In‑depth explainer on MiCA, the EU’s landmark Markets in Crypto‑Assets Regulation, covering stablecoin rules, CASP licensing, token white papers, DeFi and NFT edges, compliance timelines and how MiCA is reshaping European and global crypto markets.

+18 sources across the wider coverage universe

ClearBank secures MiCA approval to offer crypto services, targeting Circle’s EURC and USDC to enable regulated fiat-to-stablecoin conversions for institutional clients2026-04

ClearBank secures MiCA approval to offer crypto services, targeting Circle’s EURC and USDC to enable regulated fiat-to-stablecoin conversions for institutional clients2026-04 Clarity Act vote, SEC innovation exemption, and MiCA expiry converge in Q2 to test crypto's regulatory future2026-04

Clarity Act vote, SEC innovation exemption, and MiCA expiry converge in Q2 to test crypto's regulatory future2026-04 Societe Generale-FORGE brings bank-backed, MiCA-compliant USD stablecoin to MetaMask2026-04

Societe Generale-FORGE brings bank-backed, MiCA-compliant USD stablecoin to MetaMask2026-04 AllUnity expands MiCA-regulated euro stablecoin EURAU to Uniswap, Raydium, and Tempo via Flowdesk2026-04

AllUnity expands MiCA-regulated euro stablecoin EURAU to Uniswap, Raydium, and Tempo via Flowdesk2026-04 OpenPayd secures MiCA licence to offer regulated stablecoin rails across EEA2026-06

OpenPayd secures MiCA licence to offer regulated stablecoin rails across EEA2026-06 France says crypto firms without MiCA licences face blacklists and prosecution after June 302026-05

France says crypto firms without MiCA licences face blacklists and prosecution after June 302026-05

MiCA: The EU’s Markets in Crypto‑Assets Regulation Explained

The Markets in Crypto‑Assets Regulation, or MiCA, is the European Union’s first comprehensive rulebook for issuers of crypto‑assets and the firms that provide trading, custody, and related services around them, aiming to harmonize standards across all member states and close gaps in existing financial law. By setting uniform requirements for stablecoins, exchanges, custodians, and other intermediaries, MiCA is designed to make the EU a single regulated market for crypto while prioritizing consumer protection, financial stability, and market integrity.

The Policy Origins and Objectives of MiCA

MiCA emerged from the EU’s broader Digital Finance Strategy, which identified crypto‑assets as both a source of innovation and a potential locus of systemic risk. Before MiCA, crypto‑asset activities were regulated in a patchwork manner, with some tokens falling under existing regimes such as MiFID II or the E‑Money Directive, while many others sat entirely outside traditional financial supervision. This fragmented approach raised concerns about investor protection, uneven competition, and regulatory arbitrage, especially as stablecoins and large centralized exchanges started to reach mainstream scale. The EU’s political institutions responded by designing MiCA as a directly applicable regulation, meaning it takes effect uniformly across member states without requiring national transposition acts in the way directives do.

One of MiCA’s core objectives is to ensure that “same activity, same risk, same rules” applies in the crypto economy, aligning it with long‑standing principles in EU financial services regulation. Lawmakers wanted to avoid a repeat of earlier eras in which novel products grew rapidly outside the regulatory perimeter and only came under scrutiny after major failures or retail losses. High‑profile stablecoin experiments and the broader boom‑and‑bust cycle in global crypto markets crystallized fears that unregulated issuers and service providers could threaten consumer savings and, in extreme cases, monetary policy transmission. MiCA therefore places particular emphasis on disclosure, prudential safeguards for stablecoin issuers, and robust governance and risk management for intermediaries.

At the same time, MiCA is explicitly framed as an innovation‑friendly framework rather than a prohibitionist turn against crypto. EU institutions frequently present the regulation as a way to provide legal certainty so that compliant projects can scale across the bloc instead of navigating 27 different national regimes. This message resonates with parts of the industry that had already been operating under anti‑money‑laundering registration regimes, such as the Fifth Anti‑Money Laundering Directive (AMLD5), but lacked a clear licensing pathway for offering more complex crypto services. Policymakers were also acutely aware that the EU was competing with other global hubs for leadership in digital finance, and they viewed MiCA as a way to place Europe at the forefront of rule‑setting in this domain.

The regulation must also be understood in the context of a broader EU agenda around data, payments, and digital identity. While MiCA is focused on crypto‑assets, it intersects with payment services rules, e‑money legislation, and ongoing work on central bank digital currency, especially the digital euro. Although MiCA does not itself create a digital euro or redesign payment systems, it steers private stablecoin activity into a framework that is meant to be compatible with future public initiatives. This is particularly visible in the way MiCA treats stablecoins referencing non‑EU currencies, where caps and potential restrictions are justified partly in terms of monetary sovereignty and competition with the euro.

EU MiCA licenses near 230 before July 1 deadline as smaller crypto firms face shutdown pressure

The EU has issued roughly 230 MiCA licenses ahead of July 1, when unlicensed crypto service providers lose the ability to offer new services across the bloc. Germany leads with 56 approvals, followed by the Netherlands with 26 and France with 21, while about 40% of France's registered crypto service providers have not applied. MiCA is doing what regulation usually does in crypto: raising the floor for market resilience while thinning out smaller players that cannot absorb the compliance load.

Readers click MiCA most heavily not on compliance how-tos but on boundary questions — where the regulation stops (the DeFi decentralization exemption) and what it forcibly removes (stablecoin delistings) — revealing that the live commercial controversy is the perimeter of the rulebook, not the rulebook itself.↗

Scope and Key Concepts in MiCA

MiCA is intentionally broad in its definition of a crypto‑asset. It defines crypto‑assets essentially as digital representations of value or rights that can be transferred and stored electronically using distributed ledger or similar technology, while also specifying that covered tokens are those not already captured by existing EU financial services legislation. This carve‑out is essential because tokens that qualify as financial instruments under MiFID II or as traditional e‑money under prior rules remain governed by those regimes, not by MiCA. ESMA and national regulators are therefore working through practical questions about classification, including whether some tokens marketed as “utility” or “governance” tokens might in fact be financial instruments depending on their features.

Within that broad perimeter, MiCA introduces three headline categories of tokens. Asset‑referenced tokens, or ARTs, are designed to maintain a stable value by referencing one or more assets, such as a basket of currencies, commodities, or other crypto‑assets. E‑money tokens, or EMTs, are crypto‑assets intended to maintain a stable value by referencing a single official currency, and are treated in many ways like traditional e‑money, though now implemented over distributed ledgers. A third category captures all other crypto‑assets that are not ARTs or EMTs and are not financial instruments under other EU laws. These can include many so‑called utility tokens and payment tokens that are prevalent in retail‑oriented crypto markets. The differentiation matters because each category is subject to its own authorization, governance, and disclosure obligations.

MiCA also heavily regulates intermediaries through the concept of the crypto‑asset service provider, or CASP. CASPs include firms that operate trading platforms, provide custody or administration of crypto‑assets, exchange crypto‑assets for funds or other crypto‑assets, execute orders, place tokens, provide portfolio management, or give advice on crypto‑assets. In practice, this captures centralized exchanges, custodians, brokers, and various platforms that mediate access to tokens, although truly decentralized arrangements that lack an identifiable service provider raise more complex questions discussed later. CASPs need authorization from a national competent authority in one member state, and once authorized they can “passport” their services across the entire EU, in line with the bloc’s single‑market model.

Territorially, MiCA has both a geographic and a functional reach. It applies to issuers and CASPs that are established in the EU, but it can also capture non‑EU entities that actively offer services or make public offerings of tokens into the EU. This means global exchanges and stablecoin issuers must either obtain MiCA‑compliant authorization within the bloc or restrict EU residents’ access to certain products. The regulation is not designed as an extraterritorial regime in the same way as some financial sanctions frameworks, but given the size and attractiveness of the EU market, MiCA is already influencing business models far beyond Europe’s borders.

Non‑fungible tokens, or NFTs, occupy a more ambiguous space. MiCA nominally excludes crypto‑assets that are unique and not fungible with other tokens, but regulators have stressed that what matters is the actual economic function rather than marketing labels. ESMA’s consultations and industry feedback emphasize that large collections of purportedly “unique” tokens that in substance serve as mass‑market investment products could still fall under MiCA’s scope. This evolving interpretation underscores that MiCA’s boundaries are not static and that the classification of tokens will require case‑by‑case analysis as new business models emerge.

Timeline, Implementation, and National Dynamics

MiCA followed the EU’s standard legislative path, with proposals from the European Commission, negotiations among the Parliament and Council, and eventual adoption as Regulation (EU) 2023/1114. The regulation entered into force on 30 June 2023, twenty days after its publication in the Official Journal of the European Union. However, the EU opted for a staggered application schedule rather than making all obligations effective immediately. This phasing reflects both the perceived urgency of addressing certain risks—particularly around stablecoins—and the need to give industry and regulators time to prepare for a complex new regime.

The first major milestone was the application of Titles III and IV of MiCA, which govern asset‑referenced tokens and e‑money tokens, from 30 June 2024. From that date, issuers of ARTs and EMTs offering tokens in the EU or seeking admission to trading on EU platforms became subject to detailed authorization, reserve, and governance rules, and unregulated “stablecoins” could no longer be freely marketed to EU users. The rest of MiCA’s provisions, including rules for issuers of crypto‑assets other than ARTs and EMTs, requirements for CASPs, and the market‑abuse framework, began to apply from 30 December 2024. National regulators and ESMA have since been building out technical standards and supervisory practices to operationalize these obligations.

Transitional arrangements play a critical role in how this shift unfolds. CASPs that were already providing services in line with national law under AMLD5 registration regimes before 30 December 2024 are allowed to continue operating until 1 July 2026 or until their MiCA authorization is granted or refused, whichever comes first. This “grandfathering” period is meant to avoid abrupt service disruptions while encouraging firms to quickly seek full authorization as CASPs. Some member states, however, have signaled that they will adopt shorter transitional periods. The Netherlands, for example, has proposed reducing the transitional window for registered crypto service providers to six months, significantly accelerating the local compliance timeline. These divergences underscore that while MiCA is directly applicable, national authorities still wield discretion in areas such as transition management and supervisory intensity.

National political dynamics have also affected implementation. Poland, for instance, has faced repeated presidential vetoes of its Crypto‑Assets Market Act, which is intended to operationalize aspects of MiCA at the national level. As of early 2026, President Karol Nawrocki had vetoed the bill multiple times, leaving Poland as a laggard in aligning its domestic framework with MiCA even as it hosts a large number of virtual asset service providers. Legal analysts warn that if legislative deadlock persists beyond the end of the transitional period, firms operating in Poland could find themselves in a “legal vacuum,” potentially forced to shut down or relocate to other EU jurisdictions where MiCA paths are clearer. This illustrates how national politics can shape the on‑the‑ground reality of a nominally harmonized regime.

Alongside national processes, EU‑level authorities such as ESMA and the European Banking Authority (EBA) have been issuing guidelines, conducting consultations, and monitoring market developments. ESMA, for example, is building a central register of MiCA‑related information, including authorized CASPs, approved white papers, and entities that have been found non‑compliant. The EBA, together with ESMA, has published analyses of trends in crypto‑assets and DeFi to inform supervisory priorities and potential future adjustments to the framework. The European Commission has also launched a formal consultation on the functioning of EU crypto‑asset rules, gathering feedback on MiCA’s main building blocks to prepare for a potential post‑implementation review. This structured process underscores that MiCA is not a static endpoint but the foundation of a regulatory regime that will evolve over time.

- 01DeFi decentralization exemption threshold↗

The question of what 'fully decentralized' means under MiCA is a make-or-break legal threshold for every DeFi protocol serving EU users, making Danish FSA and ESMA guidance immediately actionable for builders and investors alike.

- 02Stablecoin delisting and conversion wave↗

Binance, Crypto.com, and Coinbase publicly removing or converting non-MiCA stablecoins — especially USDT — gave retail holders a concrete deadline that turned abstract regulation into urgent portfolio decisions.

- 03MiCA license race across EU member states↗

Bitpanda, MoonPay, BitGo, and others racing to secure licenses in Germany and the Netherlands highlights that a single national license unlocks all 27 EU markets — making the licensing geography a live competitive moat story.

- 04Market consolidation and M&A dynamics↗

The framing that MiCA rewards prepared firms with dominant pan-EU access and triggers acquisition of unlicensed competitors made compliance a competitive strategy story, not just a legal one.

- 05Asset classification ambiguity↗

ESMA's rejection of 'hybrid tokens' and the continued ambiguity around NFTs and governance tokens left large swaths of the market uncertain whether their products are in scope, driving demand for authoritative clarification.

- 06Interest-bearing and cross-chain stablecoin design↗

MiCA's ban on interest-bearing stablecoins and its unclear treatment of cross-chain bridges forced protocol designers to scrutinize whether yield mechanics or multi-chain architecture triggers e-money classification.

Stablecoins Under MiCA: ARTs, EMTs, and the New Reserve Regime

Stablecoins are arguably the centerpiece of MiCA’s risk‑focused provisions, and the regulation draws a sharp line between compliant, asset‑backed designs and more speculative or algorithmic models. Asset‑referenced tokens are defined as crypto‑assets that aim to maintain a stable value by referencing one or more assets or baskets, which can include currencies, commodities, or even other crypto‑assets. E‑money tokens, by contrast, reference a single official currency, such as the euro, and are meant to function as a means of payment, in close analogy to traditional e‑money. Both categories are brought into a strict framework that encompasses authorization of issuers, governance requirements, reserve management, disclosure, and ongoing supervision.

One key feature of MiCA is its hostility to algorithmic “stability” mechanisms that are not anchored in fully backed reserves. Tokens can no longer be marketed as “stablecoins” or “value‑referencing” unless they are genuinely backed by assets, and issuers must hold reserves that are safe, liquid, and segregated from their own assets. These reserves must be managed prudently, often through qualified custodians, and are subject to rules designed to ensure holders can redeem their tokens at par value at any time, particularly in the case of EMTs referencing a single currency. Algorithmic structures in which a token’s price stability depends mainly on demand dynamics, arbitrage mechanisms, or the value of related tokens do not satisfy these criteria and therefore cannot be presented to EU users as stablecoins under MiCA.

MiCA also pays special attention to tokens referencing non‑EU currencies, especially when such tokens are widely used within the EU. ARTs that reference non‑EU currencies are subject to strict caps, and tokens deemed to be “significant” or widely used may face restrictions or even prohibitions on certain uses. The rationale is to prevent private, foreign‑currency‑denominated tokens from undermining the status of the euro in everyday payments and savings within the EU. For example, euro‑area authorities have signaled discomfort with the idea that a dollar‑pegged stablecoin could become a dominant medium of exchange in European retail markets. MiCA therefore creates a framework in which euro‑denominated EMTs are favored, while foreign‑currency ARTs and EMTs are subject to more stringent constraints.

This regulatory stance has direct implications for existing stablecoin leaders. Circle, for instance, has positioned its USDC and euro‑denominated EURC as MiCA‑compliant tokens, emphasizing that of the top ten stablecoins by market capitalization, only USDC currently meets the new EU standards. Circle’s approach involves setting up an EU‑regulated issuer structure and ensuring that reserves, governance, and disclosure align with MiCA’s requirements. Other large stablecoin issuers face tougher challenges, particularly if their reserves or governance models do not fit neatly within MiCA’s expectations or if their tokens reference non‑EU currencies without sufficient safeguards. As a result, the roster of stablecoins readily available and prominently listed in the EU is undergoing a significant reshaping.

The impact extends into DeFi and trading infrastructure. Many decentralized finance protocols use stablecoins as base assets for lending, liquidity pools, and derivatives. As MiCA limits the circulation of non‑compliant stablecoins in the EU and encourages the growth of regulated EMTs and ARTs, DeFi projects that want to serve EU users must consider how to adapt their collateral and settlement structures. EBA and ESMA have noted that DeFi still represents only around 4% of global crypto‑asset market value locked, but they also emphasize that its growth could raise novel consumer and financial stability risks. The interplay between MiCA‑regulated stablecoins and DeFi protocols remains one of the most complex frontier issues in European crypto policy.

In practical terms, the shift toward MiCA‑compliant stablecoins is already visible in product design and marketing. Token issuers emphasize their adherence to reserve, audit, and governance requirements, while centralized exchanges curate listings and trading pairs that align with the new rules. Some projects are launching euro‑denominated tokens or re‑domiciling parts of their structure into the EU to take advantage of passporting across the bloc. Others may choose to restrict EU users or focus on regions with lighter stablecoin regimes, underscoring how MiCA’s treatment of stablecoins has become a central strategic variable for global crypto businesses.

Spain's CNMV rules out MiCA deadline extensions as Binance and unlicensed crypto firms face July 1 exit

Spain's CNMV says there will be no exceptions or extensions to the EU's end-of-June MiCA deadline, so unlicensed crypto firms must stop normal operations from July 1 and wind down in an orderly way. Binance is among the firms caught by the clock, with the regulator pushing affected platforms to transfer positions or return customer assets. Spain expects roughly 20 authorized crypto providers after 14 approvals and six advanced applications, making the message blunt: MiCA's grace period is over, even for the biggest exchange.

CASPs, Licensing, and Market Infrastructure Under MiCA

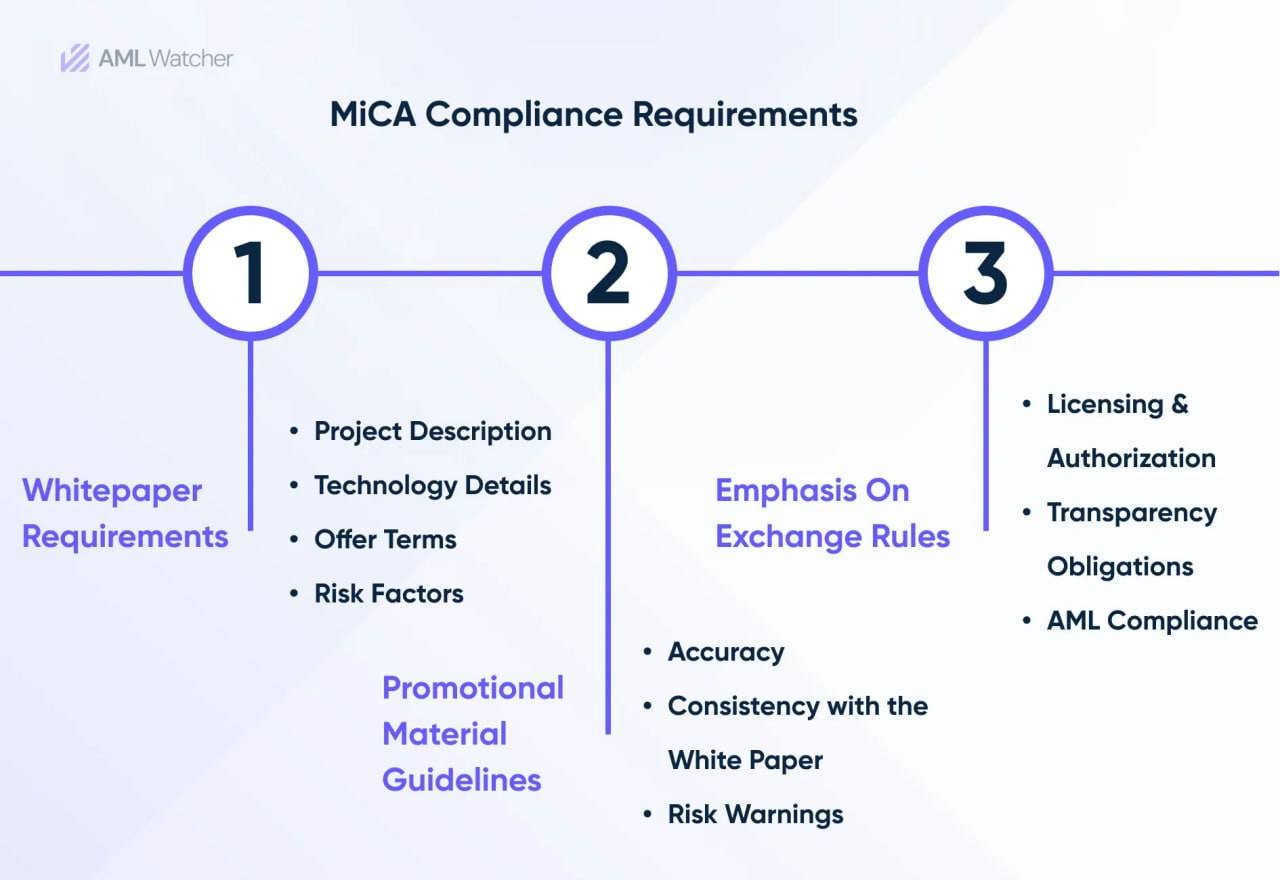

Beyond stablecoin issuers, MiCA creates a comprehensive licensing regime for crypto‑asset service providers. CASPs must obtain authorization from the competent authority in the member state where they are established, demonstrating that they meet requirements relating to governance, fit and proper management, organizational structure, safeguarding of client assets, prudential resources, and conduct of business. The application process generally requires detailed documentation of internal controls, risk management, IT and cybersecurity arrangements, and policies for handling conflicts of interest. Once authorized in one member state, CASPs can passport their services across the EU, which is particularly attractive for exchanges and custodians seeking scale.

The race to secure MiCA licenses has accelerated as transitional periods approach their end. Firms that previously operated under lighter AMLD5 registration regimes are now preparing for much more demanding authorization standards. Some, like WhiteBIT, have publicly highlighted their successful authorization under MiCA in countries such as Austria, positioning themselves as regulated players able to serve clients across the European Economic Area. External custodians and infrastructure providers are also stepping into this moment. BitGo Europe, for example, has launched MiCA‑ready crypto‑as‑a‑service platforms, enabling exchanges and fintechs to plug into regulated custody, KYC, and trading infrastructure as they navigate the licensing landscape. This clustering of services reflects a broader trend toward modular compliance solutions within the European crypto market.

The licensing process has not been smooth for all major players. News reports and public disputes about the status of certain large global exchanges’ MiCA applications illustrate the political and supervisory sensitivities involved, particularly when issues of governance, past compliance track records, or perceived systemic importance arise. Some media accounts have suggested that senior EU monetary policymakers have expressed unease about granting certain exchanges a central role in the EU market, especially in a period when the bloc is also exploring a digital euro. While the firms involved often contest such narratives and emphasize that they are working constructively with national regulators, the broader picture is one of intense scrutiny and negotiation ahead of key deadlines.

MiCA also tightens rules around market integrity and transparency. Issuers of crypto‑assets other than ARTs and EMTs must prepare, notify, and publish white papers that describe the project, the rights attached to the tokens, the underlying technology, and the main risks for buyers. ESMA is establishing a central register of these white papers, along with information on authorized CASPs and entities found to be non‑compliant. National authorities such as the Dutch AFM have clarified that for tokens already admitted to trading before 30 December 2024, white papers must be drawn up, notified, and published by 30 December 2027. For tokens admitted to trading after that date, MiCA white paper requirements apply without any transitional period. This creates a multi‑year pipeline of retroactive documentation for existing projects and prevents new token launches from bypassing disclosure rules.

Issuers and token projects increasingly treat MiCA alignment as a signaling device to markets. VeChain, for instance, has promoted the fact that its VET, VTHO, and B3TR tokens have been brought into compliance across the EU, with entries recorded in the ESMA register and white papers registered in advance of major deadlines. Project teams frame this as evidence of their commitment to proactive compliance and long‑term sustainability. Exchanges, in turn, may use MiCA status as one of their listing criteria, particularly for assets targeting EU retail access. In this way, regulatory compliance becomes part of the competitive landscape in token markets, not just a legal obligation.

Another pillar of MiCA concerns market abuse. The regulation extends familiar concepts such as insider dealing, unlawful disclosure of inside information, and market manipulation into crypto‑asset markets that fall under its scope. CASPs and issuers must establish systems to detect and report suspicious orders and transactions, similar to obligations in equity and derivatives markets. This framework aims to address concerns that thin liquidity, fragmented venues, and opaque ownership structures had made crypto markets particularly vulnerable to wash trading, pump‑and‑dump schemes, and other abusive practices. By aligning enforcement with established market‑abuse regimes, MiCA seeks to level the playing field between crypto and traditional finance and to protect retail participants from unfair or misleading conduct.

MiCA published in EU Official Journal; 18-month CASP transition clock starts

MiCA Title III and IV (stablecoin rules) enter force; e-money token and ART issuers must comply

Circle Mint France authorized as first MiCA-compliant stablecoin issuer in the EU

Coinbase launches 1:1 euro-to-EURC conversions, anchoring MiCA-compliant stablecoin liquidity

Full MiCA CASP provisions apply; crypto exchanges and custodians must hold EU licenses

Crypto.com delists USDT and nine other tokens for EU users ahead of March 31 deadline

Binance removes all non-MiCA stablecoin trading pairs for EEA users; industry-wide USDT offboarding complete

European Commission opens public consultation on functioning of MiCA rules, signaling potential MiCA 2 process

NFTs, DeFi, and the Boundaries of MiCA

MiCA’s formal scope leaves important edge cases unresolved, particularly around NFTs and decentralized finance. Legislators opted not to create a bespoke NFT regime within MiCA, instead excluding genuinely unique, non‑fungible tokens from most of its provisions. However, ESMA, industry associations, and national regulators have warned that many so‑called NFTs function in practice as fungible or quasi‑fungible investment products. The French Asset Management Association (AFG), for instance, has argued in ESMA consultations that a clearer distinction is needed between NFTs that represent truly unique digital art or collectibles and tokenized instruments that are economically indistinguishable from securities or units in collective investment schemes. Over time, guidance and enforcement actions will determine how aggressively regulators apply MiCA to large‑scale NFT projects that blur these boundaries.

DeFi presents an even more profound challenge. MiCA is largely built around the regulation of identifiable issuers and intermediaries, whereas DeFi aspires to deliver financial services through open‑source software, protocol governance by token holders, and automation via smart contracts. In their joint analysis of recent developments in crypto‑assets, the EBA and ESMA observe that DeFi remains a niche phenomenon, with total value locked in DeFi protocols representing roughly 4% of global crypto‑asset market value. They nonetheless highlight the potential for leverage, opacity, and composability in DeFi to transmit shocks or expose retail participants to complex risks they do not fully understand. MiCA touches DeFi indirectly via regulated stablecoins, CASPs that provide access to protocols, and the classification of governance tokens, but it does not create a direct licensing regime for DeFi protocols themselves.

Recognizing these gaps, some member states are exploring how DeFi might be addressed under, or alongside, MiCA‑era frameworks. Malta’s Financial Services Authority (MFSA), for example, has launched a discussion paper on decentralized finance and DAOs, inviting feedback on whether and how DeFi structures should be defined, supervised, or accommodated. The consultation examines topics such as decentralized autonomous organizations, guardian agents, account abstraction, and how varying degrees of decentralization should influence regulatory obligations. Importantly, the MFSA stresses that this is consultation material rather than a final rulebook, signaling an intention to test ideas before committing to a binding regime. Malta’s approach, including the suggestion that decentralization be treated as a spectrum rather than a binary, is likely to influence wider European debates about how to extend or complement MiCA for DeFi.

At the EU‑wide level, the European Commission has initiated a public and targeted consultation on the functioning of EU crypto‑asset rules, including MiCA’s main building blocks. This consultation, open until the end of August 2026, seeks input on whether MiCA adequately addresses emerging areas such as DeFi, staking, and more complex forms of tokenization. Market participants, academics, and civil society groups are invited to comment on the regulation’s effectiveness, proportionality, and potential unintended consequences. Some voices within the policy ecosystem argue that future reforms—often referred to informally as “MiCA 2”—should prioritize tokenization of real‑world assets and better integration with capital‑markets infrastructures, while others push for clearer and more direct rules for DeFi protocols and on‑chain governance. This debate is still unfolding and will shape how the EU’s crypto framework evolves beyond its initial launch phase.

The contrast between MiCA and other global initiatives is also important. In the United States, for example, DeFi is being pulled into regulatory debates via enforcement actions and proposed laws such as the CLARITY Act, which some legal experts describe as among the first to explicitly target decentralized protocols. Unlike MiCA, which primarily regulates centralized intermediaries and asset‑backed tokens, these emerging U.S. efforts could subject protocol developers and DAO participants to direct obligations, raising different questions about jurisdiction and code. For EU policymakers, this divergence presents both a challenge and an opportunity: they must decide whether to emulate more direct regulation of DeFi or continue to rely on regulating the “on‑ and off‑ramps” and core instruments such as stablecoins.

Token Issuers, White Papers, and MiCA Alignment

For token issuers, MiCA transforms the process of launching and maintaining a crypto‑asset in the EU. Issuers of crypto‑assets other than ARTs and EMTs must draft a white paper that meets content and format requirements, notify it to their national competent authority, and publish it in a manner that is easily accessible to the public. The white paper must describe the project’s purpose, governance, rights associated with the tokens, underlying technology, and material risks, including cybersecurity vulnerabilities and potential conflicts of interest. It must also avoid misleading statements and clearly disclose any limitations on the use or transfer of the tokens. These requirements bring token documentation closer to the prospectus‑like disclosures familiar in traditional capital markets, even though MiCA does not always require formal approval of the white paper by regulators for non‑stablecoin assets.

For ARTs and EMTs, the bar is higher. Issuers must obtain authorization, comply with detailed reserve and governance rules, and may be subject to enhanced supervision if their tokens are designated as “significant.” The authorization process scrutinizes not only the white paper but also the issuer’s business model, risk management, and systems for safeguarding reserves and executing redemptions. In this sense, issuing a MiCA‑compliant stablecoin in the EU resembles operating a regulated financial institution, with ongoing oversight and capital‑like obligations. Some market participants welcome this as a way to differentiate serious, well‑backed stablecoins from more speculative projects, while others worry that only large, well‑funded firms will be able to meet the requirements.

The AFM’s guidance on white papers for crypto‑assets underscores the long tail of compliance work that lies ahead. For tokens admitted to trading before the full application of MiCA, issuers and platforms must ensure that white papers are in place and notified by the end of 2027. This staggered timeline recognizes that many existing projects did not launch with MiCA‑grade documentation, but it also implies that token teams must revisit old materials, clarify rights and risks, and sometimes restructure governance to satisfy regulatory expectations. For newer tokens admitted to trading after 30 December 2024, there is no grace period: MiCA white paper rules apply immediately. This creates a higher barrier to entry for new projects but also aims to prevent a repeat of earlier cycles where retail users bought tokens based on thin, promotional documents.

Some projects have chosen to treat MiCA alignment as a competitive advantage and marketing theme. VeChain’s announcement that its VET, VTHO, and B3TR tokens are now compliant across the EU, with white papers registered and entries on the ESMA register, is one prominent example. The project frames this as evidence of “compliance, proactivity, and quality” and invites investors and partners to view regulated status as a feature rather than a burden. Other tokenization and Web3 initiatives, including those focused on travel, gaming, or enterprise use cases, have similarly emphasized that their token white papers are “MiCA‑ready” as they expand listings on European exchanges. Over time, such signaling may influence how institutional investors and large corporates select which crypto‑assets they are willing to hold or integrate into their products.

However, the process is far from purely promotional. KPMG and other advisory firms highlight the complexity of preparing MiCA‑ready documentation and internal governance. Projects must classify their tokens correctly, assess whether they might instead be financial instruments under MiFID II, and ensure that key information is both accurate and comprehensive. Misclassification can have serious consequences, including enforcement action for unauthorized investment services or mis‑selling. This has led many token teams to seek legal advice early in the design phase, long before launch, and in some cases to adjust token features or distribution models to fit within a clearer regulatory category. In this way, MiCA is shaping token design upstream, not only constraining behavior after launch.

OpenPayd secures MiCA licence to offer regulated stablecoin rails across EEA

OpenPayd says it has secured MiCA authorisation as a regulated CASP, letting it offer crypto-asset services across the EEA under one licence. The scope covers fiat-to-stablecoin on/off ramps, custody, wallet infrastructure and stablecoin transfers across major networks through a single API. The firm says it processes more than $240B in annualised volume for 1,100+ businesses including Kraken, eToro, OKX and B2C2, so this is a compliance land grab for stablecoin infrastructure, not a token launch.

Uneven enforcement across member states — with France's AMF already warning against lenient-jurisdiction passporting — creates compliance arbitrage risk and potential mid-stream rule tightening for licensed CASPs.

Mandatory delisting of USDT and other non-MiCA stablecoins across major EU exchanges fragments euro-zone liquidity and concentrates flow into a small set of approved instruments like USDC and EURC.

ERC-4626 yield vaults and cross-chain bridges occupy legal grey zones under MiCA — their classification as crypto-asset services or e-money substitutes remains unresolved, creating deployment risk for protocol developers.

MiCA's licensing costs and capital requirements systematically favor large incumbents and well-capitalized new entrants, accelerating consolidation and reducing the diversity of EU-accessible service providers.

ECB warnings that U.S. dollar stablecoins could drain EU capital under MiCA's framework, combined with Trump-era pro-crypto positioning, introduce macro-level uncertainty around euro-denominated crypto demand.

The 'fully decentralized' exemption has no bright-line EU-wide test; member-state-by-member-state guidance (e.g., Danish FSA) creates a patchwork that DeFi protocols must navigate without a single authoritative standard.

Exchanges, Custodians, and Service Design in a MiCA World

For centralized exchanges and custodians, MiCA fundamentally shifts business strategy in Europe. Firms that once operated with relatively light registration and KYC obligations must now demonstrate robust organizational and prudential resilience. CASPs are expected to segregate client assets from their own, maintain sufficient own funds, and implement policies for safeguarding keys and handling operational incidents. They must also establish complaint‑handling mechanisms, ensure transparent fee disclosures, and manage conflicts of interest, especially when they operate multiple lines of business such as own‑account trading, listing, and custody. These requirements push exchanges toward more institution‑grade models, resembling traditional brokers and trading venues in many respects.

As the July 2026 end of the transitional period approaches, firms are making strategic choices about whether to seek full authorization in one or more EU jurisdictions or to limit their exposure to the bloc. Some exchanges and custodians view MiCA as an opportunity to deepen ties with European banks, fintechs, and payment providers that prefer regulated counterparties. Others worry that the costs and constraints of compliance will erode the agility that made crypto platforms competitive in the first place. In response, service providers such as BitGo have positioned themselves as compliance enablers, offering MiCA‑ready custody, trading, and sub‑account structures so that platforms can plug into a regulated backbone instead of building everything in‑house. This modularization of compliance mirrors trends seen earlier in payments and banking.

The licensing landscape is also intensifying competition among EU member states to become preferred hubs for CASPs. Countries such as Germany, France, and the Netherlands already host significant crypto infrastructure and are refining their supervisory practices in light of MiCA. Smaller jurisdictions, including Malta, Cyprus, and some Central and Eastern European states, highlight their experience with fintech and digital assets, though they must also address concerns about supervisory rigor. Austria’s authorization of platforms like WhiteBIT under MiCA exemplifies how national regulators can attract business by combining clear, timely licensing processes with access to the broader EU market. At the same time, political controversies—such as repeated vetoes of implementing legislation in Poland—underscore that not all member states are moving in lockstep.

The interplay between MiCA and existing AML and sanctions regimes is another critical dimension. While MiCA itself is not an anti‑money‑laundering regulation, it operates alongside EU and national AML frameworks, which are being consolidated in parallel under new AML regulations and the creation of a European Anti‑Money Laundering Authority. CASPs must therefore design compliance architectures that integrate MiCA obligations with transaction monitoring, KYC, and screening requirements. Providers of regtech and compliance software, including those specializing in travel‑rule compliance and on‑chain analytics, see MiCA as a growth driver, since regulated CASPs will need scalable tools to meet both regulatory expectations and internal risk appetites.

Finally, MiCA prompts exchanges to reconsider product menus and risk controls. Certain leveraged products, derivatives, and high‑risk tokens may raise concerns under MiCA’s consumer‑protection provisions, especially when marketed to retail clients. CASPs must assess the appropriateness of services for different client categories and may need to implement suitability checks or restrict complex products to professional investors. This could lead to a more differentiated market in Europe, with some platforms specializing in regulated retail offerings and others focusing on institutional or professional segments. While such segmentation may reduce retail access to some high‑risk instruments, policymakers argue that it is necessary to align crypto markets with investor‑protection standards applied elsewhere in the financial system.

Risks, Critiques, and Strategic Opportunities

MiCA has been widely praised as a landmark achievement in bringing legal clarity to crypto‑assets, but it has also attracted criticism from various quarters. One common concern is that the regulation is overly complex and burdensome for small or early‑stage projects. The need to produce exhaustive white papers, implement governance structures, and potentially secure authorization can be daunting for start‑ups that might otherwise have experimented with novel tokenomics or community‑driven models. Critics argue that this may concentrate activity among large incumbents with the resources to absorb compliance costs, potentially dampening innovation and diversity in the ecosystem.

Stablecoin provisions, particularly those constraining non‑EU currency tokens, are another flashpoint. Market participants worry that caps and potential restrictions on widely used foreign‑currency stablecoins could fragment liquidity and increase friction for cross‑border payments and DeFi interactions. For example, if dollar‑pegged stablecoins face tight usage limits in the EU, protocols and users may need to redesign their collateral and trading pairs around euro‑denominated tokens, which may initially be less liquid or widely accepted. Supporters of MiCA respond that promoting euro‑denominated digital money is a legitimate policy goal, and that a stable, well‑regulated base in euros is preferable to dependence on offshore dollar instruments. This trade‑off between market convenience and monetary sovereignty lies at the heart of many debates about MiCA’s long‑term impact.

Another area of criticism concerns MiCA’s treatment of DeFi and NFTs. Some stakeholders argue that by focusing predominantly on centralized intermediaries and asset‑backed tokens, MiCA fails to address the most novel aspects of Web3, leaving consumers exposed in areas such as on‑chain lending, perpetual derivatives, and NFT‑based financial products. Others caution that premature or heavy‑handed regulation of DeFi could stifle experimentation and drive protocols to more permissive jurisdictions, without necessarily improving outcomes for EU consumers who can still access global blockchains. The European Commission’s ongoing consultation on the functioning of EU crypto‑asset rules reflects awareness of these tensions and the need to calibrate any “MiCA 2” in light of practical experience.

Despite these critiques, MiCA also creates strategic opportunities. For compliant stablecoin issuers, the regulation offers the chance to become trusted providers of digital settlement assets across the EU’s enormous single market, including in contexts such as e‑commerce, remittances, and tokenized securities. For exchanges and custodians that succeed in securing CASP authorization and building credible compliance infrastructures, MiCA can serve as a badge of quality when courting institutional clients, corporates, and fintech partners. Token projects that invest early in high‑quality governance and disclosure may reap reputational benefits and broaden their investor base, particularly as more traditional financial institutions explore exposure to digital assets.

Policymakers, for their part, see MiCA as a way to integrate crypto into the EU’s existing financial architecture rather than allowing it to evolve as a completely parallel system. By subjecting key functions to familiar rules around disclosure, prudential soundness, and market abuse, MiCA aims to reduce the likelihood of crypto‑specific crises spilling over into the broader economy. EBA and ESMA’s monitoring of DeFi and other emergent trends suggests that supervisory attention will intensify in areas where risks appear most acute, even if formal regulation lags. The Commission’s structured review process and consultations indicate that the EU intends to update its approach iteratively, incorporating lessons from both successes and failures.

For the global crypto industry, MiCA represents both a challenge and a reference point. Firms that adapt successfully can showcase EU authorization as evidence of their ability to meet demanding regulatory standards, potentially easing their entry into other jurisdictions that take comfort from EU oversight. Conversely, those that fail to obtain licenses or comply with MiCA’s requirements may face a shrinking EU footprint or even lose access entirely if they cannot serve European clients after transitional periods expire. In this sense, MiCA is a powerful lever shaping the geography of crypto business and the competitive landscape among exchanges, stablecoin issuers, and infrastructure providers.

Conclusion

MiCA marks a decisive shift in the relationship between the European Union and the crypto‑asset ecosystem. By establishing a single, directly applicable regulatory framework for a wide range of tokens and service providers, the EU has moved from fragmented national approaches and legal uncertainty to a structured regime centered on consumer protection, financial stability, and market integrity. The regulation’s core pillars—stablecoin governance, CASP licensing, white‑paper disclosure, and market‑abuse rules—bring key elements of crypto activity into alignment with long‑standing standards in traditional finance, even as they grapple with genuinely novel features such as programmable money and decentralized governance.

For stablecoins, MiCA’s requirements around reserves, redemption, and asset backing fundamentally change what qualifies as a “stable” token in the EU, favoring regulated EMTs and ARTs over algorithmic or opaque designs. For CASPs, the shift from AMLD5 registration to full MiCA authorization demands significant investment in governance, risk management, and compliance, but it also opens the door to passported access across the bloc. Token issuers face more demanding white‑paper obligations and classification challenges, yet those who align early can leverage MiCA status as a sign of robustness in an increasingly discerning market.

At the same time, MiCA leaves important questions open, particularly around DeFi, NFTs, and the future of tokenization. EU institutions and national regulators are already engaging in consultations, discussion papers, and joint analyses to determine how, and to what extent, the framework should be extended or adjusted in light of practical experience. These processes, often grouped under the informal banner of “MiCA 2,” will determine whether the EU doubles down on its current focus on centralized intermediaries and asset‑backed tokens or moves toward more direct oversight of protocol‑level activity and on‑chain governance.

For crypto market participants, MiCA represents both a compliance challenge and a strategic opportunity. Firms that take the regulation seriously, invest in understanding its nuances, and design their products and operations with MiCA in mind are likely to be better positioned as the European market matures. Those that treat it as a peripheral concern risk finding themselves squeezed out of one of the world’s largest and most heavily regulated economic areas. As MiCA moves from text to practice, it will not only reshape crypto in Europe but also serve as a global reference point in the ongoing effort to integrate digital assets into the mainstream financial system.

Outlook

Looking ahead, the real test for MiCA will be in its implementation, enforcement, and adaptation. How consistently national authorities apply common standards, how quickly ESMA and the EBA refine guidance in response to market developments, and how effectively supervisors coordinate across borders will determine whether MiCA delivers its promise of both safety and innovation. The coming years will also reveal whether regulated euro‑denominated stablecoins and MiCA‑authorized CASPs can gain sufficient traction to anchor a vibrant, compliant crypto ecosystem in the EU, or whether liquidity and experimentation migrate to less regulated jurisdictions.

The European Commission’s post‑implementation review and consultations on the functioning of EU crypto‑asset rules will be pivotal in shaping any “MiCA 2” package, including potential extensions to DeFi, staking, and more complex tokenization models. Member‑state initiatives, such as Malta’s exploration of DeFi and DAOs and the resolution of legislative bottlenecks in countries like Poland, will further influence how uniform the “single rulebook” feels in practice. For now, MiCA stands as the most comprehensive attempt by a major jurisdiction to regulate crypto‑assets holistically, and its evolution will be closely watched by regulators, policymakers, and industry players worldwide.

Latest MiCA news

EU MiCA licenses near 230 before July 1 deadline as smaller crypto firms face shutdown pressureSpain's CNMV rules out MiCA deadline extensions as Binance and unlicensed crypto firms face July 1 exitOpenPayd secures MiCA licence to offer regulated stablecoin rails across EEA Ripple gets preliminary Luxembourg MiCA nod as 30-country EEA payments passport still needs clearance

Ripple gets preliminary Luxembourg MiCA nod as 30-country EEA payments passport still needs clearanceSources

- https://www.esma.europa.eu/esmas-activities/digital-finance-and-innovation/markets-crypto-assets-regulation-mica

- https://assets.kpmg.com/content/dam/kpmg/cy/pdf/2025/markets-in-crypto-assets-regulation-mica.pdf

- https://www.21analytics.co/blog/stablecoins-in-the-eu/

- https://www.cyfrin.io/blog/mica-regulation-explained-a-guide-to-eu-crypto-compliance

- https://www.afg.asso.fr/app/uploads/2024/05/afg-response-to-esma-consultation-paper-on-the-qualification-of-crypto-assets-as-financial-instruments.pdf

- https://notabene.id/post/is-mica-2-coming-what-the-eus-2026-consultation-means-for-stablecoins-casps-and-defi

- https://x.com/vechainofficial/status/1977675639269576722

- https://x.com/crynetio/status/2068146954761081034

- https://watsonlaw.nl/en/mica-timeline/

- https://www.facebook.com/CoinMarketCap/posts/latest-bitgo-europe-launched-a-mica-ready-crypto-as-a-service-platform-letting-e/1428488425975213/

- https://www.binance.com/en/square/post/335052446892258

- https://www.tradingview.com/news/newsbtc:fa83d2afb094b:0-malta-regulator-opens-defi-consultation-as-dao-governance-enters-policy-spotlight/

- https://wozniaklegal.com/en/news-and-insight/492/polands-crypto-future-second-mica-veto-sparks-uncertainty.html

- https://sumsub.com/blog/crypto-regulations-in-the-european-union-markets-in-crypto-assets-mica/

- https://www.afm.nl/en/sector/cryptopartijen/toezicht/white-papers

- https://www.circle.com/circle-eea

- https://www.esma.europa.eu/press-news/esma-news/eba-and-esma-analyse-recent-developments-crypto-assets

- https://finance.ec.europa.eu/news/commission-seeks-feedback-functioning-eu-crypto-assets-rules-2026-05-20_en

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…