicensed money‑transmitting business under 18 U.S.C. § 1960(b)(1)(C), but deadlocked on the counts alleging conspiracy to violate IEEPA sanctions and conspiracy to commit money laundering, leading the court to declare a partial mistrial on those charges. The conviction means that even open‑source developers can be found guilty if a jury concludes that they operated or conspired to operate an unlicensed money‑transmitting business, though the unresolved sanctions and laundering questions leave significant legal uncertainty.

The story did not end there. In March 2026, federal prosecutors informed the court that they intend to retry Storm on the two hung counts: conspiracy to commit money laundering under 18 U.S.C. § 1956 and conspiracy to violate IEEPA sanctions under 50 U.S.C. § 1705. They suggested an October 2026 retrial date and estimated another three‑week proceeding. Meanwhile, Storm still faces sentencing on the § 1960 conviction, which carries a statutory maximum of five years in prison and fines up to $250,000. Observers expect Storm’s defense team to pursue post‑trial motions and appeals, raising fundamental questions about how criminal statutes should apply to open‑source software development, privacy‑enhancing technologies, and decentralized protocols. As such, U.S. v. Storm is poised to remain a central reference point in debates over financial privacy, censorship resistance, and the boundaries of developer liability in crypto.

Binance: Plea Deal Instead of Full Trial

Binance’s legal saga shows how the threat of trial can drive negotiated resolutions even in extremely large and complex cases. In late 2023, the U.S. Department of Justice announced that Binance and its founder had pleaded guilty to federal charges, admitting that the exchange had engaged in anti‑money‑laundering failures, operated as an unlicensed money‑transmitting business, and violated U.S. sanctions laws. The case centered on allegations that Binance allowed high‑risk users to trade without adequate know‑your‑customer and AML controls, permitted customers in sanctioned jurisdictions to transact, and failed to file required suspicious activity reports, among other compliance lapses.

The resolution was vast in scale. Binance agreed to pay more than $4 billion in penalties as part of a global settlement that included the DOJ, the Treasury Department, and the Commodity Futures Trading Commission. It also agreed to submit to an independent compliance monitor and adopt significant remedial measures to bring its operations in line with U.S. expectations. Crucially, these guilty pleas and the associated corporate resolution avoided a full jury trial, which would likely have exposed internal communications and decision‑making to public scrutiny and created the risk of even more damaging findings.

For the broader crypto ecosystem, the Binance case underscores that even if many disputes are resolved through settlements, the legal standards that would apply at trial still shape outcomes. Prosecutors had to be confident they could prove their charges beyond a reasonable doubt before securing a guilty plea, and the resulting compliance obligations effectively function as court‑enforced conditions similar to those that might be imposed after a conviction. The case also illustrates regulators’ willingness to treat major centralized exchanges as systemically significant infrastructure whose AML and sanctions controls must match those in traditional finance.

Prediction Markets and Insider Trading: The Polymarket Soldier Case

As prediction markets gain traction in crypto, they are drawing the attention of regulators tasked with policing insider trading and misuse of confidential information. In an indictment unsealed by the DOJ, U.S. Army soldier Gannon Ken Van Dyke is accused of using classified government information about a planned U.S. operation to capture Venezuelan leader Nicolás Maduro to place high‑stakes bets on Polymarket, a decentralized prediction market platform. Prosecutors allege that on or about December 26, 2025, Van Dyke created and funded a Polymarket account and began trading on markets linked to Maduro‑ and Venezuela‑related events, eventually profiting more than $400,000 by wagering on the timing of the operation based on sensitive information he accessed through his military role.

The charges include three counts of violating the Commodity Exchange Act—each carrying a maximum sentence of 10 years in prison—one count of wire fraud, with a maximum of 20 years, and one count of making an unlawful monetary transaction, with a maximum of 10 years. These charges reflect the government’s position that prediction‑market contracts fall under commodities law and that trading on them using nonpublic government information constitutes commodities fraud, much as trading equities on insider information would violate securities laws. Van Dyke is set to appear before a magistrate judge in the Eastern District of North Carolina, and a separate report from the crypto press notes that he has been assigned a trial date in Manhattan federal court, underscoring the case’s high profile.

For crypto users, the Polymarket case is a stark reminder that on‑chain markets do not exist outside traditional insider trading norms. Even if the instruments are event‑based contracts rather than listed securities, prosecutors can invoke broad anti‑fraud statutes to pursue misconduct. For builders of prediction markets, it raises questions about how to monitor for and deter misuse of the platform while preserving decentralization and user privacy—a tension that will likely resurface in future trials.

Transnational Money Laundering Networks

Crypto trials also intersect with broader transnational financial crime. Law enforcement in Asia and the United States has increasingly focused on networks that launder proceeds from fraud, gambling, and other illicit activity through digital assets. One notable example involves Li Xiong, described as a former leader at a Cambodian financial conglomerate accused of laundering money for criminal organizations, who was extradited from Cambodia to China to stand trial. A related news report indicates that another figure, Chen Zhi, had previously seen 127,000 bitcoins seized by the U.S. government, highlighting the massive scale of assets at stake.

Cases like these may not always hinge on the kind of detailed blockchain analysis seen in Tornado Cash or FTX, but they still implicate crypto because launderers increasingly use digital assets as part of their toolkit. Trials of alleged network leaders help clarify how courts view the role of payment processors, over‑the‑counter desks, and fintech platforms that operate in the grey area between regulated finance and informal money‑moving. For centralized platforms and OTC brokers, the message is familiar: AML controls, sanctions screening, and robust customer due diligence are not optional, and failure to implement them can lead not only to administrative penalties but to criminal trials and extradition.

U.S. soldier accused of $410K Polymarket insider trading gets Dec. 7 trial date in Manhattan

Gannon Ken Van Dyke, the Army soldier accused of using classified intel on January’s Maduro operation to trade on Polymarket, is tentatively set for trial on Dec. 7 in Manhattan. Prosecutors say he turned roughly $33K in Venezuela-related bets into about $410K, making the case the first U.S. insider trading action centered on prediction markets. His defense is also expected to seek dismissal, so the next real fight is whether old commodities and fraud law cleanly covers onchain event-contract trading.

- 01Tornado Cash developer prosecutions↗

The parallel trials of Pertsev in the Netherlands and Roman Storm in the US forced a single urgent question onto readers: does authoring open-source privacy software make you legally responsible for every transaction it later routes?

- 02Code-is-law vs criminal liability↗

The Eisenberg Mango Markets case and the Peraire-Bueno MEV exploit trial both centered on defendants who argued they followed the rules the code set — readers engaged because the verdict would determine whether that defense holds in a US courtroom.

- 03Crypto fraud executive accountability↗

Back-to-back trials of SBF, Do Kwon, and Eisenberg gave readers a running scoreboard on whether the architects of the 2022 collapse cycle would actually face prison time.

- 04Insider cooperation and hidden backstops↗

Whistleblower testimony revealing Jump Trading's role in propping up UST and Gary Wang's cooperation in the FTX case pulled readers in because they exposed the off-chain mechanics that made on-chain collapses possible.

- 05Institutional protocol testnet pilots

Babylon's Bitcoin staking testnet, the ABN AMRO and 21X tokenized-asset Polygon trade, and Japan's Project Pax stablecoin trial represented the other meaning of 'trial' — real-money institutional experiments that signal where regulated capital is actually testing crypto rails.

- 06Regulatory forum and jury-right precedents↗

The Supreme Court's ruling that SEC defendants are entitled to a jury trial rather than in-house tribunals, alongside the Ripple pre-trial motion, showed readers that the procedural battleground matters as much as the substantive charges.

Civil, Regulatory, and Corporate Trials Shaping Crypto

Not every trial in crypto is a government‑led criminal prosecution. Civil and regulatory cases can be equally important in shaping how digital asset markets operate, particularly when they clarify the boundaries of securities law, corporate governance duties, or disclosure obligations.

SEC and Exchange Litigation: Kraken, Binance, and Beyond

The SEC has brought a series of high‑profile enforcement actions against centralized exchanges and trading platforms, many of which could culminate in civil trials if not settled. One example is the SEC’s case against Kraken, in which the agency alleges that the exchange operated as an unregistered securities platform and engaged in unlawful offerings. In a recent procedural ruling, a federal judge granted partial victories to both sides: while allowing some of Kraken’s arguments to proceed, the court rejected its attempt to invoke the “major questions doctrine,” a legal theory that suggests agencies may not decide questions of vast economic or political significance without clear congressional authorization. By striking this defense, the court narrowed Kraken’s ability to argue that the SEC is overstepping its mandate, potentially shaping the narrative that will play out if the case goes to trial.

The Binance civil suits that run alongside its criminal resolution similarly illustrate how regulatory trials can shear away layers of defense and require exchanges to defend their token listings, staking services, and marketing under existing securities frameworks. Even if these cases settle before trial, pre‑trial motions and evidentiary rulings create precedents that other courts and litigants can cite in future disputes. For market participants, tracking these developments is crucial, because they inform what kinds of tokens and products may be deemed securities, what disclosures are required, and how business models may need to adapt to survive regulatory scrutiny.

Securities, AI, and Crypto: Lessons from the Musk–OpenAI Trial

The trial between Elon Musk and OpenAI, although centered on AI rather than tokens, offers relevant lessons for crypto about how courts may treat early‑stage corporate and nonprofit promises in fast‑moving technology sectors. Musk’s $134 billion lawsuit claimed that OpenAI and CEO Sam Altman had strayed from the company’s founding mission and breached obligations to operate as an open, nonprofit entity. A jury ultimately ruled that Musk sued too late, leaving Altman, OpenAI, and Microsoft free of liability and underscoring the weight courts place on statutes of limitation and contractual formalities in high‑growth tech ventures.

In the crypto context, where founders often make expansive claims in whitepapers, tweets, and community calls, the Musk–OpenAI outcome suggests that courts will scrutinize the legal status of these statements and the timing of investor challenges. Token projects that transition from nonprofit foundations to for‑profit entities, or that pivot their governance structures, may face similar arguments about mission drift and fiduciary duties. Trials in these disputes could clarify how seriously judges take informal mission statements and community expectations versus formal corporate charters and shareholder agreements.

Investor and Shareholder Trials Tied to Crypto Exposure

Beyond direct suits against token issuers and exchanges, investor and shareholder litigation increasingly targets traditional companies whose fortunes are tied to crypto. The U.S. Supreme Court’s decision to allow a securities lawsuit against Nvidia to proceed toward trial, for example, focuses on whether the chipmaker adequately disclosed how much of its revenue depended on demand from crypto miners. Such trials could clarify how public companies must characterize crypto‑related revenue streams, customer concentration, and regulatory risks, influencing disclosure standards across industries that serve the digital asset space.

For asset managers and corporate boards, these cases underscore that a trial need not be “about crypto” in a narrow sense to have major implications. Misstating or omitting material information about crypto exposures—be it mining customers, tokenized products, or stablecoin integrations—can give rise to classic securities‑fraud claims. Trials in these matters become forums in which courts and juries assess how understandable and foreseeable crypto risks were to management and whether investors were misled.

State‑Level Regulation and Evolving Trial Practice

Crypto litigation is not confined to federal courts. State attorneys general, financial regulators, and private plaintiffs are increasingly active in bringing actions under state blue‑sky laws, money‑transmitter statutes, and consumer protection rules. Legal scholars have noted that many states recognize the need for specialized legislation to govern digital assets, aiming to protect consumers and provide clearer guidance to local businesses. As these statutes proliferate, state‑court trials will test their scope, including whether particular crypto‑lending arrangements qualify as unregistered securities, or whether certain NFT offerings constitute deceptive trade practices.

Trial practice in this environment must adapt. Lawyers on both sides must educate judges and juries about on‑chain mechanics, tokenomics, and DeFi protocols while grounding their arguments in state statutory language and precedent. The resulting trial records, appellate opinions, and jury verdicts will gradually build a patchwork of state‑level crypto jurisprudence. For companies operating nationally, that patchwork can create compliance complexity, as different jurisdictions may reach different conclusions about similar products, at least until federal legislation or Supreme Court decisions harmonize standards.

“Trial” as a Product Strategy in Crypto and Fintech

Moving outside the courtroom, crypto and adjacent industries have embraced trials in the more familiar marketing sense: time‑limited access to products, or risk‑limited opportunities to test features, meant to convert curious users into long‑term customers.

SaaS Free Trials: Template for Web3 Growth

In the SaaS world, a free trial is a widely used acquisition model that lets potential customers use a service temporarily, often with limited functionality, before entering a paid subscription. Trials reduce friction by allowing users to experience the product and its value proposition firsthand without initial financial commitment. Vendors typically define the length of the trial and any usage caps or feature restrictions in advance, balancing the desire to showcase capabilities against the risk of giving away too much.

Infrastructure providers like AWS formalize this process. In AWS Marketplace, sellers can create a single SaaS free trial offer per public product, specifying a duration between 7 and 90 days and configuring which product dimensions are available during the trial. The marketplace guides sellers through selecting their product, setting trial length, reviewing service agreements, and verifying offer details before launch. While AWS itself is not a crypto product, many blockchain analytics, custody, and compliance tools are delivered as SaaS and leverage identical trial mechanics. For Web3 startups, mimicking this pattern—bounded trials with clear terms, automated conversion paths, and transparent EULAs—can be an effective way to on‑board developers, enterprises, and power users.

Exchange and Wallet Promotions: Trial Protections and Weekend Passes

Crypto‑native platforms extend the trial concept into financial risk‑sharing. Binance Wallet, for example, has run multiple phases of a Prediction Markets Trial Protection Campaign, in which new users can receive limited loss coverage on their first eligible prediction trade. In a recent phase, the campaign offered up to 5 USDT in loss protection to the first 15,000 registered users whose initial prediction‑market order met specified criteria, including being placed and resolved within defined dates and held to market resolution. If the trade lost money under those conditions, Binance would reimburse the loss up to the 5 USDT cap, effectively underwriting a small trial bet.

The detailed terms matter. Users had to complete campaign registration during the promotion window, enter eligible prediction markets via the Binance Exchange or wallet interface, and ensure their positions remained open until markets settled before the deadline. Funding could come from spot or funding account balances or, via a DApp interface, from USDT deposits on BNB Smart Chain. These constraints illustrate how “trial protection” is carefully structured to limit the platform’s liability while still giving users a feeling of reduced risk. For regulators, such promotions raise questions about whether they might encourage excessive speculation or obscure the true risk profile of prediction markets, particularly when offered in jurisdictions where derivatives regulation is evolving.

Other crypto apps have experimented with more social forms of trials. The Base app, described as an “everything app” for on‑chain trading, earning, and exploring, provides mobile‑friendly access to a broad ecosystem of crypto activities. Reports from the crypto press describe weekend trial programs in which existing Base users can give friends time‑bounded access or special fee terms, effectively transforming loyal users into distribution channels. Similar patterns appear in the wider fintech world, where telecom provider Visible has offered short free‑trial windows, and where Web3‑adjacent gaming platforms provide trial access to premium features to boost user conversion.

Telecoms, Gaming, and SportFi: Trials Driving Peripheral Crypto Adoption

Trials are also central to the growth of SportFi and blockchain‑based gaming. Titles like Trial Xtreme Freedom have reached millions of downloads, but questions about long‑term retention linger, prompting developers to experiment with trial‑based content drops and incentives to keep players engaged. In the fan‑token sector, Chiliz and its partners have framed upgrades to fan‑engagement mechanisms as entering a “trial phase” of new products like Fan Token Play, where a limited number of clubs and tokens test features before broader rollout. Early SportFi trials, such as the phase in which Persija Jakarta’s fan‑token sale sold out quickly and led to the burning of millions of CHZ tokens, hint at the demand these experimental features can unlock—but also highlight the design challenges in sustaining engagement after novelty wears off.

From a crypto perspective, these gaming and SportFi trials serve two purposes. First, they allow teams to fine‑tune token economics, reward structures, and governance mechanisms in a relatively controlled environment, learning how real users behave with small stakes before scaling up. Second, they function as on‑ramps, introducing fans and players who may not identify as “crypto users” to wallets, tokens, and on‑chain interactions. The trial framing lowers psychological barriers while preserving the option for users to opt out if they find the experience confusing or unappealing.

Risks and Responsibilities in Product “Trials”

While product trials can drive growth, they carry risks if misunderstood. Users may conflate a trial with a guarantee, assuming that a trial‑protected trade is “safe” or that trial access to a platform signifies regulatory approval. In reality, a promotion offering up to 5 USDT in loss coverage on a first prediction‑market trade does little to protect against larger future losses, and a free‑trial wallet or exchange account still exposes users to market volatility, smart‑contract risk, and counterparty risk. Platforms therefore bear a responsibility to communicate trial terms clearly, avoid overstating protections, and implement safeguards against irresponsible trading.

There is also a reputational dimension. If a trial promotion is perceived as a gimmick or as targeting vulnerable users—such as inexperienced retail traders in volatile markets—it may invite regulatory scrutiny or backlash. Conversely, well‑designed trials that emphasize education, limit financial exposure, and integrate strong disclosures can help regulators see crypto platforms as responsible innovators. For users, the key is to treat trials as opportunities to learn and experiment with small stakes, not as invitations to leap into complex products without understanding the risks.

Judge Tells Ex-FTX Chief Sam Bankman-Fried’s Mom She Can’t Contact Court or Seek More Time in His Bid for a New Trial

Phew, that serves him right.

Sam Bankman-Fried convicted on all seven federal counts in New York

SBF sentenced to 25 years; new-trial bid subsequently denied

Alexey Pertsev convicted in Netherlands for Tornado Cash money laundering

- 2024-05regulatory

Donald Trump found guilty on all 34 counts in New York hush money trial

- 2024-07regulatory

Terraform Labs and Do Kwon found liable for fraud in SEC civil trial

- 2024-12regulatory

Avi Eisenberg convicted of commodities fraud and market manipulation over Mango Markets exploit

- 2025-05regulatory

Peraire-Bueno MEV brothers trial begins in New York on $25M exploit charges

Roman Storm Tornado Cash trial proceeds after DOJ reaffirms charges and judge grants partial pre-trial privacy-argument win

Regulatory and Central Bank Trials: Sandboxes for Tokenized Finance

Beyond corporate marketing, governments and financial institutions increasingly use trials to test new forms of digital money and market infrastructure in controlled settings.

Tokenized Securities and Exchange Infrastructure

One of the most significant directions for regulatory trials is the tokenization of traditional securities and the platforms that trade them. When the SEC authorizes a tokenized trading trial on a major exchange like Nasdaq, it is effectively carving out space for experimentation with blockchain‑based settlement, fractionalized ownership, or 24/7 markets while maintaining tight oversight. These trials often restrict participation to institutional investors, limit asset types, or operate in parallel with existing systems to avoid systemic risk.

Such experiments can answer technical and legal questions that are difficult to resolve in abstract policy debates. How does on‑chain settlement interact with existing clearing and custody rules? Can smart‑contract‑based transfer restrictions enforce securities‑law requirements more effectively than legacy systems? Trials provide data on latency, resilience, error handling, and regulatory reporting, guiding both future rulemaking and commercial adoption. For crypto‑native builders, these initiatives are a signal that major incumbents are taking tokenization seriously—but also that their expectations around auditability, compliance, and interoperability are high.

Stablecoin Trials: Meta, Swiss Banks, and CBDC Experiments

Stablecoins and central bank digital currencies are another focus of regulatory trials. Reports have indicated that Swiss banks are collaborating on a trial of a franc‑pegged stablecoin, exploring how tokenized bank money could function in domestic payments and cross‑border transactions. In parallel, experiments with wholesale CBDCs and tokenized deposits are underway in multiple jurisdictions, often within regulatory sandboxes where participants must meet strict compliance and risk‑management criteria.

In the United States, attention has focused on tech giants’ stablecoin ambitions. Senator Elizabeth Warren has pressed Meta over reports of a stablecoin trial and potential 2026 rollout plans, expressing concern that the company’s entry into digital currencies might threaten financial stability, undermine privacy, and distort competition in payments markets. She has questioned whether Meta can be trusted to manage a global stablecoin responsibly given its past controversies and has urged regulators to scrutinize any trial programs carefully. For the crypto industry, these debates highlight a key tension: stablecoin trials by highly centralized platforms may accelerate adoption but also raise systemic risk and regulatory backlash if not tightly controlled.

Collateral, Bonds, and DeFi Tooling

Beyond retail payments, regulators and financial institutions are trialing tokenization in the realm of collateral management and sovereign debt. A proof‑of‑concept trial using Japanese government bonds (JGBs) as digital collateral, for example, explores how tokenized securities could be pledged, rehypothecated, and settled more efficiently in wholesale markets. Such trials are highly relevant to DeFi because they test whether real‑world assets like bonds can be integrated into programmable finance frameworks without sacrificing legal certainty or introducing hidden leverage.

These experiments often involve consortia of banks, exchanges, and fintech providers, and they typically run in parallel to legacy collateral systems. The goal is to see whether tokenized collateral can reduce operational risk, speed up margin calls, or enable new types of automated risk management, while still satisfying regulatory capital, liquidity, and reporting requirements. For DeFi protocols that already use on‑chain collateralization, the outcome of these trials may determine how easily they can plug into traditional financial flows.

AI and Infrastructure Trials Linked to Mining and Environment

Not all regulatory trials are about money itself; some focus on the infrastructure and environmental footprint of digital technologies, including crypto mining. For instance, proposals like the Mining Council of Australia’s request for funding a $13 million AI trial for environmental approvals—while not solely about crypto—reflect the increasing role of AI and data analytics in assessing the ecological impact of resource‑intensive processes. Biodiversity experts warn that such trials must not bypass careful ecological review, emphasizing that unchecked deployment of AI tools could lead to irreversible damage.

In regions where crypto mining consumes significant energy and affects local ecosystems, similar tensions arise. Trials of new monitoring systems, renewable‑energy integration, or AI‑driven optimization of mining operations could help balance innovation and environmental stewardship, but they must be designed with transparency and stakeholder input. If these experiments lead to better data on energy use and emissions, they could inform both environmental regulation and industry best practices, influencing how courts and regulators evaluate mining operations in future disputes.

Following and Interpreting Crypto Trials

For traders, builders, and policymakers, understanding how to follow a trial—legal, product‑based, or regulatory—is increasingly a core skill. Trials generate information and precedent that can materially affect token prices, business models, and compliance strategies.

Reading Indictments, Sanctions Orders, and Complaints

Legal trials begin with formal documents that set out the allegations. In criminal cases, indictments detail the statutes allegedly violated, the factual basis for the charges, and sometimes forfeiture claims. For example, the indictment against Tornado Cash’s Roman Storm and Roman Semenov describes how the government believes the founders marketed the protocol, handled compliance, and knowingly facilitated illicit transactions. In the Polymarket soldier case, the indictment specifies how Van Dyke allegedly accessed classified information, when he opened his trading account, and what kinds of trades he placed, linking those facts to Commodity Exchange Act and wire‑fraud provisions.

Sanctions orders, like OFAC’s designation of Tornado Cash, are another key document type. The Treasury’s press release explained that the mixer had been used to launder over $7 billion in virtual currency and specified that all U.S. persons are prohibited from transacting with the sanctioned entity and must block any property interests subject to U.S. jurisdiction. Civil complaints, such as those filed by the SEC, lay out jurisdictional bases, describe allegedly unregistered securities offerings or deceptive statements, and propose remedies such as injunctions, disgorgement, and penalties. For market participants, reading these documents closely can reveal regulators’ theories of liability, the conduct they consider most egregious, and the types of activities that might trigger similar actions against other firms.

What to Watch During Trial: Evidence, Expert Testimony, and Narratives

Once a trial begins, the focus shifts from pleadings to proof. In complex crypto cases, expert testimony is often central. Technical experts might explain how a blockchain protocol functions, how mixing services obfuscate transaction flows, or how exchange systems handle customer deposits and internal transfers. Financial experts may analyze loss calculations, tracing misappropriated funds or modeling investor harm. Lawyers use this testimony to build narratives that either portray the defendant’s conduct as intentional wrongdoing or as good‑faith participation in an evolving market.

For observers, key moments include rulings on the admissibility of expert evidence, cross‑examinations that expose weaknesses in testimony, and the judge’s instructions to the jury on how to interpret legal standards. In high‑profile cases like FTX, trial coverage has highlighted the emotional impact of insider testimony, where former colleagues testify against founders, as well as the power of documentary evidence such as internal messages and code commits. These details can influence public perception of the industry and may affect regulatory appetites and investor sentiment even before verdicts are reached.

Sentencing, Forfeiture, and Compliance Obligations

Verdicts are not the end; sentencing and remedial orders often have the greatest long‑term impact on the ecosystem. In Bankman‑Fried’s case, the 25‑year sentence and $11 billion forfeiture order send a clear message that misusing customer funds at scale will draw severe punishment. Forfeiture orders can also drive substantial asset recovery efforts, including on‑chain tracing and seizure of tokens or fiat balances, influencing liquidity and market dynamics. Similarly, when corporate defendants like Binance resolve cases through guilty pleas, the resulting monitorships, compliance undertakings, and reporting obligations reshape how those platforms operate day‑to‑day.

In transnational money‑laundering cases, asset seizures such as the confiscation of 127,000 bitcoins from alleged network leaders can have symbolic and practical significance. They demonstrate that law enforcement can in fact seize large digital‑asset holdings and may alter the risk calculus of criminal organizations that previously viewed crypto as beyond the reach of authorities. For regulated institutions, these outcomes underscore the importance of maintaining robust AML and sanctions programs and cooperating with investigations when suspicious activity is detected.

Appeals, Retrials, and Post‑Trial Motions

Finally, the appellate and post‑trial phase can be as consequential as the trial itself. Defendants may file motions for a new trial, as Sam Bankman‑Fried did, arguing that newly discovered evidence or legal errors justify re‑litigation, though judges rarely grant such requests and rejected his as unfounded. Appeals can challenge the interpretation of statutes, the constitutionality of sanctions, or the application of money‑transmission laws to decentralized protocols. The outcome of these appeals often affects not just the parties but the entire industry, as appellate opinions become binding precedent within their jurisdictions.

Retrials, like the one prosecutors are seeking against Roman Storm on the hung money‑laundering and sanctions counts, highlight the persistence of enforcement efforts. A mixed verdict and partial mistrial do not necessarily mark the end of a case; the government can choose to try again, armed with insights from the first trial about which arguments resonated with jurors. For the crypto community, it means that legal questions about privacy tools, developer liability, and the reach of sanctions regimes may be revisited multiple times before a durable consensus emerges.

US and Dutch prosecutors are actively testing whether financial crime statutes extend to privacy-tool authors, MEV searchers, and algorithmic stablecoin designers — verdicts in Storm, Pertsev, and Peraire-Bueno cases will directly set enforceable precedents.

- Smart-contractMedium

The Peraire-Bueno MEV case established that exploiting validator-level transaction ordering as written — without breaking any contract — may still constitute conspiracy and wire fraud if a court finds the intent was to deceive counterparties.

- CentralizationHigh

The Terraform trial revealed that Jump Trading's covert UST support constituted a hidden centralized backstop inside an ostensibly algorithmic system, a structural risk invisible to on-chain analysis alone.

The Mango Markets manipulation verdict and Terraform fraud liability finding signal that oracle manipulation and coordinated depeg attacks now carry clear civil and criminal exposure regardless of whether they used smart contracts rather than traditional instruments.

- LiquidityLow

Institutional testnet pilots — ABN AMRO on Polygon, Japan's Project Pax via SWIFT API, Babylon's BTC staking — remain in controlled trial phases, limiting near-term contagion risk from an institutional on-chain failure.

Outlook

Across courts, trading platforms, and regulatory sandboxes, trials in all their forms are now a defining feature of the crypto landscape. Criminal and civil trials are articulating how existing fraud, securities, money‑laundering, and sanctions laws apply to exchanges, developers, and prediction markets. Product trials—from free‑trial wallets to risk‑capped prediction‑market promotions—are testing how far platforms can go in lowering user friction without crossing regulatory lines or misleading customers. Regulatory and central‑bank trials, meanwhile, are exploring the feasibility of tokenized securities, stablecoins, and digital‑collateral systems that could eventually reshape financial market plumbing.

For crypto investors and builders, the implication is clear: legal literacy and regulatory awareness are no longer optional. Following major trials like FTX, Tornado Cash, Binance’s resolutions, and emerging cases such as the Polymarket insider‑trading matter provides insight into how courts think about on‑chain behavior and what types of conduct they consider criminal or deceptive. Monitoring product and regulatory trials reveals how user‑experience innovations and tokenization experiments are likely to be received by authorities and the public.

Over the next few years, more landmark trials are likely, including class‑action suits over disclosure of crypto exposures by public companies, enforcement actions against DeFi protocols, and cross‑border cases involving stablecoins and money‑laundering networks. At the same time, we will see more structured pilots of tokenized assets, central‑bank money, and AI‑enhanced infrastructure. Navigating this environment requires treating every trial—whether in a courtroom, a code repository, or a central bank’s sandbox—as a source of information about where digital finance is heading and what constraints will govern its evolution.

Latest Trial news

Appeals court upholds Sam Bankman-Fried's 25-year sentence, rejecting bid for new trial in landmark FTX fraud caseU.S. soldier accused of $410K Polymarket insider trading gets Dec. 7 trial date in ManhattanJudge Tells Ex-FTX Chief Sam Bankman-Fried’s Mom She Can’t Contact Court or Seek More Time in His Bid for a New TrialSam Bankman-Fried withdraws new-trial motion but still seeks to remove Judge Kaplan for 'extreme prejudiceFederal Judge denies Sam Bankman-Fried’s request for new trial, calling it a reputational rescue attempt and rejecting claims of new evidence in latest blow to former FTX CEO Justin Sun vs. TrueCoin (TUSD) and where $450M went

Justin Sun vs. TrueCoin (TUSD) and where $450M wentSources

- https://www.law.cornell.edu/wex/trial

- https://docs.aws.amazon.com/marketplace/latest/userguide/saas-free-trials.html

- https://search.proquest.com/openview/ae68aebd51886ca17db16bee4d6a4641/1?pq-origsite=gscholar&cbl=16721

- https://abcnews.com/US/judge-denies-new-trial-sam-bankman-fried-after/story?id=132471994

- https://www.skadden.com/-/media/files/publications/2023/09/court-victory-for-treasury-and-indictment/sealed-indictment.pdf?rev=c45a6e6167704e32b15d3ed338d5d744&hash=7A8986F843AAC54C22D122EB21782F6D

- https://www.binance.com/en/support/announcement/detail/db2abfa716de40cd930400ad418583a4

- https://x.com/CoinDesk/status/2052788391788318787

- https://www.justice.gov/opa/pr/us-soldier-charged-using-classified-information-profit-prediction-market-bets

- https://home.treasury.gov/news/press-releases/jy0916

- https://www.facebook.com/thejapantimes/posts/li-xiong-a-former-leader-at-a-cambodian-financial-conglomerate-accused-of-launde/1353448646820720/

- https://www.lawhelp.org/resource/the-differences-between-criminal-court-and-ci

- https://www.justice.gov/archives/opa/pr/binance-and-ceo-plead-guilty-federal-charges-4b-resolution

- https://www.defieducationfund.org/u-s-v-storm-2026-update/

- https://billingplatform.com/blog/what-is-a-free-trial

- https://play.google.com/store/apps/details?id=org.toshi&hl=en_US

- https://www.bankingdive.com/news/judge-tosses-krakens-major-questions-doctrines-defense/738368/

- https://www.wiley.law/alert-2025-DOJ-Fraud-Section-Year-in-Review

- https://www.justice.gov/archives/opa/pr/samuel-bankman-fried-sentenced-25-years-his-orchestration-multiple-fraudulent-schemes

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

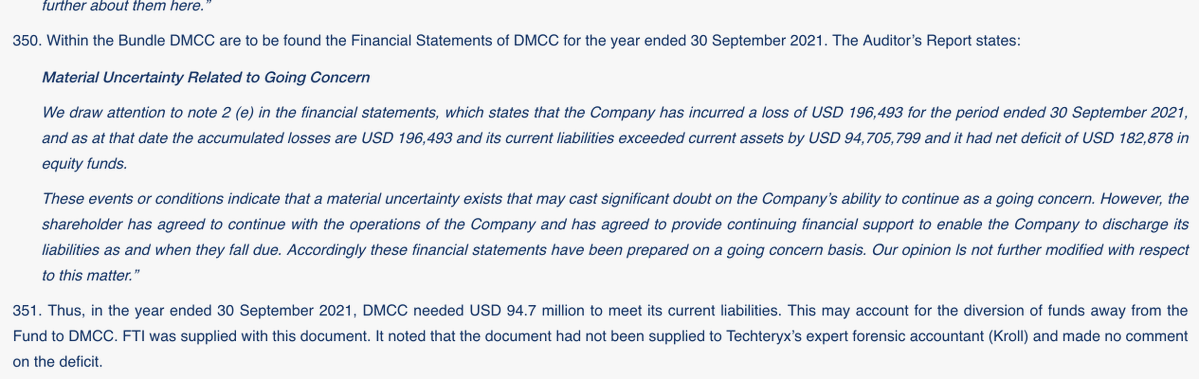

Loading notes…