In‑depth explainer on how the U.S. SEC regulates crypto, from tokenized securities and ETFs to DeFi, staking, and Reg NMS reforms, and what its evolving partnership with the CFTC means for builders and investors.

+98 sources across the wider coverage universe

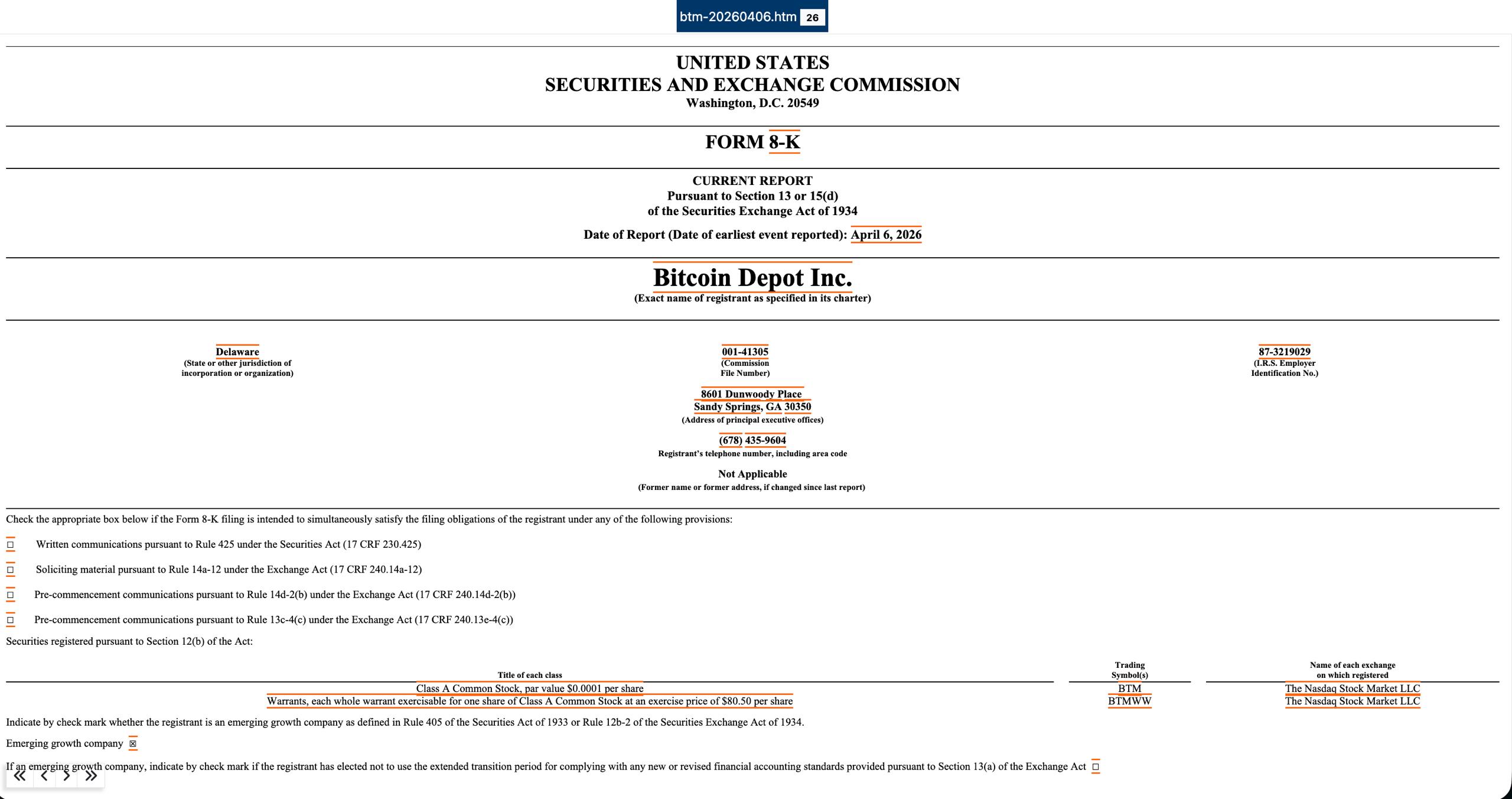

Bitcoin Depot discloses $3.6M BTC theft from corporate wallets in SEC filing, two weeks after breach2026-04

Bitcoin Depot discloses $3.6M BTC theft from corporate wallets in SEC filing, two weeks after breach2026-04 Former SEC Chief Economist backs a16z-backed safe harbor, arguing tokenized securities on DeFi can cut costs, enable 24/7 markets, and boost transparency despite regulatory tradeoffs2026-04

Former SEC Chief Economist backs a16z-backed safe harbor, arguing tokenized securities on DeFi can cut costs, enable 24/7 markets, and boost transparency despite regulatory tradeoffs2026-04 Securitize appoints former SEC and JPMorgan executive Brett Redfearn as president and board member, strengthening leadership as tokenization and digital asset markets expand2026-04

Securitize appoints former SEC and JPMorgan executive Brett Redfearn as president and board member, strengthening leadership as tokenization and digital asset markets expand2026-04 SEC axes $25,000 pattern day trader minimum after 25 years, FINRA pivots to risk-based intraday margin2026-04

SEC axes $25,000 pattern day trader minimum after 25 years, FINRA pivots to risk-based intraday margin2026-04 SEC staff addresses broker-dealer registration requirements for crypto transaction interfaces2026-04

SEC staff addresses broker-dealer registration requirements for crypto transaction interfaces2026-04 Ondo Finance requests SEC no-action letter to record tokenized securities on Ethereum2026-04

Ondo Finance requests SEC no-action letter to record tokenized securities on Ethereum2026-04

The SEC and Crypto: How U.S. Securities Regulation Shapes Digital Assets

The U.S. Securities and Exchange Commission, or SEC, is the federal agency that polices securities markets, and it now sits at the center of how crypto assets, tokenized securities, and digital-asset markets are allowed to operate in the United States. As crypto matures into a mainstream asset class touching everything from bitcoin ETFs to tokenized U.S. stocks and real‑world assets, understanding what the SEC is, what it considers a “security,” and how it shares power with the CFTC has become essential for exchanges, builders, and investors alike.

In the last several years, the SEC has moved from ad‑hoc enforcement toward a more structured framework for digital assets, including a formal taxonomy for different types of crypto assets and detailed guidance on how federal securities laws apply to airdrops, protocol mining, staking, and token wrapping. At the same time, the agency is working with the Commodity Futures Trading Commission (CFTC) and Congress, through efforts such as the Clarity Act and related legislative proposals, to draw clearer jurisdictional lines between securities, commodities, and stablecoins. The SEC has also begun to embrace tokenization of traditional securities, approving rule changes that allow tokenized shares to trade on major exchanges and making clear that a security does not cease to be a security simply because it lives on a blockchain. Market‑structure reforms, including a proposal to scrap key pieces of Regulation NMS, are being framed by analysts as a potential unlock for tokenized U.S. stocks and DeFi‑style liquidity models inside the regulated securities world. Against this backdrop, large players such as Coinbase, T. Rowe Price, NYSE, and Securitize are building products—from crypto ETFs to SEC‑registered AI advisors and tokenized stock platforms—that depend on how the SEC ultimately answers the question at the heart of crypto’s future: when is a token a security, and what should a digital securities market look like?

What the SEC Is — And Why Crypto Cares

The SEC is an independent U.S. federal agency charged with three core objectives: protecting investors, maintaining fair, orderly, and efficient markets, and facilitating capital formation in the securities markets. In practice, this means the SEC writes and enforces rules governing public companies, stock exchanges, brokers, investment advisers, and investment funds, and it interprets how long‑standing securities statutes apply to new technologies such as blockchains and crypto tokens. For crypto, the SEC matters because the moment a token, derivative, or platform is deemed to involve a security, the entire regime of registration, disclosure, trading, and anti‑fraud rules under federal securities law becomes relevant.

Legally, the SEC’s jurisdiction is tied to the definition of “security” under the Securities Act and the Exchange Act, a list that includes familiar instruments such as stocks and bonds but also more flexible categories like “investment contracts.” Courts have long interpreted “investment contracts” through the Howey test, which asks whether people are investing money in a common enterprise with an expectation of profits derived from the efforts of others. When the SEC alleges that a crypto token is an unregistered security, it is usually arguing that the token sale or ongoing scheme fits this investment‑contract framework, even if the token also has network utility or other functions. This approach is visible in the SEC’s recent interpretive release, which tries to distinguish between a crypto asset as a thing and the investment contract or scheme in which that asset might be embedded.

Crypto’s complexity has forced the SEC to clarify that not all tokens are the same and that the same token can fall inside or outside securities law depending on context. In its 2026 interpretation, the Commission laid out a coherent taxonomy of crypto assets, referring to categories such as digital commodities, digital collectibles, digital tools, stablecoins, and digital securities, and explaining when each might be implicated by an investment contract. That document introduced the concept of a “non‑security crypto asset”—for example, a digital commodity or tool—that can nevertheless be part of a securities offering if it is sold under an investment contract, and then fall out of that status if the contractual scheme winds down and the asset trades independently. This move reflects a growing recognition inside the SEC that not every tokenized instrument should be presumed to be a security forever, even if at launch it was sold in a securities transaction.

For the crypto industry, this nuance is both opportunity and risk. It opens the door for projects to argue that their networks have evolved beyond “active investment contracts,” an idea reflected in public remarks suggesting that many tokens no longer seem to be part of live investment schemes, even if the SEC retains anti‑fraud authority over securities. At the same time, it gives the Commission a flexible tool: it can scrutinize how tokens are distributed, marketed, and supported and decide, often case‑by‑case, whether a particular project sits inside securities law even if tokens look similar across projects. This duality is why crypto lawyers obsess over the SEC’s interpretive guidance and speeches; the agency’s view of what counts as a security effectively determines which parts of the crypto universe must register, which can operate under exemptions, and which can credibly argue they fall outside SEC jurisdiction.

Bitcoin Depot discloses $3.6M BTC theft from corporate wallets in SEC filing, two weeks after breach

Readers click SEC stories not for enforcement outcomes but for power-map clarity — they want to know who controls the definition of 'security,' because that answer determines whether every exchange, ETF, and token they hold is legal.↗

The SEC’s Evolving View of Crypto Assets

The latest SEC interpretation on crypto assets marks a significant shift from earlier years when the agency relied mostly on enforcement actions and staff speeches to signal its expectations. In that release, the Commission set out a taxonomy that separates digital commodities (for example, crypto assets whose primary function is as a store of value or medium of exchange), digital collectibles, digital tools (tokens that mainly provide access or utility within a protocol), stablecoins, and digital securities. The goal was to give market participants a framework for thinking about when federal securities laws apply and when they do not, while acknowledging that classification is not solely about the token’s label but about the transactional context and economic reality.

A striking feature of the interpretation is its focus on the concept of a “non‑security crypto asset” that can be associated with an investment contract at some times and not at others. The SEC explains that a crypto asset that is not itself a security can become subject to securities law if it is part of an investment scheme meeting the Howey criteria, for example via a fundraising token sale where purchasers reasonably expect the promoter’s efforts to raise the token’s value. Conversely, the Commission suggests that once the contractual promises and entrepreneurial efforts that underpinned that investment contract have dissipated, a token could cease to be part of a securities arrangement, even though it continues to exist and trade, potentially as a commodity or digital tool. This distinction between the asset and the contract is central to current debates about when networks become “sufficiently decentralized” and whether tokens can transition out of securities status over time.

The same interpretation also addresses a range of distribution mechanisms that are core to crypto: airdrops, protocol mining, protocol staking, and the wrapping of non‑security crypto assets. Airdrops, which distribute tokens for free or for performing tasks, are analyzed in terms of whether recipients are still investing “money” or other tangible value such as time, data, or promotional services in a common enterprise in expectation of profit; if so, they may still be subject to securities rules even without a cash payment. Protocol mining and staking—where participants provide computing or capital to support a network and receive token rewards—are evaluated based on whether they reflect entrepreneurial efforts by others or whether they are closer to user‑driven activity that does not create an investment contract. Public guidance has indicated that many forms of proof‑of‑work and proof‑of‑stake mining, including delegated proof‑of‑stake setups, are not viewed as core SEC jurisdictional targets when participants are simply running open‑source software or providing validation services rather than investing in a promoter‑led scheme.

Wrapping non‑security crypto assets, such as issuing a tokenized representation of bitcoin or another asset, raises its own securities questions. The SEC’s interpretation clarifies that a wrapped token can become a security if the wrapper structure creates a new claim, pooling arrangement, or expectation of profit based on the wrapper sponsor’s efforts, even if the underlying asset is not a security. For example, if a centralized entity issues wrapped tokens representing a non‑security asset and uses reserves flexibly to generate yield for tokenholders based on its trading or lending activities, that arrangement may be an investment contract subject to securities regulation. By contrast, a purely technical wrapper that is transparent, fully collateralized, and not bundled with profit‑seeking promises is more likely to be treated as a digital tool rather than a security, though the SEC emphasizes that each structure must be assessed individually.

These clarifications align with a broader change in tone from the SEC and other policymakers as they try to move from an enforcement‑only stance to a “road to clarity” for U.S. digital assets. In public discussions of Project Crypto and the Clarity Act, participants have described how regulators are trying to build a more comprehensive framework, including by formalizing dual reporting obligations and expanding supervisory reach over exchanges, custodians, and wallet providers in a way that reflects the multi‑asset nature of modern platforms. Some of these conversations have highlighted that meme coins, certain proof‑of‑work and proof‑of‑stake mining activities, and other purely speculative or participatory behaviors may not fit neatly into SEC jurisdiction, even as the agency retains authority to police fraud where the underlying instruments are securities. The resulting landscape is uneven but moving toward greater differentiation between the many use cases and technical models that fall under the broad label of “crypto.”

SEC, CFTC, and the End of the Turf Wars?

No explanation of the SEC’s role in crypto is complete without the CFTC. While the SEC oversees securities markets, the Commodity Futures Trading Commission regulates futures, options, and swaps on commodities, as well as holding anti‑fraud and anti‑manipulation authority over spot commodity markets, including many crypto assets that are not securities. In practice, this means that bitcoin and ether spot trading on crypto exchanges fall mainly under state money transmission and general consumer‑protection rules, with the CFTC stepping in when there is manipulation, while derivatives referencing bitcoin, ether, or other digital assets may fall under CFTC or SEC jurisdiction depending on whether they are considered “swaps,” “security‑based swaps,” or futures. This split in authority has fueled a long‑running turf war over who regulates what in crypto.

Recent developments suggest that turf war may be giving way to more coordinated rule‑making. The Clarity Act and related legislative efforts have been discussed as drawing clearer lines between the SEC and CFTC, while also establishing an explicit right for Americans to self‑custody digital assets and directing both agencies to engage in joint rulemaking on topics where their remits overlap. Public conversations around the Clarity Act describe how it delegates significant responsibility to both regulators and expects them to cooperate on standards for exchanges, custodians, and on‑chain market infrastructure, instead of leaving market participants to guess which agency might appear at any given time. At the same time, new legislation such as the so‑called Genius Act has reportedly carved certain stablecoins out from the CFTC’s definition of “commodity,” signaling that Congress is willing to draw asset‑specific boundaries rather than relying solely on decades‑old statutory language.

A key flashpoint in the SEC‑CFTC relationship is the classification of perpetual futures and similar derivative instruments tied to crypto assets. In a joint request for comment, the two agencies have asked the public to weigh in on how to define “swaps” and “security‑based swaps,” including in the context of perpetual derivatives on digital assets. This consultation is unfolding against the backdrop of a lawsuit by CME Group challenging aspects of the CFTC’s approach to classifying certain perpetual contracts, illustrating how even traditional derivatives giants see regulatory uncertainty around crypto products as a material business risk. At the same time, the CFTC has begun bringing perpetual futures onshore: Bitnomial Exchange became the first CFTC‑registered designated contract market to self‑certify a perpetual futures contract under the agency’s Regulation 40.2, showing that with the right design, crypto perps can fit within existing futures frameworks.

Prediction markets add another layer of complexity. As new platforms let users trade contracts on elections, sports results, and other real‑world events, regulators are wrestling with whether these should be treated as swaps or left to state gambling regulators. In a detailed comment letter, the Maryland Attorney General argued that sports bets are not derivatives subject to the CFTC’s oversight and urged the agency to make clear in rulemaking that states can continue to regulate sports wagering without federal derivatives law intruding. Former SEC and CFTC leaders have echoed the idea that federal commodities law does not displace state gambling rules, even as they warn that some complex prediction contracts might mimic swaps and require federal oversight. This debate matters for crypto because many prediction markets are built on public blockchains, and the classification of their contracts will determine whether they fall under CFTC rules, state gambling regimes, or some hybrid.

Amid all this, the SEC has signaled a desire to move beyond an “enforcement first” posture and toward coordinated frameworks. Jamie Selway, Director of the SEC’s Division of Trading and Markets, has described how the Commission is working hand‑in‑hand with the CFTC on a unified regulatory framework for tokenized securities, perpetual futures, and digital‑asset trading infrastructure under the leadership of SEC Chair Paul Atkins. Selway framed “innovation without arbitrage” as the guiding principle, meaning regulators are trying to avoid a world where firms can game jurisdictional differences, while still allowing legitimate cross‑border and cross‑asset innovation. His remarks suggest that U.S. regulators recognize the need to treat crypto trading platforms as multi‑product venues—dealing in spot commodities, securities, and derivatives—rather than forcing artificial separation that no longer reflects how markets actually function.

The relationship between the SEC and CFTC can be summarized along a few key dimensions:

| Regulator | Core domain | Typical crypto exposure | Key tools |

|---|---|---|---|

| SEC | Securities (stocks, bonds, investment contracts, security‑based swaps) | Tokenized securities, many token launches, tokenized ETFs, security‑based swaps on digital assets | Registration, disclosure rules, exchange and broker‑dealer rules, anti‑fraud enforcement |

| CFTC | Commodities and derivatives (futures, options, swaps) | Bitcoin and other non‑security tokens as commodities; futures and perps on digital assets | Market‑designation rules, self‑certification of futures, anti‑fraud/manipulation authority in spot markets |

For builders and exchanges, the practical upshot is that a single platform might need to navigate both regimes, plus state money‑transmission rules and banking regulation, depending on which products it lists and how it structures them. That is why the Clarity Act, joint SEC‑CFTC comment processes, and guidance on stablecoins and perps are followed so closely: they offer the first real chance to replace turf battles with a coherent division of labor.

Former SEC Chief Economist backs a16z-backed safe harbor, arguing tokenized securities on DeFi can cut costs, enable 24/7 markets, and boost transparency despite regulatory tradeoffs

Lewis's 40-60% bond cost reduction math checks out, but Citadel is simultaneously lobbying the SEC to classify validators and wallet providers as broker-dealers — which would reimpose the exact intermediary overhead tokenization is supposed to eliminate. $946M total tokenized equity market vs $607B daily TradFi volume means incumbents still have time to shape those definitions before scale arrives. Nasdaq already tipped its hand with an equity token design that explicitly preserves existing registries and exchanges.

- 01Trump deregulation pivot↗

The reassignment of 50+ SEC lawyers and Uyeda's appointment signaled a regime change readers needed to understand to reprice regulatory risk across their portfolios.

- 02Bitcoin and Ethereum ETF race

Each filing, delay, and seed-funding disclosure was a checkpoint in a years-long bet on whether institutions would get regulated on-ramps — readers tracked every move.

- 03Coinbase as industry proxy↗

Coinbase's simultaneous battles — SEC lawsuit, shareholder suit, FDIC suit, and CEO media campaign — made it the clearest lens on whether the industry could survive a full enforcement cycle.

- 04Exchange enforcement responses

Binance's and Kraken's public rebuttals reframed SEC actions as jurisdictional overreach rather than legitimate enforcement, a narrative readers actively chose over neutral reporting.

- 05Fraud and market manipulation charges

SEC actions against fake market makers, Ponzi operators, and Terraform gave readers validation that bad actors were being caught while surfacing how rigged retail conditions already were.

- 06SEC jurisdiction boundary fights↗

Texas lawsuit claims, Binance's 'unilateral definition' framing, and Warren's conflict-of-interest probe all fed reader appetite for who actually has the legal authority to regulate crypto.

Tokenized Securities, ETFs, and Market Structure Reform

If the early crypto story was about native tokens like bitcoin, the current phase is increasingly about tokenized securities—traditional stocks, bonds, and funds represented as crypto assets on distributed ledgers. The SEC has made its core position clear: an issuer may tokenize a security by issuing it in the format of a crypto asset, but that tokenized instrument remains a security and is subject to the same securities laws as its non‑tokenized counterpart. In official guidance, the Commission explains that tokenization typically involves integrating distributed ledger technology into a security’s lifecycle, from issuance and record‑keeping to trading and settlement, without changing the underlying rights and obligations. This means that whether a share is recorded in a conventional registry or as a token on a blockchain, it carries the same shareholder rights, must comply with the same disclosure regime, and is overseen by the same regulators.

Congress and the SEC have reinforced this principle. In a House Financial Services Committee hearing on tokenization and the future of securities, witnesses noted that the SEC has provided helpful definitional clarity stating that a tokenized security is still a security and that regulatory outcomes should not change merely because a security is issued, recorded, or transferred using distributed ledger technology. The Senate’s Clarity Act has likewise been described as embedding the principle that a security does not stop being a security simply because it moves onto a blockchain. Building on that foundation, the SEC recently approved Nasdaq’s proposal to allow securities to trade either in traditional electronic form or in tokenized form on its markets, with tokenized shares remaining fungible with their traditional counterparts, sharing the same identifiers, and conferring the same rights. The program is initially limited in scope and duration, but it signals that tokenization is moving from concept to live infrastructure on major national securities exchanges.

Private actors are racing to build the plumbing to support this shift. The New York Stock Exchange and Securitize, a leading tokenization platform and SEC‑registered transfer agent, signed a memorandum of understanding to explore how to support tokenized securities across listing, transfer, and trading functions. The initiative draws on Securitize’s experience tokenizing private and public assets and aims to help define listing and trading models for tokenized securities within the NYSE’s regulatory framework. At the same time, Securitize is pursuing a SPAC merger with Cantor Equity Partners II, with plans for the combined company to list on the NYSE under the ticker SECZ, creating a publicly traded, SEC‑regulated tokenization specialist embedded inside the traditional capital‑markets ecosystem. Together, these moves suggest that tokenization is no longer confined to startup experiments; it is being adopted by the core institutions of U.S. equity markets.

Exchange‑traded funds (ETFs) are another arena where the SEC’s decisions are reshaping the crypto landscape. After years of debate, the Commission has begun approving a growing suite of crypto‑related ETFs, including both spot and futures‑based products, recognizing that the ETF wrapper can provide a regulated, exchange‑listed way for investors to gain exposure to crypto assets. A recent example is the T. Rowe Price Active Crypto ETF, whose registration filing describes an investment objective of seeking long‑term capital growth through investments in crypto assets and identifies NYSE Arca as its listing exchange. The SEC approved NYSE Arca’s rule change to list and trade the fund, signaling that actively managed crypto strategies can fit within the ETF framework so long as they comply with existing fund and exchange rules. This endorsement is significant because it opens the door for more specialized crypto ETFs, including those focused on particular themes or staking strategies, so long as sponsors can demonstrate robust risk management and compliance.

At the same time, large crypto‑native firms are pushing deeper into SEC‑regulated territory. Coinbase, for example, has launched an SEC‑registered, AI‑powered investment advisor—Coinbase Advisor—aimed at delivering professional financial guidance, including on crypto exposures, to a mass‑market audience. The product is presented as one of the world’s first SEC‑registered AI advisors, integrating market news, ideas, and opportunities into personalized investment strategies while operating under the SEC’s investment‑adviser rules. In parallel, Coinbase has outlined a broader “system update” that includes stock options trading, pre‑IPO perpetual contracts offered via its Bermuda platform, unified global liquidity across products, and support for tokenized stocks, positioning itself as a potential “everything exchange” that straddles the line between traditional securities and digital assets. Each of these offerings requires carefully navigating SEC jurisdiction and demonstrates how crypto platforms are increasingly willing to operate inside securities law rather than outside it.

While tokenization and crypto ETFs expand what can trade, the SEC is also rethinking how securities should trade. One of its most consequential recent proposals is to rescind Rule 611 of Regulation NMS, which contains the “trade‑through” prohibition for national market system stocks, and Rule 610(e), which restricts locking and crossing quotations. Rule 611 requires trading centers to avoid executing trades at prices worse than those publicly displayed on other venues, effectively enforcing a national best bid and offer, while Rule 610(e) aims to prevent markets from displaying locked or crossed quotes that could confuse investors. The SEC’s proposal would repeal these rules, eliminate related definitions, and make conforming changes elsewhere, while moving toward a more flexible “best execution” framework that may rely more on broker‑dealer duties and less on rigid intermarket price priority.

Analysts such as Galaxy Digital have argued that scrapping Rule 611 could be a major positive for tokenized U.S. stocks and DeFi‑style market makers. By loosening the strict trade‑through prohibition, the SEC could make it easier for alternative trading systems and automated market makers—including on‑chain liquidity pools—to quote and execute tokenized versions of U.S. equities without being forced to route every order to centralized exchanges to comply with NMS benchmarks. Reporting has suggested that the agency is likely to replace Rules 611 and 610(e) with a best‑execution standard that might accommodate automated market makers so long as they can demonstrate that they provide competitive, fair pricing for investors. Bloomberg noted that the proposal could have a “clear winner” in crypto‑linked trading venues and tokenization platforms, which have long struggled to reconcile continuous on‑chain pricing with the fragmented, rule‑bound world of U.S. equity markets. If adopted, these reforms could open the door for DeFi market makers to provide liquidity in tokenized U.S. stocks at scale, under SEC supervision but with a market structure closer to crypto’s native environment.

Airdrops, Staking, DeFi, and the Edges of SEC Authority

Beyond ETFs and tokenized blue‑chip stocks, the SEC’s decisions on airdrops, staking, and decentralized finance (DeFi) will profoundly shape the crypto ecosystem. The Commission’s recent interpretive release dedicates significant attention to airdrops, recognizing that many projects distribute tokens for free to attract users, reward early adopters, or decentralize governance. The key question is whether such distributions involve an “investment of money” and whether recipients reasonably expect profits based on the efforts of a promoter or third party. The SEC suggests that even when no fiat changes hands, recipients may provide value—such as personal data, promotional services, or economic opportunity cost—that satisfies the “investment” prong of Howey, and that marketing emphasizing potential token price appreciation can bolster the case for an “expectation of profits.” This means that in some circumstances, airdrops can be securities offerings subject to registration or exemption requirements, even though they do not look like traditional capital raises.

Staking and protocol “mining” present equally thorny questions. In proof‑of‑stake networks, users lock up tokens and sometimes delegate validation rights to validators in exchange for staking rewards, blurring the line between infrastructure participation and investment income. The SEC’s guidance distinguishes between “protocol staking” where participants directly run open‑source software and secure the network and “staking‑as‑a‑service” arrangements where an intermediary pools user funds and markets a yield. Remarks in the Road to Clarity discussion have highlighted that various forms of mining and delegated proof‑of‑stake activity have been the subject of guidance indicating they are not central to SEC jurisdiction when participants are simply engaging in network operations rather than investing in a promoter’s enterprise. However, when a platform offers staking programs with contractual promises, pooled management, and heavy marketing around expected returns, the SEC is more likely to view them as investment contracts, as evidenced by enforcement actions in prior years and reinforced by the logic of its interpretive release.

DeFi complicates this analysis by removing—or at least obscuring—the role of a central promoter. Automated market makers, lending protocols, and synthetic‑asset platforms run on smart contracts that anyone can interact with, often governed by dispersed tokenholder votes. The SEC’s new taxonomy includes digital tools, which can cover governance and utility tokens that primarily provide access or functional rights within a protocol. However, the Commission emphasizes that labeling a token as a “governance” or “utility” instrument is not determinative; if tokens are marketed and sold with a strong emphasis on profit and rely on identifiable teams building and promoting the protocol, they may still be wrapped in an investment contract. By contrast, projects that are fully deployed, with no ongoing managerial efforts by a specific group and no fundraising sales, may plausibly argue that their tokens function as non‑security digital tools, even if they trade in secondary markets.

A related area is self‑custody and the extent to which individuals can hold and use their digital assets without intermediaries falling under SEC rules. The Clarity Act has been described as establishing a statutory right to self‑custody digital assets, an “extraordinary” step in the eyes of some commentators, which underscores Congress’s intent to preserve the open‑network ethos of crypto even as it tightens regulation of centralized platforms. At the same time, the Act and related legislative proposals delegate significant rulemaking authority to the SEC and CFTC, expecting them to set standards for exchanges, custodians, and wallet providers in areas such as dual reporting, risk management, and market integrity. This hybrid approach reflects a political compromise: individuals should be allowed to self‑custody and use digital assets peer‑to‑peer, but once those assets enter the realm of organized trading, pooled investment, or professional custody, they are likely to encounter securities and derivatives law.

The SEC has also clarified that its fraud and manipulation authority is not limitless. Public remarks have noted that the Commission retains fraud jurisdiction only where the underlying asset is a security; if a token is purely a commodity outside an ongoing investment contract, the SEC must rely on other agencies or general law enforcement to tackle fraud, while the CFTC may use its anti‑fraud and anti‑manipulation powers in commodity markets. This calibration is particularly important for meme coins and purely speculative tokens, which may cause real investor harm but do not always fit cleanly into the securities framework. The Commission’s recent taxonomy and guidance, combined with the Clarity Act’s carve‑outs, suggest that many such tokens will be overseen primarily through consumer‑protection and commodity‑market tools rather than full‑blown securities regulation, even as securities laws continue to apply to tokenized stocks, crypto ETFs, and various yield‑bearing products.

Securitize appoints former SEC and JPMorgan executive Brett Redfearn as president and board member, strengthening leadership as tokenization and digital asset markets expand

Redfearn ran the SEC's Division of Trading and Markets from 2017-2020 — the exact office that governs ATS and NMS frameworks for how securities actually trade in the US. Securitize is bringing him on right as they're filing to go public via Cantor SPAC at a $1.25B valuation, projecting $9B AUM by year-end (up from ~$4B now). With BUIDL already near $3B and live on UniswapX, they need someone who's sat across the table from the SEC when these tokenized fund structures inevitably get scrutinized at scale.

- 2023-06regulatory

SEC charges Coinbase and Binance on same week

- 2023-09regulatory

SEC subpoenas three crypto VC firms

- 2023-10regulatory

Friend.tech renames shares to keys amid SEC radar reports

- 2024-01milestone

SEC approves spot Bitcoin ETFs; hacked SEC account triggers false early announcement

- 2024-08regulatory

Judge fines Ripple $125M, prohibits future securities violations

- 2025-01governance

Gary Gensler resigns; Trump appoints pro-crypto Mark Uyeda as acting SEC Chair

SEC reassigns 50+ crypto enforcement lawyers, signals deregulatory pivot

SEC publishes clarification on federal securities law application to crypto assets

Global Context: The Philippine SEC and Tokenization Abroad

The U.S. SEC is not the only regulator grappling with crypto and tokenization, and global developments can influence how American policymakers think about the trade‑offs between innovation and investor protection. A notable example is the Philippine Securities and Exchange Commission, which shares a name but is a separate national regulator from the U.S. SEC. In recent speeches, Philippine SEC Commissioner Rogelio Quevedo has declared that the country is ready to accommodate the tokenization of real‑world assets (RWAs), arguing that existing Philippine laws and regulatory frameworks are sufficient to support tokenized assets and related investment products. Speaking at Philippine Blockchain Week 2026, he said the regulator is “now fully convinced” that the legal groundwork for asset tokenization is in place, positioning the Philippines as an early mover in formalizing RWA markets.

The Philippine SEC has reinforced this message through its Strategic Sandbox, a program that admits firms to test novel financial products under regulatory supervision. In late 2025, the agency disclosed that four companies had been admitted to the sandbox, including one testing a tokenized real‑estate offering and two others evaluating products designed to provide access to U.S. equities via tokenized structures. These pilots show how tokenization can be used both to fractionalize local assets, such as property, and to provide domestic investors with exposure to foreign securities in a controlled manner. The regulator has emphasized that these experiments operate under existing laws, which already cover securities offerings and trading, underscoring its view that tokenization does not require a wholesale rewrite of financial statutes.

At the same time, Philippine authorities are tightening oversight of crypto intermediaries. The country’s central bank, Bangko Sentral ng Pilipinas, has introduced stricter requirements for virtual asset service providers, requiring more extensive due‑diligence procedures before listing cryptocurrencies for customers. These measures aim to mitigate risks such as money laundering, fraud, and speculative excess, even as the Philippine SEC embraces tokenization as a potential catalyst for capital‑market innovation and financial inclusion. Commissioner Quevedo has framed tokenized assets as a way to lower barriers to investment and improve transparency while insisting that robust investor protection remains non‑negotiable.

For a crypto audience focused on the U.S., the Philippine example illustrates two important dynamics. First, multiple jurisdictions are converging on the idea that tokenized assets can largely be governed by existing securities and investment‑product laws, with tokenization treated as a technological upgrade rather than a new asset class. This mirrors the U.S. SEC’s stance that tokenized securities are still securities and should not benefit from regulatory arbitrage merely because they trade on blockchains. Second, sandbox approaches allow regulators to learn alongside industry, adjusting rules as they observe real‑world experiments in tokenized real estate, equity access products, and other RWAs. As the U.S. considers how to structure its own sandboxes and pilot programs, particularly around tokenized stocks and bond markets on venues such as Nasdaq and NYSE, it can draw lessons from how peers like the Philippine SEC balance openness with caution.

Global developments also create pressure for coherence. If jurisdictions like the Philippines, Europe, or Singapore adopt clear, permissive frameworks for tokenized securities and RWAs, U.S. policymakers face a strategic choice: align with global standards to keep capital‑markets leadership or risk seeing tokenization activity migrate abroad. The SEC’s moves—approving tokenized trading on major exchanges, working with platforms like Securitize, and exploring tokenization exemptions that can move faster than full rulemaking—suggest it is aware of this competitive dynamic. At the same time, American regulators are more constrained by complex federal statutes and the SEC‑CFTC split than many of their foreign counterparts, which may explain why progress in the U.S. often takes the form of incremental interpretations, exemptive relief, and pilot programs rather than wholesale new regimes.

How the SEC Shapes Crypto Businesses and Investors

For crypto businesses and investors, the SEC is not an abstract institution; it directly influences which products can be offered, how they can be marketed, where they can trade, and who can access them. Exchanges that list tokenized securities or crypto ETFs must register as national securities exchanges or alternative trading systems and comply with detailed rules on surveillance, best execution, capital, and customer protection. Broker‑dealers and investment advisers that recommend such products must follow suitability and fiduciary standards, file disclosure documents, and submit to examinations and enforcement risk. When Coinbase launched its SEC‑registered AI‑powered investment advisor, it did so by entering the world of registered investment advisers, promising to convert market news and ideas into tailored portfolios while operating under the SEC’s oversight. This strategy marks a shift from a purely unregulated crypto brokerage to a hybrid model where at least part of its business sits inside the traditional securities perimeter.

Investors experience the SEC primarily through the products that are available to them. A U.S. retail investor can now buy shares of a regulated crypto ETF on a securities exchange, gaining exposure to bitcoin or diversified crypto baskets without opening accounts on offshore exchanges or self‑custodying tokens. As tokenized securities develop, that same investor might be able to hold tokenized versions of U.S. stocks or RWAs in a standard brokerage account, with all the familiar protections of securities law—such as quarterly reporting, insider‑trading rules, and orderly‑market obligations—while reaping some benefits of blockchain settlement and programmability. On the other hand, the SEC’s cautious stance means that many DeFi tokens, yield‑bearing instruments, and unregistered offerings are either unavailable to U.S. investors or offered through compliance‑heavy structures that limit participation to accredited or institutional buyers. For better or worse, the SEC acts as a gatekeeper for which parts of the global crypto universe become mainstream investments.

Market structure is another lever through which the SEC shapes outcomes. The proposal to rescind Regulation NMS Rules 611 and 610(e) could radically alter how tokenized U.S. stocks and other securities trade if it leads to a regime where DeFi‑style automated market makers can operate within best‑execution principles. Analysts have suggested that such a change could “open the floodgates” for DeFi market makers to provide liquidity in tokenized U.S. equities, enabling 24/7, on‑chain trading that is still tied into the national market system. If combined with Nasdaq’s tokenized‑trading program and the NYSE‑Securitize initiative, this could usher in a future where core U.S. securities trade seamlessly between conventional and on‑chain venues, all under SEC supervision. In this world, the distinction between “crypto” and “securities” might recede, replaced by a continuum of instruments differentiated more by their risk profiles and rights than by their underlying settlement rails.

For builders, the SEC’s evolving guidance offers both constraints and design targets. Knowing that tokenized securities remain securities and that airdrops, staking programs, and wrapped tokens can become investment contracts, sophisticated teams now design tokenomics and launch strategies around regulatory touchpoints. Some may structure early fundraising as registered or exempt securities offerings, with a path for their tokens to transition into non‑security status once networks are sufficiently decentralized, aligning with the SEC’s distinction between the asset and the investment contract. Others may focus purely on digital tools and commodities, avoiding fundraising tied to token speculation and emphasizing user utility to minimize securities exposure. Still others choose to operate fully under securities law from day one, building tokenized funds, bonds, or equity instruments with clear investor‑protection safeguards and SEC registrations. In all cases, understanding the SEC’s latest interpretations is a competitive advantage.

Finally, the SEC’s coordination with other regulators shapes the broader environment. Its work with the CFTC on swap definitions and perpetual futures will determine whether certain derivative products fall under SEC or CFTC rules, affecting margin requirements, trading venues, and customer protections. Its interaction with state regulators, such as in debates over prediction markets and gambling law, influences which crypto‑based betting or forecasting platforms can operate legally. And its engagement with foreign regulators, whether through formal colleges or informal dialogues, affects how cross‑border tokenization and trading projects are structured. For the crypto industry, the SEC is thus both a national regulator and a node in a global network of policymakers whose decisions collectively determine how, and where, digital‑asset innovation can flourish.

Securities classification remains legally unsettled — courts, Congress, and the SEC itself are in active conflict over which tokens and platforms fall under federal securities law.

- MarketHigh

ETF approvals and enforcement actions have historically triggered immediate price swings, and the SEC's hacked-account false-approval incident demonstrated how fragile market reactions to SEC signals can be.

- CentralizationMedium

Enforcement has concentrated on major centralized exchanges (Coinbase, Binance, Kraken) and large VC networks, leaving DeFi protocols in a legally ambiguous but comparatively less targeted position.

- LiquidityMedium

eToro's removal of SEC-deemed securities tokens and platform chilling effects on VC investment demonstrate that enforcement credibly reduces tradable asset pools and early-stage capital flows.

- Counterparty / FraudHigh

SEC's own warning that 'the deck may be stacked against' retail crypto investors — alongside charges against fake market makers and a $60M Ponzi — confirms structural fraud risk remains acute.

- Political / PolicyMedium

The Trump administration's deregulatory shift reduced near-term enforcement risk but introduced Warren-led congressional scrutiny over conflicts of interest that could reverse course with political winds.

Outlook

The SEC’s role in crypto is entering a more mature, structurally important phase. On one front, the Commission is consolidating its view that tokenized securities are just securities in a new format, enabling pilots on Nasdaq and partnerships between NYSE and tokenization platforms like Securitize while working with ETF sponsors such as T. Rowe Price to bring active crypto funds into the regulated mainstream. On another front, it is redefining the boundaries of securities law in the digital era, through taxonomies of digital commodities and tools, nuanced treatment of non‑security crypto assets within investment contracts, and guidance on airdrops, staking, and wrapping. Parallel efforts with the CFTC and Congress—ranging from joint comment requests on swap definitions to the Clarity Act’s jurisdictional lanes and self‑custody rights—aim to resolve the turf wars that have long plagued U.S. crypto oversight.

For crypto builders and investors, the implications are profound. If the SEC’s proposed market‑structure reforms succeed, tokenized U.S. stocks and DeFi‑style market makers could eventually operate at scale within the national market system, blurring lines between Wall Street and on‑chain finance. If tokenization pilots on major exchanges demonstrate clear efficiency and transparency gains without new forms of risk, the logic that “format should not change regulatory outcome” may become the foundation for broader tokenization of everything from corporate bonds to funds and RWAs. And if AI‑driven advisers like Coinbase’s SEC‑registered Advisor prove they can deliver compliant, accessible exposure to both securities and crypto assets, the traditional distinction between “crypto users” and “securities investors” may fade as diversified portfolios routinely blend tokenized and non‑tokenized instruments.

At the same time, the SEC’s caution on DeFi, yield products, and unregistered offerings will continue to constrain the more experimental edges of crypto, pushing some activity offshore or into gray areas while also shielding many U.S. investors from the riskiest projects. Global peers, such as the Philippine SEC, will keep testing alternative models, especially for RWA tokenization and sandbox‑driven innovation. Over the next several years, the central question will not be whether the SEC regulates crypto—it already does—but whether it can do so in a way that preserves the open, permissionless qualities that made crypto compelling in the first place while meeting its investor‑protection mandate. For anyone building or investing in digital assets, staying abreast of SEC rulemakings, interpretations, and enforcement priorities is no longer optional; it is part of understanding how the future of finance itself is being negotiated.

Latest SEC news

Bitcoin Depot discloses $3.6M BTC theft from corporate wallets in SEC filing, two weeks after breachFormer SEC Chief Economist backs a16z-backed safe harbor, arguing tokenized securities on DeFi can cut costs, enable 24/7 markets, and boost transparency despite regulatory tradeoffsSecuritize appoints former SEC and JPMorgan executive Brett Redfearn as president and board member, strengthening leadership as tokenization and digital asset markets expandSEC axes $25,000 pattern day trader minimum after 25 years, FINRA pivots to risk-based intraday marginSEC staff addresses broker-dealer registration requirements for crypto transaction interfacesOndo Finance requests SEC no-action letter to record tokenized securities on EthereumSources

- https://www.sec.gov/newsroom/press-releases/2026-30-sec-clarifies-application-federal-securities-laws-crypto-assets

- https://www.sec.gov/newsroom/speeches-statements/corp-fin-statement-tokenized-securities-012826-statement-tokenized-securities

- https://www.bitget.com/amp/news/detail/12560605468932

- https://unchainedcrypto.com/cftc-and-sec-seek-comment-on-defining-swaps-as-cme-sues-the-cftc-over-the-same-question/

- https://www.sec.gov/newsroom/press-releases/2026-54-sec-proposes-rescission-regulation-nms-rules-611-610e

- https://www.youtube.com/watch?v=xqrUN2gS2pM

- https://www.coinbase.com/advisor

- https://www.federalregister.gov/documents/2026/06/17/2026-12160/self-regulatory-organizations-nyse-arca-inc-order-granting-approval-of-a-proposed-rule-change-as

- https://katten.com/perpetual-futures-come-onshore-the-cftcs-new-regulatory-framework

- https://www.sec.gov/Archives/edgar/data/2034269/000095010326003337/dp242886_425-cantor.htm

- https://crypto.news/philippine-sec-embraces-tokenization-as-sandbox-bets-expand/

- https://www.kucoin.com/news/flash/philippine-sec-says-ready-to-regulate-rwa-tokenization

- https://financefeeds.com/secs-selway-pushes-toward-unified-crypto-market-rules-as-perpetual-futures-debate-intensifies/

- https://thedefiant.io/news/cefi/coinbase-system-update-sec-registered-ai-advisor-stock-options-brokerage-push

- https://www.tradingview.com/news/cointelegraph:714aedcdd094b:0-sec-plan-to-scrap-rule-611-positive-for-tokenized-us-stocks-galaxy/

- https://oag.maryland.gov/News/Documents/pdfs/2026-4-30%20CFTC%20Comment%20Letter.pdf

- https://ir.theice.com/press/news-details/2026/New-York-Stock-Exchange-and-Securitize-Agree-to-Memorandum-of-Understanding-to-Support-Tokenized-Securities/default.aspx

- https://www.sec.gov/Archives/edgar/data/2089855/000199937126005896/active-s1a_031626.htm

- https://www.youtube.com/watch?v=Ftn3dYknFz0

- https://www.bloomberg.com/news/articles/2026-06-17/sec-proposal-to-scrap-decades-old-stock-rule-has-a-clear-winner

Community notes

Spot something off or out of date? Drop a note. Editors review topic notes daily and roll accepted fixes into the explainer — contributors are recognized in the monthly $SQUID drop.

Loading notes…