Explains what “license” means in crypto, covering regulatory approvals (MiCA, VARA, MAS, HK stablecoin regime, US MTLs), software and content licenses, and how licensing shapes launches, payments, stablecoins and competition across major jurisdictions.

+24 sources across the wider coverage universe

Ripple to secure Australian Financial Services License, expanding payments offering across APAC2026-03

Ripple to secure Australian Financial Services License, expanding payments offering across APAC2026-03 Ripple receives full EU Electronic Money Institution License in Luxembourg.2026-02

Ripple receives full EU Electronic Money Institution License in Luxembourg.2026-02 The Bank of Russia proposed a new crypto framework expanding retail and professional investor access under tiered limits, while keeping crypto barred from domestic payments and routed through licensed intermediaries, with full legislation targeted for 2026.2025-12

The Bank of Russia proposed a new crypto framework expanding retail and professional investor access under tiered limits, while keeping crypto barred from domestic payments and routed through licensed intermediaries, with full legislation targeted for 2026.2025-12 Hybrid crypto platform Byrrgis has secured an EU MiCA license ahead of its January 15 launch and opened a waitlist for early access. The regulated hub will combine CEX and DEX features, offering automated portfolio packs and advanced trading tools.2025-12

Hybrid crypto platform Byrrgis has secured an EU MiCA license ahead of its January 15 launch and opened a waitlist for early access. The regulated hub will combine CEX and DEX features, offering automated portfolio packs and advanced trading tools.2025-12- ANDRE CRONJE: "If you're asking whether or not Fantom has obtained a banking license and is launching a crypto friendly bank, the answer is yes, that is happening." 2023-04

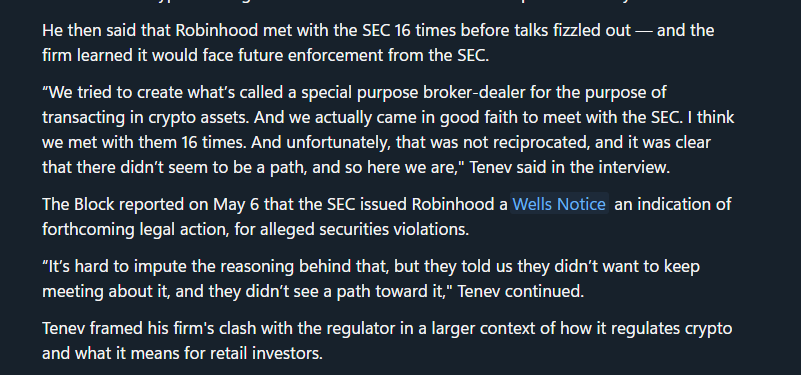

Even with all securities licenses and expertise, Robinhood faces challenges in offering Crypto compliantly.

"Robinhood has every possible securities license, TradFi securities relationship, an army of traditional securities lawyers, etc., and even THEY can't figure out how to offer crypto compliantly***even if they were to treat tokens as securities***"2024-05

Even with all securities licenses and expertise, Robinhood faces challenges in offering Crypto compliantly.

"Robinhood has every possible securities license, TradFi securities relationship, an army of traditional securities lawyers, etc., and even THEY can't figure out how to offer crypto compliantly***even if they were to treat tokens as securities***"2024-05

Licenses in Crypto: What They Are and Why They Matter

In digital asset markets, a license is formal permission to do something that would otherwise be illegal or contractually prohibited, whether that is providing crypto services to the public, issuing a stablecoin, operating a prediction market, or reusing someone else’s code. Licenses increasingly shape who can launch, trade, pay, build and innovate in crypto, and they are becoming one of the main competitive battlegrounds across jurisdictions.

What “License” Means In A Crypto Context

The term license is broader than many market participants initially assume. In a regulatory sense, a license is an authorization granted by a government or regulator that allows a firm to carry out a defined financial or commercial activity, such as exchanging crypto for fiat, issuing a stablecoin, or providing custody services to the public. In a technical or legal sense, a license is also the contractual agreement that governs how software, content, or a protocol can be used, copied, modified, or commercialized. Both dimensions are central to crypto, and both increasingly determine who can enter the market and on what terms.

In financial regulation, a license is a gatekeeper. In most jurisdictions, operating a crypto exchange, wallet, payment rail, or gambling platform without the appropriate authorization is unlawful, regardless of whether a firm is “decentralized” or uses blockchain technology. This is evident in the United States, where crypto firms must navigate a patchwork of state money transmitter licenses, and in the European Union, where the Markets in Crypto‑Assets Regulation (MiCA) now requires crypto‑asset service providers to be authorized under harmonized rules before serving EU clients. In parallel, regulators in Dubai, Hong Kong, Singapore, Brazil, Australia, and other markets have created distinct licensing regimes for virtual asset service providers and stablecoin issuers, underscoring that digital assets are no longer treated as an unregulated frontier.

At the same time, crypto is built on software, and software is governed by licenses. Open‑source licenses determine whether a DeFi protocol’s code can be forked freely or only under certain conditions. NFT and content licenses determine what buyers can actually do with the images, music, or in‑game objects they purchase. Cloud services and platforms impose end‑user license agreements (EULAs) that govern how wallets, exchanges, or even on‑chain AI agents may use underlying infrastructure. As disputes about “license violations” in DeFi, AI and gaming demonstrate, software and content licenses are increasingly intertwined with the business and governance of crypto protocols.

Understanding the different types of licenses, how they are issued, and what they allow is therefore essential for exchanges planning an EU launch under MiCA, payment firms building stablecoin rails, developers forking an automated market maker, and everyday users deciding whether a “licensed” platform is genuinely safer.

Ripple to secure Australian Financial Services License, expanding payments offering across APAC

Readers click licensing stories not for compliance mechanics but to track legitimacy arbitrage — which actors are gaining regulated access while well-resourced incumbents like Robinhood publicly admit they cannot crack the same problem.↗

Regulatory Crypto Licenses: From “Wild West” To Supervised Industry

The global policy backdrop: VASPs and financial regulation

Over the last decade, regulators have moved from treating crypto as a niche curiosity to treating it as part of the formal financial system. A key turning point was the Financial Action Task Force’s (FATF) decision to define Virtual Asset Service Providers (VASPs) and subject them to anti‑money laundering (AML) and counter‑terrorist financing rules that mirror those applied to banks and broker‑dealers. Chainalysis, summarizing FATF guidance, notes that a VASP is any business that exchanges, transfers, or custodies digital assets, or provides related financial services. This definition is intentionally technology‑neutral: a centralized exchange, an OTC desk, or a wallet operator can all be VASPs if they are “in the business” of facilitating transactions on behalf of others.

Once a firm falls into the VASP category, most jurisdictions require it to register or obtain a license, implement AML/KYC controls, monitor for suspicious activity, and comply with the so‑called “travel rule,” which demands that originator and beneficiary information accompany certain transfers. This is fundamentally a licensing issue: firms are not merely complying with abstract rules but are seeking formal authorization to operate. A license can be refused, conditioned, suspended, or revoked if the firm fails to meet prudential, conduct, or AML standards.

This shift is visible in mature financial centers. The European Union’s MiCA creates a comprehensive authorization regime for crypto‑asset service providers (CASPs), building on the VASP concept but integrating it into EU financial law. Hong Kong’s stablecoin regime requires fiat‑referenced issuers to obtain a specific license from the Hong Kong Monetary Authority (HKMA) as of August 2025. Dubai’s Virtual Assets Regulatory Authority (VARA) licenses virtual asset exchanges, custodians, and other service providers under its own rulebook. In Singapore, the Monetary Authority of Singapore (MAS) licenses “digital payment token” service providers as part of its Payment Services Act and has shown its willingness to revoke licenses in the crypto sector. Licensing thus serves as the main conduit through which general financial policy is applied to crypto.

Core categories of regulated crypto activity

Although details vary by jurisdiction, the same functional activities tend to trigger licensing requirements. The most fundamental is exchanging between crypto and fiat or between different crypto‑assets on behalf of others. Firms that run order‑book exchanges, brokerage services, or automated matching systems are usually required to obtain one or more licenses, often in categories such as “crypto‑asset service provider,” “virtual asset exchange,” or “money transmitter.” In Dubai, for example, VARA’s broker‑dealer and exchange licenses cover activities such as executing client orders and operating trading platforms.

Custody is another licensed function. Safeguarding clients’ private keys, operating omnibus wallets, or managing institutional cold storage are almost always considered regulated activities. Many frameworks treat custodians as a distinct class requiring enhanced operational resilience, segregation of assets, and independent audits. VARA, for instance, has a dedicated custody license category. Hong Kong’s stablecoin regime similarly focuses on governance and safeguarding of backing assets, which is conceptually a custody problem.

Payment and remittance activities also attract licensing. In Singapore, digital payment token services are licensed under MAS’s Payment Services Act, and firms can be designated as “major payment institutions” once they surpass certain thresholds. In the United States, transmitting money, even in crypto form, typically requires state money transmitter licenses. Cross‑border payment firms like Ripple, and fiat‑crypto payment gateways such as Alchemy Pay, therefore pursue financial services licenses that allow them to operate compliant on‑ and off‑ramps. Similarly, issuing stablecoins that function as means of payment is increasingly being regulated as a licensed activity in its own right in the EU, Hong Kong, and proposed US state frameworks.

Finally, activities that look like trading, speculation, or wagering can fall under securities, derivatives, or gambling laws, requiring specialized licenses. European authorities have treated some crypto prediction markets not as financial infrastructure but as unlicensed gambling platforms, requiring them to obtain the same authorizations as online betting companies. As crypto integrates into traditional markets, these licensing categories increasingly overlap, and a single platform may need multiple licenses to conduct its business legally.

The United States: Money Transmitter Licenses And Emerging Stablecoin Regimes

A 50‑state patchwork for crypto businesses

Unlike the EU’s MiCA framework, the United States does not have a single federal regulatory regime for digital assets that covers all crypto activities in a unified way. Instead, crypto businesses must navigate a complex mosaic of state and federal rules. At the state level, most crypto exchanges and payment platforms are treated similarly to money services businesses and must obtain money transmitter or equivalent licenses in each state where they have customers. A review by the Wharton Initiative on Financial Policy and Regulation underscores that “the United States has no federal regulatory framework for digital assets,” and that states have taken widely differing approaches, from comprehensive virtual currency statutes to minimal guidance.

In practice, this means that a company offering fiat‑to‑crypto conversions or custodial wallets might need to secure dozens of separate licenses. Each license application entails background checks on management, financial audits, compliance program reviews, and ongoing reporting obligations. Some states, such as New York, have created specialized regimes like the BitLicense, while others rely on general money transmitter laws. For crypto firms, this is a licensing marathon: expansion across the U.S. is not a single event but a state‑by‑state campaign.

Alchemy Pay’s licensing trajectory illustrates how payment‑focused crypto firms adapt to this environment. The company, which provides fiat‑crypto payment and on‑ramp services, has obtained multiple state money transmitter licenses, including a currency transmitter license in Rhode Island and a money transmitter license in Delaware. The Rhode Island license contributed to bringing Alchemy Pay’s licensed coverage to 16 states, supporting the growth of its compliant fiat‑crypto payment services and stablecoin‑powered infrastructure. The Delaware license authorizes regulated money transmission services in that state under the supervision of its banking regulator. This incremental approach is typical: as each new license is granted, the firm can serve more U.S. customers while demonstrating a growing footprint of regulatory compliance.

Delaware’s proposed stablecoin and digital asset service provider framework

One emerging development in the U.S. is the move from generic money transmitter rules toward specialized regimes for stablecoin issuers and digital asset service providers. Delaware, a major corporate domicile, has introduced legislation to establish a licensing and regulatory framework for payment stablecoin issuers and digital asset service providers operating in the state. The bill’s stated purposes include setting up a formal regime for licensing payment stablecoin issuers, adopting supervisory standards for digital asset service providers, and providing legal clarity to market participants.

Although money transmitter laws already capture many crypto activities, Delaware’s proposal recognizes that payment stablecoins occupy a distinct regulatory niche, blending characteristics of stored value, bank deposits, and securities. By creating a dedicated license for payment stablecoin issuers, Delaware aims to attract such businesses while imposing specific obligations around reserve composition, redemption rights, and risk management. A similar approach can be seen in Hong Kong’s Stablecoins Ordinance, which explicitly regulates the issuance of fiat‑referenced stablecoins as a licensed activity. For crypto firms, the emergence of specialized stablecoin licensing regimes suggests that future regulatory mapping will be more granular than the early “money transmitter” paradigms.

Federal and sectoral licensing trends

Overlaying the state landscape is a patchwork of federal oversight from agencies such as the Securities and Exchange Commission (SEC), the Commodity Futures Trading Commission (CFTC), and banking regulators, which can require securities, derivatives, or banking licenses depending on how a crypto asset is structured. Although the U.S. still lacks a unified federal crypto statute, the international trend toward recognizing VASPs and stablecoin issuers as distinct regulatory categories suggests that further specialized licensing frameworks may eventually emerge at the federal level as well. For now, however, most U.S. retail‑facing crypto businesses must treat state licenses as their primary regulatory passport, with federal regimes layered on top for specific activities.

For users and investors, the key takeaway is that a U.S. crypto firm describing itself as “licensed” is most likely referring to an array of state money transmitter licenses, perhaps supplemented by other federal approvals. Understanding exactly which licenses a firm holds, and what those licenses cover, remains essential due diligence.

- 01MiCA EU passporting wave↗

Bitpanda, MoonPay, BitGo, and others winning single-jurisdiction MiCA licenses that unlock all 27 EU markets created an unmistakable competitive-moat story readers tracked as a bellwether for who survives European crypto.

- 02US compliance impossibility↗

Robinhood's explicit admission that even a full securities-license stack and TradFi legal army cannot achieve compliant US crypto operations crystallized the regulatory arbitrage driving offshore licensing.

- 03TradFi custody licensing race

Commerzbank and Deutsche Bank filing for or securing crypto custody licenses signaled that regulated institutional custody was becoming a competitive necessity for legacy banks, not a niche experiment.

- 04Dubai VASP licensing surge↗

OKX, Backpack, and Crypto.com winning VARA authorizations showed Dubai's VARA emerging as the primary regulated alternative for exchanges stalled or blocked in Asia and the US.

- 05GPL vs BUSL open-source abuse

Cronje's callout of a protocol rebranding his GPL3 code under a restrictive BUSL license exposed how commercial forks monetize open-source DeFi infrastructure without attribution or reciprocity.

- 06DeFi frontend MiCA existential threat↗

The warning that EU regulators may require MiCA licenses for DeFi frontends on normal internet domains raised the question of whether decentralized interfaces can legally exist in Europe at all.

The European Union: MiCA Authorization As A Regional Passport

What a MiCA license is and what it covers

The European Union’s Markets in Crypto‑Assets Regulation (MiCA) represents one of the most comprehensive attempts to create a unified licensing framework for crypto assets and crypto service providers. MiCA institutes uniform EU market rules for crypto‑assets that are not already regulated under existing financial services legislation, such as traditional securities or e‑money instruments. It creates categories for different classes of tokens, including asset‑referenced tokens and e‑money tokens, and sets out rules for those issuing and trading them.

For crypto‑asset service providers (CASPs), MiCA defines activities such as operating a trading platform, providing custody and administration of crypto‑assets, exchanging crypto for fiat and vice versa, executing orders on behalf of clients, and providing advice. CASPs must obtain authorization in an EU member state, meet governance and capital requirements, implement robust security and incident management procedures, and provide clear, fair information to clients. Once authorized, they can passport their services throughout the EU, similar to how banks and investment firms operate under other EU directives.

MiCA’s key policy objectives are to enhance transparency and disclosure, ensure authorization and supervision of crypto‑asset activities, and support market integrity and financial stability. The regulation is designed to regulate public offers of crypto‑assets, giving consumers better information about the associated risks and intentions of issuers. For stablecoin‑like instruments, especially asset‑referenced and e‑money tokens, MiCA adds stricter requirements around reserves, redemption, and significant issuer oversight, reflecting regulators’ concerns about systemic risk.

WhiteBIT: consolidating European operations under MiCA

WhiteBIT EU’s licensing path exemplifies how MiCA is reshaping the competitive landscape. WB‑Shield Innovations GmbH, operating as WhiteBIT EU, announced that it has obtained authorization under MiCA in Austria. This authorization consolidates the exchange’s previous efforts to secure regulatory approvals across various European jurisdictions, allowing it to operate under a single, harmonized regime rather than a patchwork of national registrations. With a MiCA license, WhiteBIT can serve users across the EU under one regulatory framework, simplifying compliance and enhancing its ability to launch new services for millions of customers.

Strategically, securing one of the early MiCA licenses is a differentiator. It signals to institutional clients and regulators that the exchange can meet EU‑level standards on risk management, consumer protection, and transparency. It also provides a measure of regulatory certainty for product launches, such as new trading pairs, staking services, or custody offerings, since these are now explicitly covered under CASP categories. For rivals, the WhiteBIT example underscores that MiCA authorization is not optional: without it, long‑term EU market access is at risk.

Binance: the cost of missing the EU license window

The experience of Binance shows the downside risk of failing to secure MiCA authorization in time. According to reports, Greece’s capital markets regulator is preparing to reject Binance’s application for a MiCA license. Although Binance has denied receiving any official rejection and maintains that it has complied with regulatory requirements, a rejection in Greece would leave the exchange without the regulatory approval needed to continue serving EU customers after MiCA’s full entry into force. Without a MiCA license in any member state, the world’s largest crypto exchange could effectively be forced to exit the EU market once transitional periods end.

This situation highlights a key structural feature of MiCA: because authorization is passportable, a CASP only needs one member state approval to operate across the bloc, but without any authorization it cannot operate legally in any of them. For firms that grew rapidly under fragmented national regimes, MiCA compresses years of regulatory risk into a single licensing decision. Exchanges and custodians that fail to obtain a MiCA license may need to pivot to other regions or radically reconfigure their business models. For EU users, it underscores that a platform’s long‑term availability is now deeply tied to its licensing status.

Prediction markets and gambling licenses in Europe

MiCA does not address every type of crypto platform. Prediction markets, which allow users to bet on real‑world events via tokenized contracts, occupy a regulatory gray zone between financial derivatives and gambling products. Several European jurisdictions have recently taken the view that such platforms constitute gambling and require gambling licenses rather than financial services authorizations.

Spain offers a clear example. The country’s Consumer Rights Ministry, which oversees its gambling watchdog, temporarily blocked US‑based prediction markets Polymarket and Kalshi for operating without a gambling license. An order published in the Spanish state gazette stated that the companies were allegedly breaching rules requiring online operators offering wagers on uncertain outcomes to hold administrative authorization. The suspension is expected to last three to four months while a formal investigation examines whether the platforms meet technical and consumer safeguard requirements, including identity verification and access controls to keep minors off the platforms. Spain’s action follows similar decisions by France, Belgium, Poland and Italy, where authorities have treated Polymarket’s operations as unlicensed gambling.

Under Spain’s gambling laws, operators seeking to enter the market must first secure a general license covering categories like betting and gaming, and then apply for specific licenses for particular products. Compliance extends beyond simple registration to include responsible gambling measures, advertising rules, and technical standards. For crypto prediction markets, this means that even if their tokens and smart contracts fall outside MiCA’s scope, they can still be forced offline if they lack the appropriate gambling licenses. The lesson is that “being a crypto protocol” does not exempt a platform from non‑securities regulations such as betting and gaming law.

Ripple receives full EU Electronic Money Institution License in Luxembourg.

Ripple somehow still making big moves, XRP meanwhile still being sold to make these moves

Middle East And Asia: VARA, SVF, MAS, Hong Kong, Australia, Brazil

Dubai’s VARA: a bespoke virtual asset regulator

Dubai’s Virtual Assets Regulatory Authority (VARA) is one of the first stand‑alone regulators dedicated entirely to virtual assets. VARA operates a licensing framework that covers a spectrum of activities, including virtual asset broker‑dealer services, custody services, exchange services, lending and borrowing, management and investment services, transfer and settlement, advisory services, and issuance. Each of these activities is a separate licensed activity with its own conditions and risk profile. VASPs seeking a VARA license must complete a two‑stage application process, starting with an initial approval and followed by a full market license once they meet operational conditions.

Kraken’s expansion into Dubai illustrates how major global exchanges use VARA licenses to anchor their regional growth. Payward FZCO, Kraken’s local entity, has been licensed by VARA as a Virtual Asset Service Provider under a broker‑dealer and investment and management license category. This authorization permits Kraken to provide virtual asset services to both retail and professional investors in the Emirate of Dubai, subject to VARA’s regulatory framework and conditions. The license also enables Kraken to build out institutional products and integrate Dubai into its global liquidity network under clear regulatory oversight.

VARA’s approach underscores that some jurisdictions view crypto as important enough to warrant a purpose‑built regulator rather than folding it into existing securities or banking agencies. For market participants, this can provide greater clarity about expectations but also introduces a specialized rulebook whose nuances must be understood before launch.

Central Bank of the UAE: stored value facilities and crypto payments

While VARA handles many crypto investment services, the Central Bank of the UAE (CBUAE) oversees broader payment services, including stored value facilities (SVFs). Crypto.com has announced that it received an SVF license from the CBUAE, positioning it as the first virtual asset service provider to obtain this license from the central bank. The license enables Crypto.com to support virtual‑asset payments for government services, effectively integrating crypto‑denominated value into official payment channels.

An SVF license focuses on safeguarding customer funds, ensuring redemption, and managing operational and cybersecurity risks associated with stored value wallets. For a crypto platform, holding such a license signals that the firm is not only a trading venue but also a regulated payments provider under central bank oversight. It broadens the use cases for its tokens and stablecoins from trading and speculation to retail payments and bill settlement. When combined with VARA authorizations, the UAE’s dual‑track licensing regime lets a single firm handle both investment and payments use cases within a coherent regulatory perimeter.

Singapore’s MAS: licensing and revocation power

Singapore has positioned itself as a leading hub for digital assets, but it has also emphasized strict supervision of licensed entities. Under the Payment Services Act, firms that provide digital payment token services must obtain a license, and large operators can be designated as major payment institutions subject to enhanced requirements. MAS has demonstrated that these licenses can be revoked when firms fail to meet regulatory expectations.

In a high‑profile example, MAS revoked the major payment institution license of Bsquared Technology (also known as BSQ), a local crypto liquidity provider. The revocation followed MAS’s discovery of “serious breaches” of regulatory requirements, including significant weaknesses in the firm’s risk‑management practices, conflict‑of‑interest policies, and failures to comply with outsourcing guidelines. MAS also stated that Bsquared had provided false or misleading statements on multiple occasions during its time as a licensee. The license was revoked as of May 14, roughly 16 months after it had been granted.

Importantly, Bsquared informed MAS that it held no outstanding customer assets, and the authority required the company to submit a closure certificate issued by its auditors confirming that all customer funds had been returned to their intended recipients. This case underscores that licensing is not a permanent badge but a conditional grant that can be withdrawn. For clients, a license offers additional recourse and supervisory oversight, but it does not eliminate the need for due diligence on a firm’s governance and operational integrity.

Hong Kong: stablecoin issuer licenses and the Stablecoins Ordinance

Hong Kong has adopted a particularly focused licensing regime for stablecoin issuers. Under the Stablecoins Ordinance, which came into force on 1 August 2025, the business of issuing fiat‑referenced stablecoins is a regulated activity, and a license is required. The Hong Kong Monetary Authority is responsible for this regime and has published detailed guidance for prospective licensees. Entities interested in applying must familiarize themselves with the requirements and are encouraged to reach out to the HKMA for early discussions via a dedicated contact channel.

The licensing framework requires stablecoin issuers to maintain adequate backing assets, robust governance, and transparent disclosure about reserve composition and redemption mechanisms. HKMA’s communication emphasizes the importance of public confidence and financial stability, making clear that unlicensed issuance of fiat‑referenced stablecoins will not be tolerated. For crypto projects contemplating launches of Hong Kong dollar‑linked tokens or other fiat‑referenced instruments targeting Hong Kong users, the stablecoin license is now a prerequisite.

Hong Kong has already issued its first stablecoin licenses. The jurisdiction granted inaugural stablecoin issuer licenses to HSBC Holdings and a joint venture of Standard Chartered, allowing them to issue cryptocurrencies pegged to the local currency. These licenses position established banks as frontrunners in Hong Kong’s regulated stablecoin market, reflecting a regulatory strategy that initially favors well‑capitalized incumbents over crypto‑native startups. For DeFi and crypto issuers, this creates both opportunities for partnerships with licensed banks and barriers to direct participation in officially sanctioned stablecoin markets.

Australia: AFSLs for crypto exchanges and payment networks

Australia regulates many financial activities, including some crypto services, under the Australian Financial Services License (AFSL) regime. An AFSL is required for businesses that provide financial product advice, deal in financial products, or operate registered managed investment schemes. Crypto assets that are deemed financial products, as well as services such as derivatives, custodial arrangements, and certain payment products, can therefore fall under AFSL requirements.

Coinbase has secured an AFSL in Australia, with plans to use it as a foundation for expanding into equity trading and payments in the country. Bloomberg reporting indicates that after receiving an AFSL, Coinbase aims to broaden its offerings beyond pure crypto trading to include traditional financial products and integrated payment services. This illustrates how a single license can underpin multi‑asset platforms that handle both digital and traditional instruments.

Ripple, likewise, has announced plans to secure an AFSL to expand its blockchain‑based payments offering across the Asia‑Pacific region. The company described the AFSL as a key element in its strategy to deepen its presence in APAC and provide regulated cross‑border payments to a broader client base. By anchoring their operations in an AFSL, firms like Coinbase and Ripple are signaling that they intend to operate within the same licensing perimeter as mainstream financial service providers rather than on the fringes of regulation.

Brazil and the rise of VASP licenses in Latin America

Brazil is among the Latin American countries that have moved to regulate crypto service providers along VASP lines. Ripple has outlined plans to apply for a Virtual Asset Service Provider (VASP) license with the Central Bank of Brazil as it expands its payments offering in the country. This license would align Ripple’s local operations with Brazil’s evolving regulatory framework for crypto intermediaries, which is informed by FATF’s VASP standards. For companies providing cross‑border payment rails and liquidity solutions, local VASP authorization helps build trust with banks, regulators, and enterprise clients.

Latin America’s licensing trend reflects a broader shift from viewing crypto as simply a consumer asset to treating it as infrastructure for remittances, business payments, and capital markets. As more central banks and securities regulators adopt VASP‑style regimes, obtaining local licenses is becoming a prerequisite for serious expansion in the region.

MiCA CASP rules fully applied; EU crypto service provider licensing regime live

- 2025-04regulatory

Cayman Islands CIMA licensing rules take effect for custody and trading providers

Coinbase secures Australian Financial Services License (AFSL) for APAC expansion

HSBC and Standard Chartered receive first Hong Kong stablecoin issuer licenses

Stablecoin Licenses: A New Regulatory Class

Why stablecoins attract specialized licensing

Stablecoins, particularly fiat‑backed ones, sit at the intersection of payments, banking, and capital markets. They promise price stability relative to a reference asset, often a fiat currency, and can be used for everyday payments, remittances, collateral, and DeFi liquidity. Their potential to scale rapidly, combined with their role as quasi‑money, has prompted regulators to treat them differently from purely speculative crypto‑assets.

MiCA distinguishes asset‑referenced tokens and e‑money tokens and subjects them to enhanced authorization and supervision. Issuers must provide clear white papers, maintain appropriate reserves, and, in the case of significant stablecoins, meet additional governance and capital requirements. Hong Kong’s Stablecoins Ordinance similarly focuses on fiat‑referenced stablecoins, requiring issuers to obtain a license from the HKMA and comply with detailed oversight on backing assets and redemption processes. Delaware’s proposed framework targets payment stablecoin issuers, recognizing their distinct role in the financial system and subjecting them to a licensing regime separate from general money transmitters.

These specialized licenses reflect concerns about run risk, systemic contagion, and consumer harm if a widely used stablecoin were to “break the buck” or suffer a governance failure. They also reflect an acknowledgment that stablecoins are likely to become embedded in mainstream payment rails. Consequently, regulators keen to promote innovation while preserving stability see dedicated stablecoin licenses as a way to set clear expectations.

Comparing stablecoin licensing regimes

Although each jurisdiction is unique, there are common patterns in how stablecoin issuance is being licensed. The table below gives a simplified comparison among four emerging regimes.

| Jurisdiction | Regulator / Law | Scope of Stablecoin License | Key Themes |

|---|---|---|---|

| European Union | ESMA / MiCA | Asset‑referenced tokens and e‑money tokens not covered by existing law; issuers and service providers must be authorized | Harmonized EU rules on transparency, reserves, and supervision to support market integrity and financial stability |

| Hong Kong | HKMA / Stablecoins Ordinance | Issuance of fiat‑referenced stablecoins as a regulated activity | License required as of 1 Aug 2025; focus on reserve quality, governance, and public confidence |

| Hong Kong (market example) | HKMA (licenses to firms) | First licenses granted to HSBC and Standard Chartered JV to issue HKD‑pegged stablecoins | Priority for well‑capitalized incumbents; bank‑backed stablecoins at the core of regulated ecosystem |

| Delaware (proposed) | State banking regulator / SB19 | Establish licensing framework for payment stablecoin issuers and digital asset service providers | Specialized design for payment stablecoins; aims to attract issuers while ensuring oversight |

In each case, stablecoin licenses go beyond simple registration. They typically involve scrutiny of reserve assets, board and management qualifications, risk management frameworks, and business continuity plans. Issuers must often provide detailed disclosures about how the stablecoin works, how it is backed, and what rights users have. Some regimes may require segregation of reserves with regulated custodians or impose restrictions on investment of backing assets.

Implications for issuers, DeFi, and users

For stablecoin issuers, specialized licensing can be both a barrier and a competitive edge. Large financial institutions like HSBC and Standard Chartered, with existing infrastructure and compliance teams, can more easily absorb the cost of obtaining and maintaining a stablecoin issuer license. Crypto‑native companies, particularly decentralized teams, may find it harder to align their governance structures with regulator expectations, pushing them toward partnerships or hybrid models.

In DeFi, regulated stablecoins may become the “safe collateral” of choice for institutional participation, especially when they are clearly backed by bank deposits or high‑quality liquid assets under strict supervision. However, licensing requirements may also restrict how such stablecoins can be used in permissionless protocols, for example by limiting their availability in jurisdictions where unregulated DeFi pools dominate. Smaller, unregulated stablecoins may persist in the open ecosystem, but they will likely face heightened scrutiny and limited integration with regulated venues.

For users, the emergence of stablecoin licenses means that not all “dollar‑pegged” or “HKD‑pegged” tokens are equal. A licensed stablecoin issuer must meet defined regulatory standards, while unlicensed issuers may offer higher yields but carry greater risk. As regulated stablecoins are integrated into payment flows—such as government service payments in the UAE through licensed providers—users will increasingly confront a choice between regulated, licensed tokens and more experimental alternatives.

Software, Code, And Content Licenses In Crypto

Open‑source and protocol licenses

Beyond regulatory authorizations, crypto ecosystems are governed by software licenses. Many DeFi protocols and blockchain projects are open source, releasing their code under licenses such as MIT, Apache, GPL, or custom business source licenses. These licenses determine who can copy, modify, and deploy the code, under what conditions, and whether derivative projects must also open source their changes.

License choices are strategic. A permissive license like MIT allows anyone, including competitors, to fork and commercialize the code with minimal obligations. Copyleft licenses, such as GPL, require derivative works to remain open source, thereby preventing proprietary forks from capturing closed‑source value atop community work. Business source or time‑delayed open‑source licenses attempt to balance openness with commercial protection, often restricting commercial use for a period before transitioning to a more permissive license.

In DeFi, accusations of “license violations” have become a way to contest forks or clones that reuse code without following terms. Protocol teams sometimes warn would‑be competitors that copying their stableswap or AMM logic in ways that breach non‑commercial clauses or attribution requirements could be unlawful and strategically unwise, since it may expose them to legal action and reputational damage. These conflicts reveal that despite rhetoric about “code is law,” real‑world legal contracts—licenses—still govern who can do what with the underlying software.

NFT, content, and data licenses

NFTs added another layer of licensing complexity. Owning an NFT does not automatically confer ownership of the underlying artwork, music, or media; it is the license terms that define what rights holders have. Some projects grant only personal, non‑commercial display rights; others grant broad commercial rights up to certain revenue thresholds; a minority use public‑domain style licenses such as CC0. These differences significantly affect the value and utility of NFT collections, especially for brands and creators planning derivative works.

Similarly, data and content used in crypto, from price feeds to AI‑generated art and in‑game assets, may be subject to licensing terms. Market data providers, for example, often license their feeds under strict conditions that limit redistribution or commercial use. As crypto projects increasingly integrate AI agents, third‑party APIs, and off‑chain compute, they must navigate a web of end‑user license agreements and data licenses that may constrain how their smart contracts can interact with external services.

The AI sector’s experience with shifting software and model licenses is instructive. Some open‑source AI models have changed from permissive to more restrictive licenses after gaining popularity, raising concerns about legal certainty and trust. For on‑chain AI projects or crypto wallets incorporating AI agents, such license shifts can pose real operational risks, especially if products were launched on the assumption of enduring open‑source terms.

End user license agreements and platform terms

Finally, centralized platforms—from exchanges to cloud providers—govern their relationships with users through end‑user license agreements and terms of service. For a crypto exchange, these documents define what services the license actually covers, how user assets are treated in insolvency, what rights the platform has to halt trading or close accounts, and which jurisdiction’s law applies. For cloud services and tooling, EULAs dictate how nodes, validators, or AI agents can use compute and storage resources, whether certain crypto workloads are prohibited, and how liability is allocated.

These contractual licenses are often overlooked but critically important. A user may feel reassured that a platform is “licensed” by a regulator, but the EULA may still contain clauses that allow the platform to suspend services or alter rules with limited recourse. Conversely, builders who rely heavily on licensed platforms or APIs must ensure that their own contracts with users accurately reflect upstream license constraints. In an increasingly regulated and institutionalized crypto environment, reading the fine print of both regulatory licenses and private licenses is a necessary discipline.

The Bank of Russia proposed a new crypto framework expanding retail and professional investor access under tiered limits, while keeping crypto barred from domestic payments and routed through licensed intermediaries, with full legislation targeted for 2026.

Jurisdictional fragmentation forces operators to pursue dozens of incompatible licenses globally with no mutual recognition outside the EU's MiCA passporting system.

License revocation or application withdrawal — as seen with Gate.io winding down Hong Kong services and MAS revoking Bsquared's permit — immediately suspends all local user access.

Robinhood's case demonstrates that even firms with every existing securities license and a large TradFi legal apparatus cannot deterministically achieve crypto compliance in the US.

MiCA concentrates EU crypto authorization in national competent authorities, with BaFin and the Netherlands AFM issuing passports that carry disproportionate pan-European leverage.

- Open-source / IPMedium

GPL3-to-BUSL relicensing by commercial forks creates legal ambiguity and community credibility damage without clear on-chain enforcement mechanisms in decentralized ecosystems.

Current licensing frameworks universally target custodians and service providers rather than on-chain protocol logic directly, leaving smart contract risk outside the immediate regulatory perimeter.

Licenses As Gateways For Launch, Payments, And Market Structure

Licenses as go/no‑go milestones for launches and expansion

For crypto businesses, licenses have become central milestones in product launches, geographic expansion, and partnership strategies. WhiteBIT’s MiCA authorization in Austria was not just a legal formality; it was the culmination of efforts to consolidate its European presence under one framework and unlock access to EU clients through a single regulatory passport. Binance’s struggles with MiCA authorization, by contrast, show how missing such a license can jeopardize an entire regional strategy.

In payments, licenses enable firms to move beyond speculative trading and into everyday financial services. Ripple’s pursuit of an AFSL in Australia and a VASP license in Brazil underpins its ambition to provide regulated cross‑border payments to institutional clients in APAC and Latin America. Alchemy Pay’s stepwise acquisition of state money transmitter licenses in the U.S. allows it to roll out compliant fiat‑crypto gateways and stablecoin‑based payment infrastructure to a growing number of states. Crypto.com’s SVF license in the UAE positions it to support virtual‑asset payments for government services, embedding crypto rails into public payment systems. Kraken’s VARA license in Dubai allows it to serve both retail and professional investors in a major regional hub under a specialized virtual asset regime.

These examples illustrate a broader pattern: a license is increasingly the “launch button” for new products and markets. Without it, even technically robust protocols and platforms cannot legally operate at scale.

The costs of non‑compliance: suspensions, exits, and trust damage

The flip side of licensing is enforcement. Firms that operate without required licenses, or breach the conditions of granted licenses, face suspensions, fines, and forced exits.

Spain’s action against Polymarket and Kalshi shows how unlicensed operations can be interrupted even when the underlying technology is novel. By treating their prediction markets as unlicensed gambling, Spanish authorities ordered temporary blocks pending an investigation, emphasizing the absence of required technical and consumer safeguards such as identity verification and minor protections. The resulting three‑ to four‑month suspension disrupts business and signals to other jurisdictions that similar platforms warrant scrutiny.

Singapore’s revocation of Bsquared’s major payment institution license underlines that even licensed firms can lose their status if they fail to maintain adequate governance, risk management, and truthful communication with regulators. The requirement that Bsquared confirm the return of all customer funds via an auditor‑issued closure certificate adds operational and reputational cost. For customers, such episodes erode trust not just in the affected platform but in the broader sector, especially when licenses are perceived as quality seals.

Binance’s potential inability to secure a MiCA license similarly shows how a licensing failure can threaten a firm’s access to an entire regional market. Even if customers can migrate to alternative platforms, the uncertainty around continuity of service, and the risk of abrupt changes in access, creates friction and may drive some users back to less regulated venues or self‑custody options.

Impact on innovation, competition, and decentralization

Licensing inevitably shapes who can compete in crypto markets. On one hand, licensing regimes can promote stability, transparency, and consumer protection, making it easier for mainstream investors and institutions to participate. On the other, licensing can be costly and complex, favoring incumbents and well‑capitalized players.

Hong Kong’s choice to grant its first stablecoin licenses to HSBC and a Standard Chartered joint venture illustrates how regulators may prioritize banks in early stages of a regime. These institutions have the resources and risk‑management expertise to meet stringent requirements, but their dominance may limit the space for smaller, crypto‑native issuers to experiment. In the EU, MiCA gives CASPs that can meet EU‑wide standards a powerful passport, but it may also raise the barrier to entry for small exchanges that previously operated under more lenient national regimes.

For DeFi and decentralized protocols, the challenge is more nuanced. Many licensing frameworks assume identifiable corporate entities and centralized governance, which do not map cleanly onto DAO‑governed systems or fully permissionless networks. This creates pressure either to “wrap” decentralized protocols in licensed front‑ends or to limit the reach of decentralized tools in regulated markets. The resulting hybrid models—licensed gateways atop permissionless infrastructure—could shape the future structure of crypto markets, dividing them into regulated, licensed zones and open, unlicensed zones with very different risk and access profiles.

How To Read A Crypto License: Practical Considerations

For users, developers, and investors, understanding what a license actually covers is crucial. A firm might highlight one license prominently—for example, a VARA broker‑dealer license, an MAS major payment institution license, or a MiCA CASP authorization—but the practical implications depend on the fine print.

The first step is to identify the licensing authority and the specific category of license. VARA’s framework, for instance, distinguishes broker‑dealer services, custody, exchange services, lending and borrowing, management and investment, transfer and settlement, advisory, and issuance. A platform that holds only a broker‑dealer license may not be authorized to operate an exchange or provide custody, and vice versa. Similarly, a Hong Kong stablecoin license from the HKMA applies specifically to fiat‑referenced stablecoin issuance, not to broader crypto trading. In the EU, a MiCA CASP license covers defined crypto‑asset services, while issuance of certain stablecoins falls under asset‑referenced or e‑money token categories with separate obligations.

Second, it is important to understand the geographic scope of a license. State money transmitter licenses in the U.S. are valid only in the issuing state, requiring multi‑state firms to build a “quilt” of authorizations as Alchemy Pay has done. By contrast, MiCA licenses in one EU member state can be passported across the entire bloc. VARA licenses apply to the Emirate of Dubai, whereas the Central Bank of UAE’s SVF license may have broader implications for payment flows within the UAE. Misunderstanding geographic coverage can lead to misplaced confidence about what protections apply and where.

Third, the conditions and history of a license matter. MAS’s revocation of Bsquared’s license underscores that regulators can and do enforce against non‑compliance. A firm that highlights a newly obtained license but has a track record of enforcement actions elsewhere may warrant closer scrutiny. Conversely, a firm with multiple licenses across jurisdictions, a clean supervisory record, and transparent disclosures about its compliance program may be more trustworthy, even if its products are similar to those of less regulated competitors.

Finally, users and builders should recognize that regulatory licenses are only one part of the licensing landscape. Software licenses, content licenses, and EULAs govern how code and services can be used. These private licenses may impose restrictions or allocate risks in ways that are not obvious from regulatory status alone. A full understanding of a crypto project’s risk and rights profile therefore requires looking both at public regulatory licenses and private contractual licenses.

Conclusion

Licenses in crypto are no longer an afterthought or a niche legal detail. They are becoming the primary interface between digital asset innovation and the legal systems that govern finance, commerce, and intellectual property. On the regulatory side, licenses determine who may run an exchange, issue a stablecoin, operate a payment rail, or offer prediction markets, under what conditions, and in which jurisdictions. Frameworks such as MiCA in the EU, VARA in Dubai, MAS’s Payment Services Act in Singapore, HKMA’s stablecoin regime in Hong Kong, and emerging state‑level stablecoin laws in the United States are converging on the view that crypto activities must sit within supervised licensing regimes rather than outside the perimeter.

Concrete examples bring this into focus. WhiteBIT’s MiCA license in Austria provides a single regulatory passport across the EU, while Binance’s potential MiCA setbacks in Greece threaten its EU footprint. Kraken’s VARA authorization, Crypto.com’s SVF license, and Ripple’s pursuit of AFSL and VASP licenses illustrate how payments and trading businesses treat licensing as a strategic pillar for expansion. Spain’s blocking of Polymarket and Kalshi and Singapore’s revocation of Bsquared’s license show that regulators will not hesitate to act against unlicensed or non‑compliant operators. In stablecoins, specialized licensing regimes reflect concern about systemic risk and are already shaping which issuers—banks versus crypto‑natives—dominate regulated markets.

At the same time, software and content licenses continue to govern the open‑source code, NFTs, data, and AI components that make up the crypto stack. Disputes over code copying and license violations remind developers that legal rights do not disappear simply because code is deployed on‑chain. End‑user license agreements on exchanges, cloud platforms, and AI systems define users’ rights and remedies in ways that may matter as much as regulatory status.

For users, builders, and investors, the practical implication is that “licensed” has become a loaded term. It can signal real regulatory oversight and consumer protection, but only if one understands who issued the license, what it covers, and how it interacts with other legal obligations. As the crypto industry matures, literacy about licensing—both regulatory and contractual—will be as important as understanding consensus algorithms or tokenomics.

Outlook

Looking ahead, licensing will likely become even more central to crypto’s evolution. As MiCA is fully implemented, EU regulators refine stablecoin supervision, and jurisdictions such as Hong Kong, Dubai, Singapore, Brazil, and Delaware iterate on their frameworks, the global map of crypto licenses will continue to shift. Firms that anticipate these changes, invest early in licensing strategies, and align their technical architectures with legal requirements will be best positioned to launch and scale new products, from payments networks to stablecoins and on‑chain AI agents. Those that ignore licensing, or treat it as a one‑time box‑ticking exercise, may find themselves sidelined by enforcement actions, market exits, or lost trust. In a world where crypto increasingly plugs directly into mainstream finance and public services, licenses have become not just a regulatory hurdle but a core part of the infrastructure of digital asset markets.

Latest License news

Ripple to secure Australian Financial Services License, expanding payments offering across APACRipple receives full EU Electronic Money Institution License in Luxembourg.The Bank of Russia proposed a new crypto framework expanding retail and professional investor access under tiered limits, while keeping crypto barred from domestic payments and routed through licensed intermediaries, with full legislation targeted for 2026.Hybrid crypto platform Byrrgis has secured an EU MiCA license ahead of its January 15 launch and opened a waitlist for early access. The regulated hub will combine CEX and DEX features, offering automated portfolio packs and advanced trading tools. Securitize Scores EU DLT Pilot License: Set to Launch Regulated Tokenization Platform on Avalanche.

Securitize Scores EU DLT Pilot License: Set to Launch Regulated Tokenization Platform on Avalanche. The American Independent Community Bankers Association urges the OCC to reject Sony's stablecoin license.

The American Independent Community Bankers Association urges the OCC to reject Sony's stablecoin license.Sources

- https://wifpr.wharton.upenn.edu/50-state-review-of-cryptocurrency-and-blockchain-regulation/

- https://www.esma.europa.eu/esmas-activities/digital-finance-and-innovation/markets-crypto-assets-regulation-mica

- https://markets.businessinsider.com/news/stocks/whitebit-eu-secures-mica-license-in-austria-expanding-regulated-crypto-services-across-europe-1036262579

- https://www.facebook.com/GreeceHighDefinition/posts/greece-rejects-binance-licence-putting-eu-operations-at-riskthe-worlds-largest-c/1584693756443769/

- https://thenextweb.com/news/spain-blocks-polymarket-kalshi-gambling-licence

- https://blog.kraken.com/news/uae-vara-authorization

- https://www.businesstimes.com.sg/singapore/mas-revokes-bsquared-crypto-permit-over-serious-breaches

- https://crypto.com/us/company-news/cryptocom-receives-uae-stored-value-facilities-license-to-enable-virtual-asset-payments-for-government-services

- https://www.bloomberg.com/news/articles/2026-04-10/hsbc-stanchart-get-first-hong-kong-stablecoin-issuer-licenses

- https://legis.delaware.gov/json/BillDetail/GenerateHtmlDocument?legislationId=142988&legislationTypeId=1&docTypeId=2&legislationName=SB19

- https://ripple.com/ripple-press/ripple-deepens-commitment-to-brazil-with-expanded-payments-offering-growing-customer-momentum-and-vasp-license-application/

- https://ripple.com/ripple-press/ripple-to-secure-australian-financial-services-license-expanding-payments-offering-across-apac/

- https://alchemypay.org/news-and-press/alchemy-pay-expands-u-s-licensing-footprint-with-arizona-money-transmitter-license-approval

- https://briefglance.com/companies/alchemy-gps-singapore-pte-ltd-alchemy-pay/pulses/40244

- https://www.bloomberg.com/news/articles/2026-04-07/coinbase-plans-australia-expansion-after-securing-afsl-license

- https://www.chainalysis.com/glossary/virtual-asset-service-provider/

- https://www.hkma.gov.hk/eng/key-functions/international-financial-centre/stablecoin-issuers/

- https://www.vara.ae/en/licenses-and-register/licensed-activities/

- https://altenar.com/blog/gambling-laws-and-regulations-in-spain-your-compliance-guide-for-2025/

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…